1. 調査手法および対象範囲

1.1. 調査手法

1.2. 調査目的およびレポートの対象範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品別抜粋

3.2. 素材別抜粋

3.3. 患者グループ別抜粋

3.4. エンドユーザー別抜粋

3.5. 地域別抜粋

4. ダイナミクス

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 慢性疾患の増加

4.1.2. 抑制要因

4.1.2.1. 麻酔専門医の不足

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

5.5. 償還分析

5.6. 特許分析

5.7. SWOT分析

5.8. DMI意見

6. 製品別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率(%)別、製品別

6.1.2. 市場魅力度指数、製品別

6.2. 喉頭鏡*

6.2.1. イントロダクション

6.2.2. 市場規模分析および前年比成長率(%)別

6.3. 蘇生器

6.4. 麻酔マスク

6.5. 呼吸バッグ

6.6. 呼吸回路

6.7. 気管チューブ

6.8. 挿管用アクセサリー

6.9. 喉頭マスク換気装置

7. 素材別

7.1. はじめに

7.1.1. 素材別市場規模分析および前年比成長率(%)

7.1.2. 素材別市場魅力度指数

7.2. プラスチック*

7.2.1. イントロダクション

7.2.2. 市場規模分析および前年比成長率分析(%)

7.3. シリコン

8. 患者グループ別

8.1. イントロダクション

8.1.1. 患者グループ別市場規模分析および前年比成長率分析(%)

8.1.2. 市場魅力度指数、患者グループ別

8.2. 新生児*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率(%)

8.3. 成人

8.4. 小児

9. エンドユーザー別

9.1. はじめに

9.1.1. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

9.1.2. 市場魅力度指数、エンドユーザー別

9.2. 病院および診療所*

9.2.1. 概要

9.2.2. 市場規模分析および前年比成長率分析(%)

9.3. 外来外科センター

9.4. 訪問看護

9.5. その他

10. 地域別

10.1. はじめに

10.1.1. 地域別市場規模分析および前年比成長率(%)

10.1.2. 地域別市場魅力度指数

10.2. 北米

10.2.1. はじめに

10.2.2. 主要地域別の動向

10.2.3. 製品別市場規模分析および前年比成長率分析(%)

10.2.4. 材料別市場規模分析および前年比成長率分析(%)

10.2.5. 患者グループ別市場規模分析および前年比成長率分析(%)

10.2.6. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

10.2.7. 市場規模分析および前年比成長率分析(%)、国別

10.2.7.1. 米国

10.2.7.2. カナダ

10.2.7.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 主要地域別の動向

10.3.3. 製品別市場規模分析および前年比成長率(%)

10.3.4. 材料別市場規模分析および前年比成長率(%)

10.3.5. 患者グループ別市場規模分析および前年比成長率(%)

10.3.6. 市場規模の分析と前年比成長率の分析(%)、エンドユーザー別

10.3.7. 市場規模の分析と前年比成長率の分析(%)、国別

10.3.7.1. ドイツ

10.3.7.2. 英国

10.3.7.3. フランス

10.3.7.4. イタリア

10.3.7.5. スペイン

10.3.7.6. ヨーロッパのその他地域

10.4. 南アメリカ

10.4.1. はじめに

10.4.2. 主要地域別の動向

10.4.3. 製品別市場規模分析および前年比成長率(%)

10.4.4. 市場規模分析および前年比成長率(%)、材料別

10.4.5. 市場規模分析および前年比成長率(%)、患者グループ別

10.4.6. 市場規模分析および前年比成長率(%)、エンドユーザー別

10.4.7. 市場規模分析および前年比成長率(%)、国別

10.4.7.1. ブラジル

10.4.7.2. アルゼンチン

10.4.7.3. 南米その他

10.5. アジア太平洋

10.5.1. はじめに

10.5.2. 主要地域特有の動向

10.5.3. 市場規模分析および前年比成長率分析(%)、製品別

10.5.4. 市場規模分析および前年比成長率(%)、材料別

10.5.5. 市場規模分析および前年比成長率(%)、患者グループ別

10.5.6. 市場規模分析および前年比成長率(%)、エンドユーザー別

10.5.7. 市場規模分析および前年比成長率(%)、国別

10.5.7.1. 中国

10.5.7.2. インド

10.5.7.3. 日本

10.5.7.4. 韓国

10.5.7.5. アジア太平洋地域その他

10.6. 中東およびアフリカ

10.6.1. はじめに

10.6.2. 主要地域特有の動向

10.6.3. 製品別市場規模分析および前年比成長率(%)

10.6.4. 材料別市場規模分析および前年比成長率(%)

10.6.5. 患者グループ別市場規模分析および前年比成長率(%)

10.6.6. エンドユーザー別市場規模分析および前年比成長率(%)

11. 競合状況

11.1. 競合シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. 合併・買収分析

12. 企業プロフィール

Ambu A/S

Drägerwerk AG & Co. KGaA

Teleflex Incorporated

Hamilton Medical

Intersurgical Ltd

Medline Industries

LP

Medtronic

Mercury Medical

Sharn Anesthesia

Narang Medical Limited

リストは網羅的なものではありません

13. 付録

13.1. 当社およびサービスについて

13.2. お問い合わせ

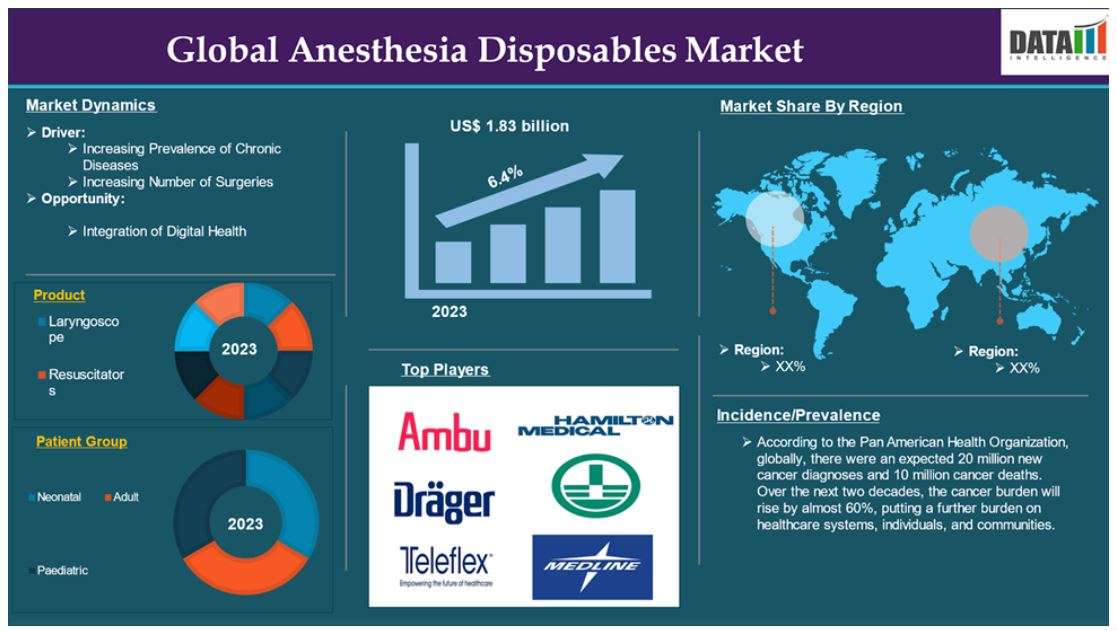

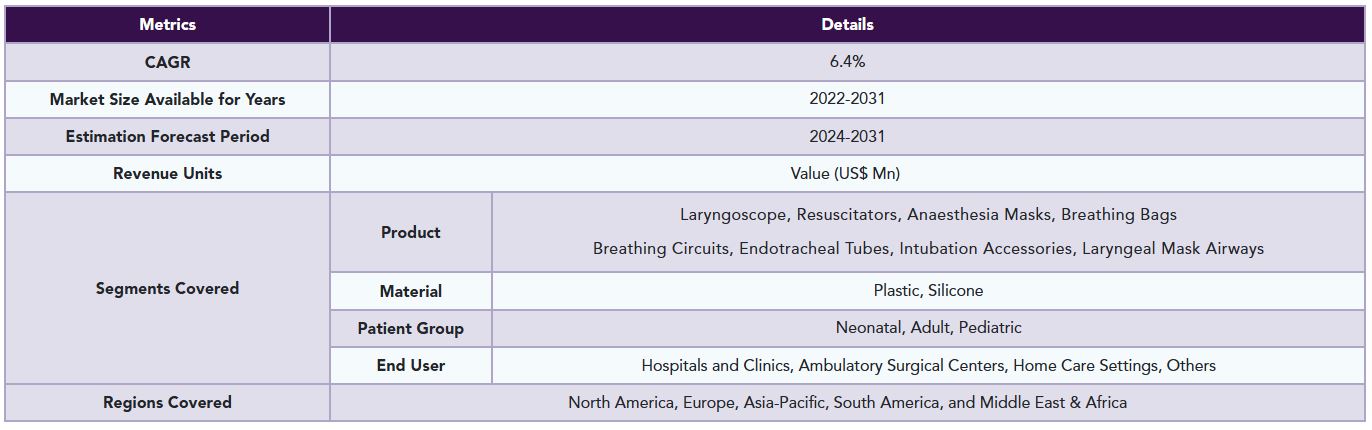

The global anesthesia disposables market reached US$ 1.12 billion in 2023 and is expected to reach US$ 1.83 billion by 2031, growing at a CAGR of 6.4% during the forecast period 2024-2031.

Anesthetic disposables are a category of single-use medical products created primarily for the administration of anesthetic during surgical procedures. These items are critical to guaranteeing patient safety, preventing cross-contamination, and maintaining a sterile environment in operating rooms. The most common forms of anesthetic disposables are anesthesia breathing circuits, endotracheal tubes, anesthesia masks, and laryngeal mask airways. Each of these components is critical to the successful delivery of anesthetic agents as well as the facilitation of airway management and monitoring during surgery.

The increasing prevalence of chronic diseases is the driving factor that drives the market over the forecast period. For instance, according to the Pan American Health Organization, globally, there were an expected 20 million new cancer diagnoses and 10 million cancer deaths. Over the next two decades, the cancer burden will rise by almost 60%, putting a further burden on healthcare systems, individuals, and communities.

Market Dynamics: Drivers & Restraints

Increasing prevalence of chronic diseases

The increasing prevalence of cancer is expected to be a significant factor in the growth of the global anesthesia disposables market. The increasing prevalence of chronic diseases is expected to have a substantial impact on the global anesthesia disposables market. Chronic ailments such as diabetes, hypertension, cardiovascular disease, and respiratory disorders frequently necessitate surgical procedures, resulting in increased demand for anesthetic products. Patients with these chronic disorders have distinct problems during surgery since their health can impair the perioperative procedure. Individuals with diabetes, for example, may experience delayed wound healing and greater susceptibility to infections, while those with cardiovascular disorders are at a higher risk of complications before and after surgery. This intricacy needs expert anesthetic management, which increases the demand for disposable anesthesia equipment that ensures safety and efficacy in these high-risk patients.

For instance, according to the National Institute of Health, in 2023, the United States is expected to see 1,958,310 new cancer cases and 609,820 cancer deaths. Prostate cancer incidence climbed by 3% every year from 2014 to 2019, after two decades of reduction, resulting in an additional 99,000 new cases. The annual cancer incidence rate is 440.5 per 100,000 men and women (based on cases from 2017 to 2021). The cancer death rate (cancer mortality) is 146.0 per 100,000 men and women annually (based on deaths from 2018-2022). In 2024, a projected 14,910 children and adolescents between the ages of 0 and 19 will be diagnosed with cancer, with 1,590 deaths from the condition.

Moreover, according to the National Institute of Health, approximately 462 million individuals were affected by type 2 diabetes corresponding to 6.28% of the world’s population. For instance, according to the Centers for Disease Control and Prevention, approximately 38.4 million individuals of all ages, representing 11.6% of the U.S. population, were diagnosed with diabetes. Among adults aged 18 and older, this figure rose to 38.1 million, accounting for 14.7% of all U.S. adults.

Dearth of trained anaesthesiologists

Factors such as dearth of trained anaesthesiologists are expected to hamper the global anesthesia disposable market. The growing dearth of trained anesthesiologists and certified registered nurse anesthetists (CRNAs) is predicted to have a substantial impact on the worldwide anesthesia disposables industry. This scarcity is a multidimensional issue caused by a number of variables, including an aging workforce and a growing demand for surgery. As healthcare organizations struggle to maintain proper staffing levels in anesthesia departments, the capacity to offer timely and effective surgical care suffers, which has a direct impact on anesthesia disposable consumption.

Segment Analysis

The global anesthesia disposables market is segmented based on product, material, patient group, end user, and region.

Anaesthesia masks segment is expected to dominate the global anesthesia disposables market share

Anaesthesia masks segment is expected to dominate the global anesthesia disposables market share. The anesthesia masks segment is expected to dominate the worldwide anesthesia disposables market due to many compelling considerations that highlight its importance in surgical operations. Anesthesia masks, which are required for administering anesthetic gases and regulating patient breathing, are widely used in a variety of healthcare settings, including hospitals and ambulatory surgical centers. Their critical role in assuring patient safety and comfort during anesthetic administration makes them necessary in modern medical practice.

One of the key drivers of growth in the anesthesia masks industry is the growing number of surgical procedures conducted around the world and the increasing prevalence of chronic diseases. With advances in medical technology and an aging population necessitating surgical operations, the demand for effective anesthetic administration systems has increased. Anesthesia masks provide rapid and efficient ventilation, which is especially important in emergency situations and for patients undergoing short-term procedures. The shift to minimally invasive surgical techniques also contributes to this trend, as these operations frequently necessitate accurate and dependable anesthetic care, reinforcing the importance of anesthesia masks.

The increasing prevalence of chronic diseases results in an increase in the number of surgical procedures which increases the demand for anesthesia masks. For instance, according to the World Health Organization (WHO), cancer diagnoses are predicted to exceed 22 million by 2023 and in the case of breast cancer, 1 in 12 women will be diagnosed with breast cancer in their lifetime and 1 in 71 women die of it.

Geographical Analysis

North America is expected to hold a significant position in the global anesthesia disposables market share

North America is expected to maintain its dominant position in the global anesthetic disposables market due to several key factors. One significant driver is the region's high prevalence of chronic diseases, which results in an increasing number of surgical procedures. Conditions such as cardiovascular diseases, cancer, diabetes, and respiratory disorders are common, leading to a higher volume of procedures that require effective anesthetic management. Consequently, the demand for disposable anesthetic devices—including masks, tubes, and breathing circuits—continues to rise.

For example, according to the National Institutes of Health, the United States is projected to see 2,001,140 new cancer cases and 611,720 cancer-related deaths in 2024. While cancer mortality has decreased overall due to reductions in smoking, earlier detection, and improved treatments, this progress is being overshadowed by a rising incidence of six of the top ten cancers. This growing demand for surgical interventions and anesthetic management will further fuel the need for anesthetic disposables in the region.

Asia Pacific is growing at the fastest pace in the global anesthesia disposables market

Asia Pacific is experiencing the fastest growth in global anesthesia disposables owing to the increasing incidence of chronic diseases in the region. Asia Pacific experiences the greatest growth in the worldwide anesthetic disposables market, owing to a combination of variables that improve surgical capabilities and healthcare access throughout the region. One of the key drivers of this expansion is the increased volume of surgical procedures, which is mostly due to the rising prevalence of chronic conditions. As populations in nations like as China and India age and urbanize, there is an increase in health problems that necessitate surgical procedures. This trend calls for a higher dependence on anesthesia disposables as healthcare providers strive to assure patient safety and reduce infection risks during surgeries. For instance, according to the National Institute of Health, the expected number of cancer cases in India for 2022 is 14,61,427 (crude rate: 100.4 per 100,000). In India, one out of every nine people is likely to develop cancer over his or her lifetime. Males and females were most likely to develop lung and breast cancer, respectively.

Competitive Landscape

The major global players in the global anesthesia disposables market include Ambu A/S, Drägerwerk AG & Co. KGaA, Teleflex Incorporated, Hamilton Medical, Intersurgical Ltd, Medline Industries, LP, Medtronic, Mercury Medical, Sharn Anesthesia, Narang Medical Limited among others.

Emerging Players

Conus Airway, Solvet among others

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global anesthesia disposables market report would provide approximately 53 tables, 47 figures, and 176 pages.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product

3.2. Snippet by Material

3.3. Snippet by Patient Group

3.4. Snippet by End User

3.5. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Increasing Prevalence of Chronic Diseases

4.1.2. Restraints

4.1.2.1. Dearth Of Trained Anaesthesiologists

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter's Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

5.5. Reimbursement Analysis

5.6. Patent Analysis

5.7. SWOT Analysis

5.8. DMI Opinion

6. By Product

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

6.1.2. Market Attractiveness Index, By Product

6.2. Laryngoscope*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Resuscitators

6.4. Anaesthesia Masks

6.5. Breathing Bags

6.6. Breathing Circuits

6.7. Endotracheal Tubes

6.8. Intubation Accessories

6.9. Laryngeal Mask Airways

7. By Material

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

7.1.2. Market Attractiveness Index, By Material

7.2. Plastic*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Silicone

8. By Patient Group

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Patient Group

8.1.2. Market Attractiveness Index, By Patient Group

8.2. Neonatal*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Adult

8.4. Paediatric

9. By End User

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

9.1.2. Market Attractiveness Index, By End User

9.2. Hospitals and Clinics*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Ambulatory Surgical Centers

9.4. Home Care Settings

9.5. Others

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Patient Group

10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.7.1. The U.S.

10.2.7.2. Canada

10.2.7.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Patient Group

10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.7.1. Germany

10.3.7.2. UK

10.3.7.3. France

10.3.7.4. Italy

10.3.7.5. Spain

10.3.7.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Patient Group

10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.7.1. Brazil

10.4.7.2. Argentina

10.4.7.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Patient Group

10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.7.1. China

10.5.7.2. India

10.5.7.3. Japan

10.5.7.4. South Korea

10.5.7.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product

10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Patient Group

10.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Ambu A/S*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. Drägerwerk AG & Co. KGaA

12.3. Teleflex Incorporated

12.4. Hamilton Medical

12.5. Intersurgical Ltd

12.6. Medline Industries, LP

12.7. Medtronic

12.8. Mercury Medical

12.9. Sharn Anesthesia

12.10. Narang Medical Limited

LIST NOT EXHAUSTIVE

13. Appendix

13.1. About Us and Services

13.2. Contact Us

*** 麻酔用使い捨て製品の世界市場に関するよくある質問(FAQ) ***

・麻酔用使い捨て製品の世界市場規模は?

→DataM Intelligence社は2023年の麻酔用使い捨て製品の世界市場規模を11億2000万米ドルと推定しています。

・麻酔用使い捨て製品の世界市場予測は?

→DataM Intelligence社は2031年の麻酔用使い捨て製品の世界市場規模を18億3000万米ドルと予測しています。

・麻酔用使い捨て製品市場の成長率は?

→DataM Intelligence社は麻酔用使い捨て製品の世界市場が2024年~2031年に年平均6.4%成長すると展望しています。

・世界の麻酔用使い捨て製品市場における主要プレイヤーは?

→「Ambu A/S、Drägerwerk AG & Co. KGaA、Teleflex Incorporated、Hamilton Medical、Intersurgical Ltd、Medline Industries、LP、Medtronic、Mercury Medical、Sharn Anesthesia、Narang Medical Limitedなど ...」を麻酔用使い捨て製品市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/