1. 調査方法および範囲

1.1. 調査方法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品種類別抜粋

3.2. 接続別抜粋

3.3. 用途別抜粋

3.4. エンドユーザー別抜粋

3.5. 地域別

4. ダイナミクス

4.1. 影響要因

4.1.1. 推進要因

4.1.1.1. 技術の進歩

4.1.1.2. XX

4.2. 抑制要因

4.2.1. 熟練した専門家の不足

4.3. 機会

4.3.1. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

6. 製品種類別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率(%)、製品種類別

6.1.2. 製品種類別市場魅力度指数

6.2. ウェアラブルECGセンサー *

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率分析(%)

6.3. パッチECGセンサー

6.4. ワイヤレスECGセンサー

6.5. 一体型ECGデバイス

7. 接続性別

7.1. はじめに

7.1.1. 接続性別市場規模分析および前年比成長率(%)

7.1.2. 接続性別市場魅力度指数

7.2. 有線*

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率(%)

7.3. 有線

8. 用途別

8.1. はじめに

8.1.1. 用途別市場規模分析および前年比成長率分析(%)

8.1.2. 用途別市場魅力度指数

8.2. 不整脈*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率分析(%)

8.3. 心筋梗塞

8.4. その他

9. エンドユーザー別

9.1. はじめに

9.1.1. エンドユーザー別市場規模分析および前年比成長率分析(%)

9.1.2. エンドユーザー別市場魅力度指数

9.2. 病院および診療所*

9.2.1. はじめに

9.2.2. 市場規模分析および前年比成長率分析(%)

9.3. 外来外科センター

9.4. 在宅医療施設

9.5. スポーツおよびフィットネスセンター

9.6. 研究機関

10. 地域別

10.1. はじめに

10.1.1. 地域別市場規模分析および前年比成長率分析(%)

10.1.2. 市場魅力度指数、地域別

10.2. 北米

10.2.1. はじめに

10.2.2. 地域特有の主な動向

10.2.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.2.4. 市場規模分析および前年比成長率分析(%)、接続別

10.2.5. 用途別市場規模分析および前年比成長率(%)

10.2.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.2.7. 国別市場規模分析および前年比成長率(%)

10.2.7.1. 米国

10.2.7.2. カナダ

10.2.7.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 地域別の主な動向

10.3.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.3.4. 市場規模分析および前年比成長率分析(%)、接続別

10.3.5. 用途別市場規模分析および前年比成長率分析(%)

10.3.6. エンドユーザー別市場規模分析および前年比成長率分析(%)

10.3.7. 国別市場規模分析および前年比成長率分析(%)

10.3.7.1. ドイツ

10.3.7.2. 英国

10.3.7.3. フランス

10.3.7.4. スペイン

10.3.7.5. イタリア

10.3.7.6. ヨーロッパのその他地域

10.4. 南アメリカ

10.4.1. はじめに

10.4.2. 主要地域特有の動向

10.4.3. 製品種類別市場規模分析および前年比成長率(%)

10.4.4. 接続別市場規模分析および前年比成長率(%)

10.4.5. 用途別市場規模分析および前年比成長率(%)

10.4.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.4.7. 市場規模の分析と前年比成長率の分析(%)、国別

10.4.7.1. ブラジル

10.4.7.2. アルゼンチン

10.4.7.3. 南米のその他地域

10.5. アジア太平洋地域

10.5.1. はじめに

10.5.2. 主要地域特有の動向

10.5.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.5.4. 市場規模分析および前年比成長率分析(%)、接続別

10.5.5. 市場規模分析および前年比成長率分析(%)、用途別

10.5.6. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

10.5.7. 国別の市場規模分析および前年比成長率分析(%)

10.5.7.1. 中国

10.5.7.2. インド

10.5.7.3. 日本

10.5.7.4. 韓国

10.5.7.5. アジア太平洋地域その他

10.6. 中東およびアフリカ

10.6.1. はじめに

10.6.2. 地域別主要動向

10.6.3. 製品種類別市場規模分析および前年比成長率分析(%)

10.6.4. 接続形態別市場規模分析および前年比成長率分析(%)

10.6.5. 用途別市場規模分析および前年比成長率分析(%)

10.6.6. 市場規模の分析と前年比成長率の分析(%)、エンドユーザー別

10.6.7. 市場規模の分析と前年比成長率の分析(%)、エンドユーザー別

11. 競合状況

11.1. 競合シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. 合併・買収分析

12. 企業プロフィール

Texas Instruments Inc

Movesense

Unimed Medical Supplies Inc.

APK Technology Co., Ltd.

Shenzhen Amydi-med Electronic Technology Co., Ltd

Monitor Health

Mobile Sense Technologies Inc.

VitalSignum Oy

RONSEDA ELECTRONICS CO.,LTD

KEBORUI

(リストは網羅的ではありません)

12. 付録

12.1 当社およびサービスについて

12.2 お問い合わせ

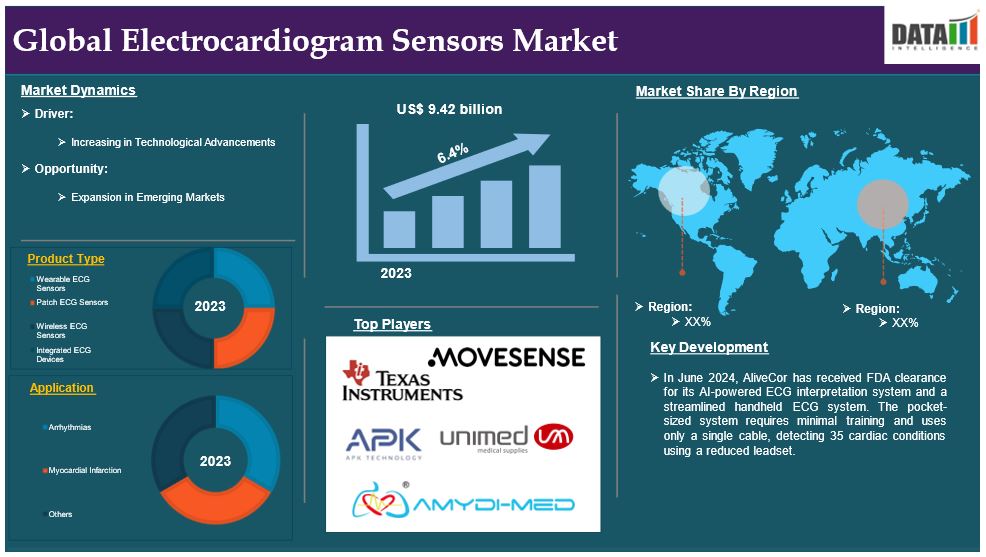

The global electrocardiogram sensors market reached US$ 9.42 billion in 2023 and is expected to reach US$ 15.41 billion by 2031, growing at a CAGR of 6.4% during the forecast period 2024-2031.

ECG sensors are significant constituents of the operation and diagnosis of heart conditions in assessing the heart's electric activity. In fact, another important function includes those in the detection of arrhythmias, myocardial infarctions, and other cardiac abnormalities, which require immediate detection and intervention through medical channelization. Technologically speaking, ECG sensors have evolved over time, changing from large machines to compact use in the form of wearable gadgets like smartwatches, fitness trackers, and wireless patches, making them easy to access and use for people. An increment in cardiovascular diseases and increased demand for home or remote monitoring and fitness-tracking services geared towards that will build.

Market Dynamics: Drivers & Restraints

Increasing Technological Advancements

Advances in technology are set to revolutionize quite a lot in the world electrocardiogram (ECG) sensors market in terms of innovation and extension in possible applications among healthcare settings. For example, advancements like miniaturization, wireless connectivity, and artificial intelligence integration have made ECG sensors much more functional with regard to accuracy, making them easier and more friendly to handle. With the aid of advancement technologies, wearable ECG sensors now allow real-time monitoring, early detection of low arrhythmic events, and personalized health insights, enabling patients to manage their cardiac health from a distance. AI-driven algorithms improve diagnostic precision through complex data pattern analysis while relieving the healthcare professional's burden.

Innovations in sensor materials and designs, such as flexible skin-friendly patches, have brought about increased comfort and compliance with the patient. These are in line with the emergent trends of telemedicine and home-based care, positioning ECG sensors as among the modern healthcare delivery's modalities, but are playing a huge role in accelerating the growth of the market.

For instance, in August 2023, Finnish medical device manufacturer Movesense has introduced a lightweight wearable ECG sensor, 'Movesense Medical', for remote patient monitoring and telehealth applications. The Class IIa device is registered under the EU Medical Device Regulation and is intended for use by remote healthcare providers, manufacturers, hospitals, or companies developing their own medical devices.

Lack of Skilled Professionals

The availability of knowledgeable personnel who can correctly interpret the ECG data present forms an important limitation in the global electrocardiogram (ECG) sensors market, particularly in countries with poor healthcare infrastructure. Sensor technology and AI have introduced various innovations that can make ECG monitoring simpler, but the interpretation of complex cardiac signals often has to be carried out by trained cardiologists or specialists.

This gap in rural and isolated areas further confines access to such expertise, limiting the effectiveness of the ECG sensor installation. Besides, automated systems over-dependence may lead to misdiagnosis due to lack of validation by human oversight, further frowning on the trust and adoption of these devices. This skill shortage and unequal distribution of healthcare resources serve as yet more disincentives to the uptake, distribution, and use of ECG sensor technologies.

Segment Analysis

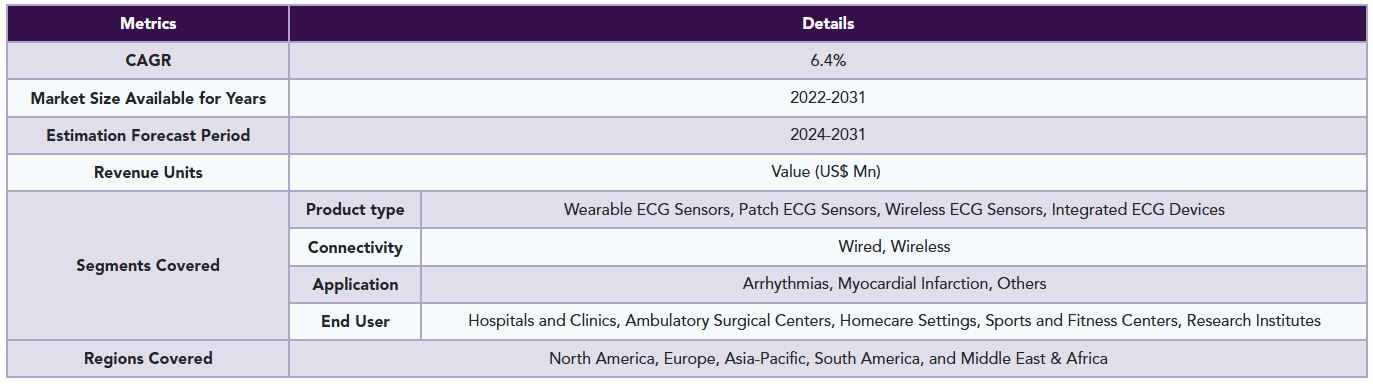

The global electrocardiogram sensors market is segmented based on product type, connectivity, application, end user and region.

Product type:

Wearable ECG sensors segment is expected to dominate the electrocardiogram sensors market share

The Wearable ECG sensors segment holds a major portion of the electrocardiogram sensors market share and is expected to continue to hold a significant portion of the electrocardiogram sensors market share during the forecast period.

The emergence of wearable ECG sensors will transform the whole electrocardiogram (ECG) sensors market beyond its limits by providing convenient real-time heart monitoring solutions. The demand for remote ongoing care is driving this trend further. Battery-powered miniature, user-friendly devices such as watches, patches, or fitness bands will allow users to continuously monitor their hearts. Especially for arrhythmias, chronic cardiac conditions, and preventive care, these devices will add value. State-of-the-art technologies give AI and Bluetooth-influenced advantages in the area of promising features such as accuracy multiple and easy availability to instant diagnosis.

The continuous advancement gives rise to the use of wearables in home settings with high demand because of an increase in cardiovascular diseases causing maximum consumer awareness of monitoring their health and hence the change towards home and personal healthcare solutions, plus the emergence of the technological landscape. Ultimately, the adoption of wearable ECG sensors resonates with global telemedicine and digital health trends that will not miss being accomplished for future modern needs of the health system and will contribute significantly to its market growth.

For instance, in October 2023, RMIT University in Australia has developed a lightweight, gel-free, and waterproof electrocardiogram (ECG) sensor that offers comfort and less skin irritation compared to other heart monitoring devices. The wearable ECG device, which weighs only 10 grams, could be used to prevent heart attacks in remote healthcare and ambulatory care settings, helping manage cardiovascular disease, which affects around 4 Billion Australians and kills over 100 people daily.

Application:

Arrhythmias segment is the fastest-growing segment in electrocardiogram sensors market share

The arrhythmias segment is the fastest-growing segment in the electrocardiogram sensors market share and is expected to hold the market share over the forecast period.

This market for ECG sensors globally is highly driven by arrhythmias in view of the urgency they present in effective diagnosis and monitoring solutions with which to meet the increasing burden of such irregular heart rhythms. Such conditions as atrial fibrillation, ventricular tachycardia, and bradycardia, which call for extremely continuous and accurate tracking of heart rhythm, have been the catalyst for the rapid adoption of advanced ECG sensors throughout clinical and personal healthcare. The increasing drive for wearable devices that detect real-time arrhythmias, like smartwatches and portable ECG monitors, has given the predicted boost in market revenue.

Technology innovations in sensors, such as AI integration and wireless connectivity, could definitely increase the accuracy and convenience of arrhythmia detection for early intervention and better patient outcomes. Additionally, the rising incidence of arrhythmias in the global world, which is greatly due to increased aging of the population, inactivity lifestyles, and the presence of cardiovascular conditions, makes ECG sensors irreplaceable tools in ensuring heart health and hence a potent driver of market growth.

Geographical Analysis

North America is expected to hold a significant position in the electrocardiogram sensors market share

North America holds a substantial position in the electrocardiogram sensors market and is expected to hold most of the market share due to advanced healthcare infrastructure, a high prevalence of cardiovascular diseases, and a growing inclination toward advanced diagnostic tools for heart health management.

Moreover, North America is also seeing a surge in the adoption of wearable and portable ECG monitoring devices, all against the backdrop of increasing usage of remote patient monitoring and telemedicine services, as boosted through extensive government initiatives and investments in digital health technologies for better early diagnosis and disease management. The development of the market is also aided by the presence of key industry players as well as continuous innovations in sensor technologies such as wireless and AI-enabled ECG devices. Furthermore, an intensely technology-based population and favorable reimbursement policies concerning cardiac diagnostic procedures withhold value to the end users for better adoption of ECG sensors in clinical and personal health applications.

For instance, in May 2024, Defibtech, a US manufacturer of life-saving medical equipment, has introduced dual-language AED models in their Lifeline VIEW and Lifeline ECG product lines. These models allow rescuers to choose English or Spanish as the spoken language with a simple touch of a button. The new AED models are designed to make the devices accessible to more of the population, thereby saving more lives from sudden cardiac arrest. Joseph Mullally, Senior Vice President of Commercial Operations for Defibtech, expressed his satisfaction with the additions.

Europe is growing at the fastest pace in the electrocardiogram sensors market

Europe holds the fastest pace in the electrocardiogram sensors market and is expected to hold most of the market share.

Growing burden of cardiovascular diseases because of this aging population and sedentary lifestyle is what's propelling the ECG sensors market in Europe, along with rising awareness on preventive healthcare. To boost the ECG market, government-sponsored healthcare systems and strong regulatory frameworks ensure the availability and adoption of advanced technologies. Awareness campaigns and initiatives have led to significant acceptance of these devices for continuous and wearable monitoring in the region, emphasizing early detection and management of heart conditions.

Innovations in small, wireless, and integrated AI technology ECG sensors have emerged through collaborative efforts of healthcare providers and technology developers to further increase their use in hospitals and outpatient settings as well as in homes. However, this region continues to stimulate the growth of demand concerning ECG sensors, hence making Europe a substantial contributor to this global market because of its research and development, as well as improvement in healthcare outcomes.

Competitive Landscape

The major global players in the electrocardiogram sensors market include Texas Instruments Inc, Movesense, Unimed Medical Supplies Inc., APK Technology Co., Ltd., Shenzhen Amydi-med Electronic Technology Co., Ltd, Monitor Health, Mobile Sense Technologies Inc., VitalSignum Oy, RONSEDA ELECTRONICS CO.,LTD, KEBORUI among others.

Emerging Players

The emerging players in the electrocardiogram sensors market include AliveCor, Qardio, Inc, FibriCheck and among others.

Key Developments

• In June 2024, AliveCor has received FDA clearance for its AI-powered ECG interpretation system and a streamlined handheld ECG system. The pocket-sized system requires minimal training and uses only a single cable, detecting 35 cardiac conditions using a reduced leadset.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global electrocardiogram sensors market report delivers a detailed analysis with 60+ key tables, more than 50 visually impactful figures, and 176 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Connectivity & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

Table of Contents

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product Type

3.2. Snippet by Connectivity

3.3. Snippet by Application

3.4. Snippet by End User

3.5. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Increasing Technological Advancements

4.1.1.2. XX

4.2. Restraints

4.2.1. Lack of Skilled Professionals

4.3. Opportunity

4.3.1. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

6. By Product type

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product type

6.1.2. Market Attractiveness Index, By Product type

6.2. Wearable ECG Sensors *

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Patch ECG Sensors

6.4. Wireless ECG Sensors

6.5. Integrated ECG Devices

7. By Connectivity

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

7.1.2. Market Attractiveness Index, By Connectivity

7.2. Wired*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Wired

8. By Application

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

8.1.2. Market Attractiveness Index, By Application

8.2. Arrhythmia*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Myocardial Infarction

8.4. Others

9. By End User

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

9.1.2. Market Attractiveness Index, By End User

9.2. Hospitals and Clinics*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Ambulatory Surgical Centers

9.4. Homecare Settings

9.5. Sports and Fitness Centers

9.6. Research Institutes

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.7.1. U.S.

10.2.7.2. Canada

10.2.7.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.7.1. Germany

10.3.7.2. U.K.

10.3.7.3. France

10.3.7.4. Spain

10.3.7.5. Italy

10.3.7.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.7.1. Brazil

10.4.7.2. Argentina

10.4.7.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.7.1. China

10.5.7.2. India

10.5.7.3. Japan

10.5.7.4. South Korea

10.5.7.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.6.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Texas Instruments Inc*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. Movesense

12.3. Unimed Medical Supplies Inc.

12.4. APK Technology Co., Ltd.

12.5. Shenzhen Amydi-med Electronic Technology Co., Ltd

12.6. Monitor Health

12.7. Mobile Sense Technologies, Inc.

12.8. VitalSignum Oy

12.9. RONSEDA ELECTRONICS CO.,LTD

12.10. KEBORUI (LIST NOT EXHAUSTIVE)

12. Appendix

12.1 About Us and Services

12.2 Contact Us

*** 心電図センサーの世界市場に関するよくある質問(FAQ) ***

・心電図センサーの世界市場規模は?

→DataM Intelligence社は2023年の心電図センサーの世界市場規模を94.2億米ドルと推定しています。

・心電図センサーの世界市場予測は?

→DataM Intelligence社は2031年の心電図センサーの世界市場規模を154.1億米ドルと予測しています。

・心電図センサー市場の成長率は?

→DataM Intelligence社は心電図センサーの世界市場が2024年~2031年に年平均6.4%成長すると展望しています。

・世界の心電図センサー市場における主要プレイヤーは?

→「Texas Instruments Inc、Movesense、Unimed Medical Supplies Inc.、APK Technology Co., Ltd.、Shenzhen Amydi-med Electronic Technology Co., Ltd、Monitor Health、Mobile Sense Technologies Inc.、VitalSignum Oy、RONSEDA ELECTRONICS CO.,LTD、KEBORUIなど ...」を心電図センサー市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/