1. 調査方法および範囲

1.1. 調査方法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 拡張の種類別スニペット

3.2. 形状別スニペット

3.3. 表面の種類別スニペット

3.4. 用途別スニペット

3.5. エンドユーザー別

3.6. 地域別

4. ダイナミクス

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 美容整形手術に対する需要の高まり

4.1.2. 抑制要因

4.1.2.1. 豊胸手術に伴う合併症や副作用

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 特許分析

5.5. 規制分析

5.6. SWOT分析

5.7. 未充足ニーズ

6. 豊胸の種類別

6.1. はじめに

6.1.1. 種類別分析および前年比成長率(%)

6.1.2. 種類別市場魅力度指数

6.2. 豊胸インプラント*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率(%)

6.2.3. 生理食塩水バッグ入り豊胸インプラント

6.2.4. シリコンバッグ入り豊胸インプラント

6.3. 脂肪注入法による豊胸

7. 形状別

7.1. はじめに

7.1.1. 形状別市場規模および前年比成長率(%)

7.1.2. 形状別市場魅力度指数

7.2. 輪郭のある豊胸インプラント*

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率分析(%)

7.3. 解剖学的乳房インプラント

8. 表面の種類別

8.1. はじめに

8.1.1. 市場規模分析および前年比成長率分析(%)表面の種類別

8.1.2. 市場魅力度指数、表面の種類別

8.2. 滑らかな豊胸インプラント*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率分析(%)

8.3. テクスチャード加工豊胸インプラント

9. 用途別

9.1. はじめに

9.1.1. 市場規模分析および前年比成長率分析(%)、用途別

9.1.2. 用途別市場魅力度指数

9.2. 再建手術*

9.2.1. はじめに

9.2.2. 市場規模分析および前年比成長率分析(%)

9.3. 美容整形手術

10. エンドユーザー別

10.1. はじめに

10.1.1. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

10.1.2. 市場魅力度指数、エンドユーザー別

10.2. 病院 *

10.2.1. 概要

10.2.2. 市場規模分析および前年比成長率分析(%)

10.3. 美容クリニック

11. 地域別

11.1. はじめに

11.1.1. 市場規模分析および前年比成長率分析(%)、地域別

11.1.2. 市場魅力度指数、地域別

11.2. 北米

11.2.1. はじめに

11.2.2. 主な地域特有の動向

11.2.3. 市場規模分析および前年比成長率分析(%)、増強の種類別

11.2.4. 市場規模分析および前年比成長率分析(%)、形状別

11.2.5. 市場規模分析および前年比成長率分析(%)、表面の種類別

11.2.6. 市場規模分析および前年比成長率分析(%)、用途別

11.2.7. エンドユーザー別市場規模分析および前年比成長率分析(%)

11.2.8. 国別市場規模分析および前年比成長率分析(%)

11.2.8.1. 米国

11.2.8.2. カナダ

11.2.8.3. メキシコ

11.3. ヨーロッパ

11.3.1. はじめに

11.3.2. 主要地域別の動向

11.3.3. 市場規模分析および前年比成長率分析(%)、種類別

11.3.4. 市場規模分析および前年比成長率分析(%)、形状別

11.3.5. 市場規模分析および前年比成長率分析(%)、表面の種類別

11.3.6. 用途別市場規模分析および前年比成長率(%)

11.3.7. エンドユーザー別市場規模分析および前年比成長率(%)

11.3.8. 国別市場規模分析および前年比成長率(%)

11.3.8.1. ドイツ

11.3.8.2. イギリス

11.3.8.3. フランス

11.3.8.4. スペイン

11.3.8.5. イタリア

11.3.8.6. ヨーロッパのその他地域

11.4. 南アメリカ

11.4.1. はじめに

11.4.2. 主要地域特有の動向

11.4.3. 市場規模分析および前年比成長率分析(%)、種類別

11.4.4. 市場規模分析および前年比成長率分析(%)、形状別

11.4.5. 市場規模分析および前年比成長率分析(%)、表面の種類別

11.4.6. 市場規模分析および前年比成長率分析(%)、用途別

11.4.7. エンドユーザー別市場規模分析および前年比成長率分析(%)

11.4.8. 国別市場規模分析および前年比成長率分析(%)

11.4.8.1. ブラジル

11.4.8.2. アルゼンチン

11.4.8.3. 南米その他

11.5. アジア太平洋

11.5.1. はじめに

11.5.2. 主要地域別の動向

11.5.3. 市場規模分析および前年比成長率分析(%)、種類別

11.5.4. 市場規模分析および前年比成長率分析(%)、形状別

11.5.5. 市場規模分析および前年比成長率分析(%)、表面の種類別

11.5.6. 用途別市場規模分析および前年比成長率(%)

11.5.7. エンドユーザー別市場規模分析および前年比成長率(%)

11.5.8. 国別市場規模分析および前年比成長率(%)

11.5.8.1. 中国

11.5.8.2. インド

11.5.8.3. 日本

11.5.8.4. 韓国

11.5.8.5. アジア太平洋地域その他

11.6. 中東およびアフリカ

11.6.1. はじめに

11.6.2. 市場規模および前年比成長率分析(%)、増強の種類別

11.6.3. 市場規模分析および前年比成長率分析(%)、種類別

11.6.4. 市場規模分析および前年比成長率分析(%)、表面の種類別

11.6.5. 市場規模分析および前年比成長率分析(%)、用途別

11.6.6. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

12. 競合状況

12.1. 競合シナリオ

12.2. 市場ポジショニング/シェア分析

12.3. 合併・買収分析

13. 企業プロフィール

Johnson & Johnson

AbbVie

Sientra, Inc.

GC Aesthetics

POLYTECH Health & Aesthetics GmbH

Sebbin

Laboratoires Arion

Silimed

Establishment Labs and Guangzhou Wanhe Plastic Material Co., Ltd

(リストは網羅的ではありません)

14. 付録

14.1. 当社およびサービスについて

14.2. お問い合わせ

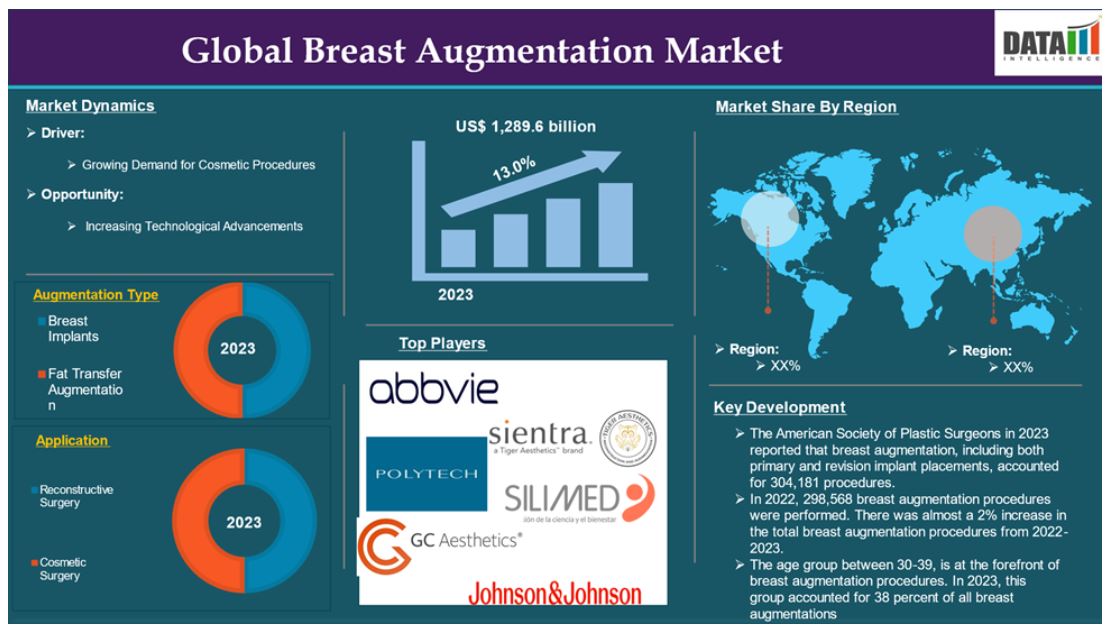

The global breast augmentation market reached US$ 1,289.6 million in 2023 and is expected to reach US$ 3,440.6 million by 2031, growing at a CAGR of 13.0% during the forecast period 2024-2031.

Breast augmentation, also referred to as augmentation mammoplasty, is a surgical procedure designed to enhance the size and volume of the breasts. This enhancement can be accomplished using breast implants or through fat transfer techniques. Individuals often seek this procedure for a variety of reasons, such as increasing breast fullness, restoring volume lost due to weight loss or pregnancy, correcting asymmetry between the breasts, and improving overall body proportions.

The choice of implant type and placement method can significantly influence the aesthetic outcome and recovery experience. Patients often pursue this procedure to boost self-confidence and improve their body image. While breast augmentation can enhance appearance.

Breast augmentations are ranked as the number one cosmetic surgery for women based on gender distribution data, while breast implants are ranked as the 13th most popular procedure among men.

Market Dynamics: Drivers & Restraints

Growing demand for cosmetic procedures

The growing demand for cosmetic procedures, influenced by a blend of social, cultural, economic, and technological elements, is a key factor driving the expansion of the breast augmentation market. The market is witnessing substantial growth as more individuals pursue aesthetic enhancements such as breast augmentation.

Many people seek breast augmentation not only for cosmetic reasons but also to improve their self-esteem and body image. This procedure can empower women, helping them feel more confident and at ease in their own bodies. The number of individuals undergoing breast augmentation is expected to rise with the growing interest among individuals. For instance, according to the report by the American Society of Plastic Surgeons in 2023, breast augmentation, including both primary and revision implant placements, accounted for 304,181 procedures. In 2022, 298,568 breast augmentation procedures were performed. There was almost a 2% increase in the total breast augmentation procedures from 2022-2023.

The age group between 30-39, is at the forefront of breast augmentation procedures. In 2023, this group accounted for 38 percent of all breast augmentations, driven by a mix of aesthetic aspirations and a growing acceptance of cosmetic enhancements. Additionally, there has been an increase in the number of women pursuing reconstructive surgery after breast cancer treatment. In these cases, breast implants are frequently utilized, offering a solution for breast reconstruction and assisting patients in regaining a sense of normalcy. The rise in breast cancer survivors seeking reconstruction has further contributed to the demand for breast implants, broadening the market to encompass both cosmetic enhancements and medical reconstructive needs.

Moreover, the increasing advancements in surgeries and the approvals of more breast implants with advanced features are expected to drive the breast augmentation market.

Complications and side effects associated with breast augmentation

Complications and side effects linked to breast augmentation procedures are expected to considerably impede the growth of the breast augmentation market. The complications and side effects such as breast implant-associated anaplastic large cell lymphoma (BIA-ALCL) or other very rare cancers in the capsule around the breast, such as breast implant-associated squamous cell carcinoma (BIA-SCC) could result after breast augmentation.

Also bleeding, changes in breast sensation, fluid accumulation (seroma), formation of tight scar tissue around the implant (capsular contracture), hematoma, implant leakage or rupture, infection, persistent pain, and poor scarring complications associated with breast augmentation are expected to restrict the individual from undergoing the breast augmentation procedure. There is a large increase in the number of individuals who have removed breast implants which could be due its side effects.

Segment Analysis

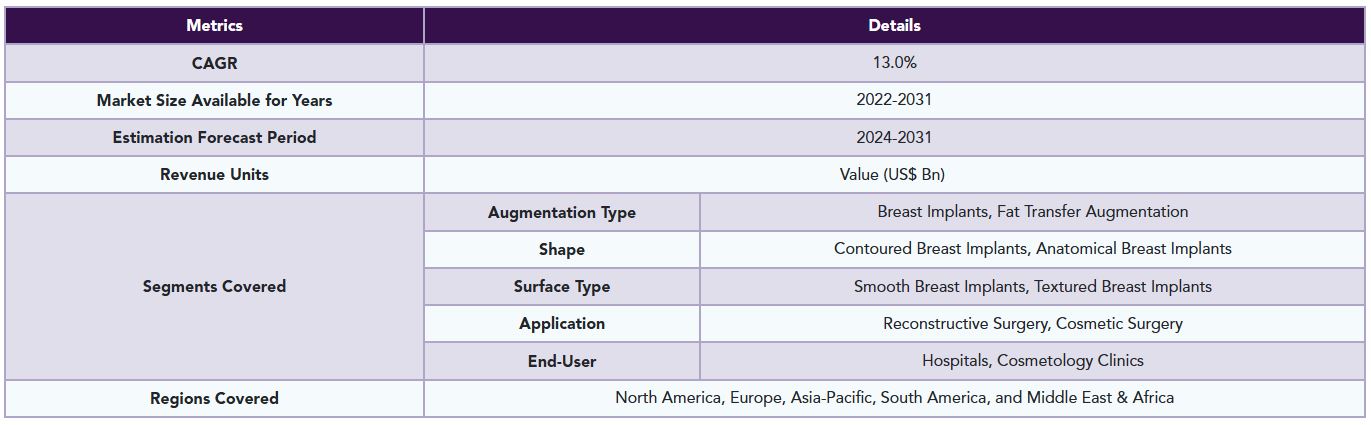

The global breast augmentation market is segmented based on augmentation type, shape, surface type, application, end-user, and region.

Augmentation Type:

The breast implants segment is expected to dominate the global breast augmentation market share

The breast implants segment is experiencing significant growth, driven by several key factors. Patients are increasingly opting for silicone implants due to their more natural appearance and feel compared to saline alternatives. This growing preference for silicone implants is fueling the demand within the market. Additionally, the rising incidence of breast cancer has further contributed to the growth of this segment, as breast implants are commonly used for post-mastectomy reconstruction.

The segment’s expansion is also supported by ongoing product approvals, frequent new product launches, and continuous innovations in implant technology. Companies are addressing the growing patient demand for longer-lasting implants by improving durability and reducing the risk of complications such as rupture and leakage. Advancements in cohesive silicone gels and enhanced outer shell designs have resulted in implants that can last longer, with some products offering warranties of 10 years or more.

With the rising demand for breast implants, the companies are introducing their products. For instance, in April 2024 GC Aesthetics (GCA) introduced a micro-textured anatomical breast implant LUNA XT. The company says it is the first breast implant in the world approved under the new European Medical Device Regulation (MDR).

Furthermore, manufacturers are increasingly focusing on biocompatibility, ensuring that implants are not only safe but also well-tolerated by the body. The development of biocompatible materials helps minimize the risks of inflammation and immune system rejection, enhancing the safety and success of breast implant procedures.

Moreover, the Food and Drug Administration (FDA) is approving breast implants by evaluating their safety. For instance, in September 2024, the FDA approved for marketing of Motiva USA, LLC’s SmoothSilk Round and Round Ergonomic Silicone Gel-Filled Breast Implants, indicated for breast augmentation for patients of at least 22 years of age.

Together, these factors are propelling the breast implant segment toward continued growth and dominance in the breast augmentation market. As these trends progress, the segment's growth is expected to expand substantially.

Geographical Analysis

North America is expected to hold a significant position in the global breast augmentation market share

North America holds a dominant position in the breast augmentation market. The region's dominance in the breast augmentation market is attributed to several critical factors that collectively enhance its position. The increasing number of breast augmentation surgeries reflects a growing societal acceptance of cosmetic enhancements. For instance, according to the publication by the Toronto Plastic Surgeons, in the United States alone, 255,200 breast augmentation surgeries were performed in 2022, making it the leader in this category globally with approximately 11.7% of the total number of breast augmentations performed worldwide.

Technological advancements play a pivotal role in this market's growth. Innovations such as cohesive silicone gel implants have significantly improved safety and aesthetic outcomes, enhancing patient satisfaction and driving further demand for breast augmentation procedures.

The region's robust regulatory environment ensures high safety standards for medical devices and procedures, fostering consumer confidence in breast augmentation options. With the rising approvals of breast implants in the region, the region is addressing the rising demand for breast implants globally. The rising number of approvals of implants is also expected to contribute to the region’s market growth. For instance, in March 2022, Sientra, Inc. received approval from Health Canada to market the Company’s line of smooth surface, High-Strength Cohesive (HSC and HSC+) silicone gel breast implants in Canada.

As these factors continue to evolve, North America is expected to maintain its dominant position in the breast augmentation market, contributing to a thriving landscape that is projected to grow in the coming years.

Asia Pacific is growing at the fastest pace in the global breast augmentation market

The Asia-Pacific (APAC) region is currently emerging as one of the fastest-growing markets for breast augmentation, encompassing both aesthetic and reconstructive procedures. Several factors contribute to the rapid expansion of the breast augmentation market in this region. There is a growing societal focus on physical appearance and body image in the APAC region, resulting in heightened acceptance of cosmetic procedures among women. This cultural shift is driving an increased demand for aesthetic enhancements, including breast augmentation.

Competitive Landscape

The major global players in the breast augmentation market include Johnson & Johnson, AbbVie, Sientra, Inc., GC Aesthetics, POLYTECH Health & Aesthetics GmbH, Sebbin, Laboratoires Arion, Silimed, Establishment Labs and Guangzhou Wanhe Plastic Material Co., Ltd among others.

Key Developments

• In September 2024, GC Aesthetics (GCA) launched the YOUTHLY brand in China, featuring its latest breast implant innovations: PERLE, Luna XT, and the latest version of The Round Collection, 100% filled.

• In September 2024, POLYTECH introduced Opticon Plus, an innovative addition to its broad portfolio. POLYTECH's portfolio now includes this new implant, which sits between their anatomical forms Replicon and Opticon, providing surgeons with an option that features a base shape between the round Replicon® base and the standard Opticon short oval base.

Why Purchase the Report?

• Pipeline & Innovations: Insights into clinical trials, product pipelines, and upcoming advancements.

• Market Positioning: Analysis of product performance and growth potential for optimized strategies.

• Real-World Evidence: Integration of patient feedback for enhanced product outcomes.

• Physician Preferences: Insights into healthcare provider behaviors and adoption strategies.

• Regulatory & Market Updates: Coverage of recent regulations, policies, and emerging technologies.

• Competitive Insights: Analysis of market share, competitor strategies, and new entrants.

• Pricing & Market Access: Review of pricing models, reimbursement trends, and access strategies.

• Market Expansion: Strategies for entering new markets and forming partnerships.

• Regional Opportunities: Identification of high-growth regions and investment prospects.

• Supply Chain Optimization: Assessment of risks and distribution strategies.

• Sustainability & Regulation: Focus on eco-friendly practices and regulatory changes.

• Post-Market Surveillance: Enhanced safety and access through post-market data.

• Value-Based Pricing: Insights into pharmacoeconomics and data-driven R&D decisions.

The global breast augmentation market report delivers a detailed analysis with 60+ key tables, more than 50 visually impactful figures, and 176 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

Table of Contents

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Augmentation Type

3.2. Snippet by Shape

3.3. Snippet by Surface Type

3.4. Snippet by Application

3.5. Snippet by End-User

3.6. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Growing demand for cosmetic procedures

4.1.2. Restraints

4.1.2.1. Complications and side effects associated with breast augmentation

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Patent Analysis

5.5. Regulatory Analysis

5.6. SWOT Analysis

5.7. Unmet Needs

6. By Augmentation Type

6.1. Introduction

6.1.1. Analysis and Y-o-Y Growth Analysis (%), By Augmentation Type

6.1.2. Market Attractiveness Index, By Augmentation Type

6.2. Breast Implants*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.2.3. Saline Breast Implants

6.2.4. Silicone Breast Implants

6.3. Fat Transfer Augmentation

7. By Shape

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Shape

7.1.2. Market Attractiveness Index, By Shape

7.2. Contoured Breast Implants*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Anatomical Breast Implants

8. By Surface Type

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Surface Type

8.1.2. Market Attractiveness Index, By Surface Type

8.2. Smooth Breast Implants*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Textured Breast Implants

9. By Application

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.1.2. Market Attractiveness Index, By Application

9.2. Reconstructive Surgery*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Cosmetic Surgery

10. By End-User

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.1.2. Market Attractiveness Index, By End-User

10.2. Hospitals *

10.2.1. Introduction

10.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

10.3. Cosmetology Clinics

11. By Region

11.1. Introduction

11.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

11.1.2. Market Attractiveness Index, By Region

11.2. North America

11.2.1. Introduction

11.2.2. Key Region-Specific Dynamics

11.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Augmentation Type

11.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Shape

11.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Surface Type

11.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

11.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.2.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.2.8.1. U.S.

11.2.8.2. Canada

11.2.8.3. Mexico

11.3. Europe

11.3.1. Introduction

11.3.2. Key Region-Specific Dynamics

11.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Augmentation Type

11.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Shape

11.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Surface Type

11.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

11.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.3.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.3.8.1. Germany

11.3.8.2. U.K.

11.3.8.3. France

11.3.8.4. Spain

11.3.8.5. Italy

11.3.8.6. Rest of Europe

11.4. South America

11.4.1. Introduction

11.4.2. Key Region-Specific Dynamics

11.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Augmentation Type

11.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Shape

11.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Surface Type

11.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

11.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.4.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.4.8.1. Brazil

11.4.8.2. Argentina

11.4.8.3. Rest of South America

11.5. Asia-Pacific

11.5.1. Introduction

11.5.2. Key Region-Specific Dynamics

11.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Augmentation Type

11.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Shape

11.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Surface Type

11.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

11.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.5.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.5.8.1. China

11.5.8.2. India

11.5.8.3. Japan

11.5.8.4. South Korea

11.5.8.5. Rest of Asia-Pacific

11.6. Middle East and Africa

11.6.1. Introduction

11.6.2. Market Size Analysis and Y-o-Y Growth Analysis (%), By Augmentation Type

11.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Shape

11.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Surface Type

11.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

11.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

12. Competitive Landscape

12.1. Competitive Scenario

12.2. Market Positioning/Share Analysis

12.3. Mergers and Acquisitions Analysis

13. Company Profiles

13.1. Johnson & Johnson*

13.1.1. Company Overview

13.1.2. Product Portfolio and Description

13.1.3. Financial Overview

13.1.4. Key Developments

13.2. AbbVie

13.3. Sientra, Inc.

13.4. GC Aesthetics

13.5. POLYTECH Health & Aesthetics GmbH

13.6. Sebbin

13.7. Laboratoires Arion

13.8. Silimed

13.9. Establishment Labs

13.10. Guangzhou Wanhe Plastic Material Co.,Ltd(LIST NOT EXHAUSTIVE)

14. Appendix

14.1. About Us and Services

14.2. Contact Us

*** 豊胸手術の世界市場に関するよくある質問(FAQ) ***

・豊胸手術の世界市場規模は?

→DataM Intelligence社は2023年の豊胸手術の世界市場規模を12億8,960万米ドルと推定しています。

・豊胸手術の世界市場予測は?

→DataM Intelligence社は2031年の豊胸手術の世界市場規模を34億4,060万米ドルと予測しています。

・豊胸手術市場の成長率は?

→DataM Intelligence社は豊胸手術の世界市場が2024年~2031年に年平均13.0%成長すると展望しています。

・世界の豊胸手術市場における主要プレイヤーは?

→「Johnson & Johnson、AbbVie、Sientra, Inc.、GC Aesthetics、POLYTECH Health & Aesthetics GmbH、Sebbin、Laboratoires Arion、Silimed、 Establishment Labs and Guangzhou Wanhe Plastic Material Co., Ltdなど ...」を豊胸手術市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/