1. 調査手法および範囲

1.1. 調査手法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. スニペットの種類別

3.2. スニペットの素材別

3.3. スニペットの固定タイプ別

3.4. スニペットのテクノロジー別

3.5. エンドユーザー別スニペット

3.6. 地域別スニペット

4. ダイナミクス

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 臓器移植件数の増加

4.1.2. 抑制要因

4.1.2.1. 規制上のハードル

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

5.5. 償還分析

5.6. 特許分析

5.7. SWOT分析

5.8. DMI 意見

6. 種類別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率分析(%)、種類別

6.1.2. 市場魅力度指数、種類別

6.2. 人工臓器*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率分析(%)

6.2.3. 腎臓

6.2.4. 心臓

6.2.5. 肺

6.2.6. 肝臓

6.2.7. 四肢

6.2.8. その他

6.3. 人工生体工学

6.3.1. 人工内耳

6.3.2. 外部骨格

6.3.3. バイオニック・リム

6.3.4. 視覚バイオニクス

6.3.5. 脳バイオニクス

7. 素材別

7.1. はじめに

7.1.1. 素材別市場規模分析および前年比成長率(%)

7.1.2. 素材別市場魅力度指数

7.2. プラスチック*

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率(%)

7.3. 金属

7.4. コラーゲン

7.5. ゼラチン

7.6. フィブリン

7.7. 多糖類

7.8. 合成ポリマー

7.9. その他

8. 固定の種類別

8.1. はじめに

8.1.1. 固定の種類別市場規模および前年比成長率(%)

8.1.2. 固定の種類別市場魅力度指数

8.2. 一時的*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率分析(%)

8.3. 恒久的

9. 技術別

9.1. はじめに

9.1.1. 技術別市場規模分析および前年比成長率分析(%)

9.1.2. 技術別市場魅力度指数

9.2. 機械生体工学*

9.2.1. はじめに

9.2.2. 市場規模分析および前年比成長率分析(%)

9.3. 電子生体工学

10. エンドユーザー別

10.1. はじめに

10.1.1. エンドユーザー別市場規模分析および前年比成長率分析(%)

10.1.2. 市場魅力度指数、エンドユーザー別

10.2. 病院*

10.2.1. はじめに

10.2.2. 市場規模分析および前年比成長率分析(%)

10.3. 専門クリニック

10.4. 学術・研究機関

11. 地域別

11.1. はじめに

11.1.1. 市場規模分析および前年比成長率分析(%)、地域別

11.1.2. 市場魅力度指数、地域別

11.2. 北米

11.2.1. はじめに

11.2.2. 地域特有の主な動向

11.2.3. 市場規模分析および前年比成長率分析(%)、種類別

11.2.4. 市場規模分析および前年比成長率分析(%)、材料別

11.2.5. 市場規模分析および前年比成長率分析(%)、固定タイプ別

11.2.6. 市場規模分析および前年比成長率分析(%)、技術別

11.2.7. エンドユーザー別市場規模分析および前年比成長率(%)

11.2.8. 国別市場規模分析および前年比成長率(%)

11.2.8.1. 米国

11.2.8.2. カナダ

11.2.8.3. メキシコ

11.3. ヨーロッパ

11.3.1. はじめに

11.3.2. 主要地域別の動向

11.3.3. 市場規模分析および前年比成長率分析(%)種類別

11.3.4. 市場規模分析および前年比成長率分析(%)材料別

11.3.5. 市場規模分析および前年比成長率分析(%)固定タイプ別

11.3.6. 市場規模分析および前年比成長率分析(%)、技術別

11.3.7. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

11.3.8. 市場規模分析および前年比成長率分析(%)、国別

11.3.8.1. ドイツ

11.3.8.2. 英国

11.3.8.3. フランス

11.3.8.4. イタリア

11.3.8.5. スペイン

11.3.8.6. ヨーロッパのその他地域

11.4. 南アメリカ

11.4.1. はじめに

11.4.2. 主要地域特有の動向

11.4.3. 種類別市場規模分析および前年比成長率(%)

11.4.4. 材料別市場規模分析および前年比成長率(%)

11.4.5. 固定タイプ別市場規模分析および前年比成長率(%)

11.4.6. 技術別市場規模分析および前年比成長率(%)

11.4.7. エンドユーザー別市場規模分析および前年比成長率(%)

11.4.8. 国別市場規模分析および前年比成長率(%)

11.4.8.1. ブラジル

11.4.8.2. アルゼンチン

11.4.8.3. 南米その他

11.5. アジア太平洋

11.5.1. はじめに

11.5.2. 主要地域別の動向

11.5.3. 市場規模分析および前年比成長率分析(%)種類別

11.5.4. 市場規模分析および前年比成長率分析(%)材料別

11.5.5. 市場規模分析および前年比成長率分析(%)固定タイプ別

11.5.6. 市場規模分析および前年比成長率分析(%)、技術別

11.5.7. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

11.5.8. 市場規模分析および前年比成長率分析(%)、国別

11.5.8.1. 中国

11.5.8.2. インド

11.5.8.3. 日本

11.5.8.4. 韓国

11.5.8.5. アジア太平洋地域その他

11.6. 中東およびアフリカ

11.6.1. はじめに

11.6.2. 主要地域特有の動向

11.6.3. 種類別市場規模分析および前年比成長率(%)

11.6.4. 材料別市場規模分析および前年比成長率(%)

11.6.5. 固定タイプ別市場規模分析および前年比成長率(%)

11.6.6. 技術別市場規模分析および前年比成長率(%)

11.6.7. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

12. 競合状況

12.1. 競合シナリオ

12.2. 市場ポジショニング/シェア分析

12.3. 合併・買収分析

13. 企業プロフィール

Abiomed Inc.(Johnson & Johnson Services, Inc.)

SynCardia Systems, LLC

Medtronic

Boston Scientific Corporation

Zimmer Biomet.

Edwards Lifesciences Corporation.

Jarvik Heart, Inc.

Cochlear Ltd.

Berlin Heart

Ekso Bionics

リストは網羅的ではありません

14. 付録

14.1. 当社およびサービスについて

14.2. お問い合わせ

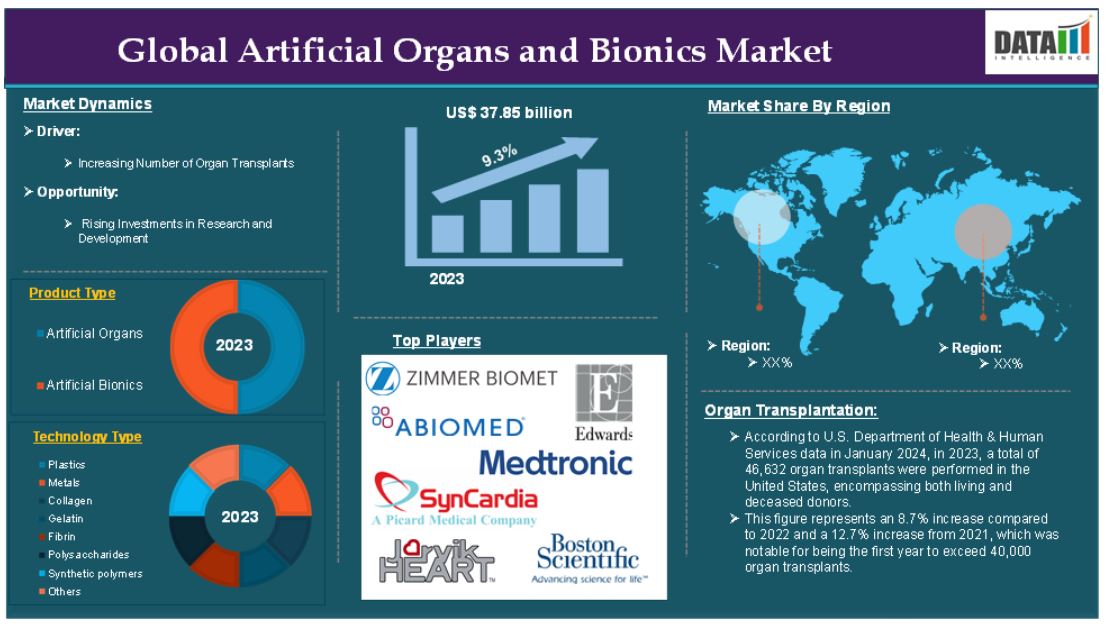

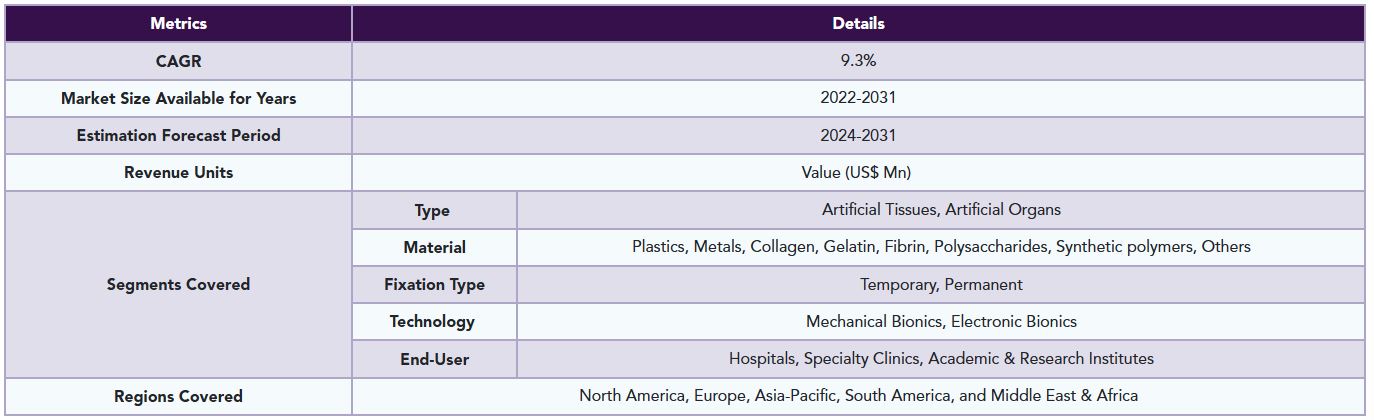

The global artificial organs and bionics market reached US$ 37.85 billion in 2023 and is expected to reach US$ 77.08 billion by 2031, growing at a CAGR of 9.3% during the forecast period 2024-2031.

Artificial organs are human-made devices or tissues that are implanted or integrated into a person’s body to replace, duplicate, or augment the function of a natural organ. These organs interface with living tissue, allowing patients to regain normal functionality and improve their quality of life. Examples include artificial hearts, kidneys, and limbs, which can restore essential bodily functions or enhance physical capabilities.

Bionics, on the other hand, involves the integration of biological systems with electronic components, often resulting in devices that can interact with the nervous system. Bionic devices include prosthetics that can be controlled by neural signals and implants that restore sensory functions, such as cochlear implants for hearing restoration. These factors have driven the global artificial organs and bionics market expansion.

With the growing investments and the rising funding by the government, there is growing research and development of innovative solutions for artificial organs and bionics. For instance, in 2024, BiVacor, a clinical-stage medical device company based in Australia and California, received an award of US$13 million from the Australian Government’s Medical Research Future Fund (MRFF) grant through the Artificial Heart Frontiers Program (AHFP). The funding will support the company’s Total Artificial Heart (TAH) program and future product enhancements.

Market Dynamics: Drivers & Restraints

Increasing number of organ transplants

The increasing number of organ transplants is significantly driving the growth of the global artificial organs and bionics market and is expected to drive throughout the market forecast period. The increasing prevalence of chronic diseases such as diabetes, heart disease, and kidney disorders is a significant factor contributing to the rising incidence of organ failure. This escalation in organ failure cases directly correlates with the growing demand for artificial organs and bionics.

According to U.S. Department of Health & Human Services data in January 2024, in 2023, a total of 46,632 organ transplants were performed in the United States, encompassing both living and deceased donors. This figure represents an 8.7% increase compared to 2022 and a 12.7% increase from 2021, which was notable for being the first year to exceed 40,000 organ transplants. The growth in transplant numbers reflects several important trends and factors within the organ donation and transplantation landscape.

The rising rates of organ failure are increasing the demand for artificial organs as substitutes for traditional transplants. These artificial organs can help fill the void caused by the shortage of available donors, offering life-saving alternatives for patients with severe chronic illnesses.

Regulatory hurdles

Regulatory challenges impose significant obstacles on the artificial organs and bionics sector, affecting the speed and efficiency of product development and entrance. The approval processes for artificial organs and bionic devices are frequently lengthy and complex. Regulatory bodies, such as the FDA in the United States and comparable organizations around the world, need rigorous clinical trials to establish product safety and efficacy before it is commercialized. This can delay the deployment of novel technology and limit patients' timely access to them.

Segment Analysis

The global artificial organs and bionics market is segmented based on type, material, fixation type, technology, end-user and region.

Type:

Artificial Organs segment is expected to dominate the artificial organs and bionics market share

The artificial organs segment is expected to dominate the global artificial organs and bionics market. The artificial organs segment will continue to dominate the artificial organs and bionics market, owing to many compelling factors driving demand and growth in this field. The global prevalence of chronic diseases such as heart disease, diabetes, and kidney failure is rising, resulting in an increased risk of organ failure. This tendency creates a considerable need for artificial organs to replace failing natural organs, driving up demand for this segment.

Furthermore, the aging population contributes to an increase in chronic diseases and organ failures among older persons, raising the demand for artificial organ solutions because these people frequently require replacements for deteriorating organs.

Companies are conducting advanced research and development of artificial organs and are introducing new organs to meet the rising demand. For instance, in January 2022, IIT-Kanpur launched the Hridyantra project, aimed at developing an advanced Left Ventricular Assist Device (LVAD) in collaboration with several hospitals. This initiative is particularly significant for patients suffering from end-stage heart failure, a condition where the heart can no longer pump blood effectively, leading to severe health complications.

Geographical Analysis

North America is expected to hold a significant position in the artificial organs and bionics market share

North America holds a substantial position in the global artificial organs and bionics market and is expected to hold most of the market share. The rising number of organ transplants significantly influences the demand for artificial organs. In the U.S., there are over 104,234 people on the national waiting list as of 2023, with a new person added every ten minutes. This urgent need for organ replacements drives the demand for artificial medical devices as alternatives.

The companies are receiving approvals for a wide range of organs and devices that are being developed innovatively. For instance, in March 2022, Edwards Lifesciences received FDA approval for the MITRIS RESILIA valve, a tissue valve replacement designed for the heart's mitral position. This valve is notable for its innovative design and advanced materials, which aim to improve patient outcomes in mitral valve replacement surgeries. Thus, the above are expected to hold the region in the dominant position in the global artificial organs and bionics market.

Asia-Pacific is growing at the fastest pace in the artificial organs and bionics market

The Asia-Pacific (APAC) region is experiencing the fastest growth rate in the artificial organs and bionics market, owing to the rising research and development of innovative artificial organs and bionics, increasing incidence of chronic diseases, and the rising number of organ failures. For instance, according to the National Institute of Health, India experiences 17,000–18,000 solid organ transplants performed every year. This increase in the number of organ failures increases the need for artificial organs solutions for transplantions.

Competitive Landscape

The major global players in the artificial organs and bionics market include Abiomed Inc. (Johnson & Johnson Services, Inc.), SynCardia Systems, LLC, Medtronic, Boston Scientific Corporation, Zimmer Biomet., Edwards Lifesciences Corporation., Jarvik Heart, Inc., Cochlear Ltd., Berlin Heart and Ekso Bionics among others.

Key Developments

• In October 2023, Edwards received the CE [Conformité Européenne] mark for the valve for mitral replacement surgeries. It was approved by the US Food and Drug Administration (FDA) in March 2022.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global artificial organs and bionics market report delivers a detailed analysis with 60+ key tables, more than 50 visually impactful figures, and 176 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Type

3.2. Snippet by Material

3.3. Snippet by Fixation Type

3.4. Snippet by Technology

3.5. Snippet by End-User

3.6. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Increasing number of organ transplants

4.1.2. Restraints

4.1.2.1. Regulatory hurdles

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter's Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

5.5. Reimbursement Analysis

5.6. Patent Analysis

5.7. SWOT Analysis

5.8. DMI Opinion

6. By Type

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

6.1.2. Market Attractiveness Index, By Type

6.2. Artificial Organs*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.2.3. Kidney

6.2.4. Heart

6.2.5. Lungs

6.2.6. Liver

6.2.7. Limbs

6.2.8. Others

6.3. Artificial Bionics

6.3.1. Cochlear Implant

6.3.2. Exoskeleton

6.3.3. Bionic Limbs

6.3.4. Vision Bionics

6.3.5. Brain Bionics

7. By Material

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

7.1.2. Market Attractiveness Index, By Material

7.2. Plastics*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Metals

7.4. Collagen

7.5. Gelatin

7.6. Fibrin

7.7. Polysaccharides

7.8. Synthetic polymers

7.9. Others

8. By Fixation Type

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Type

8.1.2. Market Attractiveness Index, By Fixation Type

8.2. Temporary*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Permanent

9. By Technology

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

9.1.2. Market Attractiveness Index, By Technology

9.2. Mechanical Bionics*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Electronic Bionics

10. By End-User

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.1.2. Market Attractiveness Index, By End-User

10.2. Hospitals*

10.2.1. Introduction

10.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

10.3. Specialty Clinics

10.4. Academic & Research Institutes

11. By Region

11.1. Introduction

11.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

11.1.2. Market Attractiveness Index, By Region

11.2. North America

11.2.1. Introduction

11.2.2. Key Region-Specific Dynamics

11.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

11.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

11.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Type

11.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

11.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.2.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.2.8.1. The U.S.

11.2.8.2. Canada

11.2.8.3. Mexico

11.3. Europe

11.3.1. Introduction

11.3.2. Key Region-Specific Dynamics

11.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

11.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

11.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Type

11.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

11.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.3.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.3.8.1. Germany

11.3.8.2. UK

11.3.8.3. France

11.3.8.4. Italy

11.3.8.5. Spain

11.3.8.6. Rest of Europe

11.4. South America

11.4.1. Introduction

11.4.2. Key Region-Specific Dynamics

11.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

11.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

11.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Type

11.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

11.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.4.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.4.8.1. Brazil

11.4.8.2. Argentina

11.4.8.3. Rest of South America

11.5. Asia-Pacific

11.5.1. Introduction

11.5.2. Key Region-Specific Dynamics

11.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

11.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

11.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Type

11.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

11.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11.5.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

11.5.8.1. China

11.5.8.2. India

11.5.8.3. Japan

11.5.8.4. South Korea

11.5.8.5. Rest of Asia-Pacific

11.6. Middle East and Africa

11.6.1. Introduction

11.6.2. Key Region-Specific Dynamics

11.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type

11.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Material

11.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Type

11.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

11.6.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

12. Competitive Landscape

12.1. Competitive Scenario

12.2. Market Positioning/Share Analysis

12.3. Mergers and Acquisitions Analysis

13. Company Profiles

13.1. Abiomed Inc (Johnson & Johnson Services, Inc.) *

13.1.1. Company Overview

13.1.2. Product Portfolio and Description

13.1.3. Financial Overview

13.1.4. Key Developments

13.2. SynCardia Systems, LLC

13.3. Medtronic

13.4. Boston Scientific Corporation

13.5. Zimmer Biomet.

13.6. Edwards Lifesciences Corporation.

13.7. Jarvik Heart, Inc.

13.8. Cochlear Ltd.

13.9. Berlin Heart

13.10. Ekso Bionics

LIST NOT EXHAUSTIVE

14. Appendix

14.1. About Us and Services

14.2. Contact Us

*** 人工臓器&生体工学の世界市場に関するよくある質問(FAQ) ***

・人工臓器&生体工学の世界市場規模は?

→DataM Intelligence社は2023年の人工臓器&生体工学の世界市場規模を378.5億米ドルと推定しています。

・人工臓器&生体工学の世界市場予測は?

→DataM Intelligence社は2031年の人工臓器&生体工学の世界市場規模を770.8億米ドルと予測しています。

・人工臓器&生体工学市場の成長率は?

→DataM Intelligence社は人工臓器&生体工学の世界市場が2024年~2031年に年平均9.3%成長すると展望しています。

・世界の人工臓器&生体工学市場における主要プレイヤーは?

→「Abiomed Inc.(Johnson & Johnson Services, Inc.)、SynCardia Systems, LLC、Medtronic、Boston Scientific Corporation、Zimmer Biomet.、Edwards Lifesciences Corporation.、Jarvik Heart, Inc.、Cochlear Ltd.、Berlin Heart、Ekso Bionicsなど ...」を人工臓器&生体工学市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/