1. 調査方法および範囲

1.1. 調査方法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品種類別抜粋

3.2. 技術別抜粋

3.3. 用途別抜粋

3.4. エンドユーザー別抜粋

3.5. 地域別

4. ダイナミクス

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 幹細胞研究の進歩

4.1.1.2. XX

4.2. 抑制要因

4.2.1.1. 製造コストの高さ

4.3. 機会

4.3.1. 影響分析

5. 業界分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

6. 製品タイプ別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率(%)分析、製品タイプ別

6.1.2. 製品種類別市場魅力度指数

6.2. 細胞培養製品*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率分析(%)

6.3. 非細胞培養製品

7. 技術別

7.1. はじめに

7.1.1. 市場規模分析および前年比成長率(%)、技術別

7.1.2. 市場魅力度指数、技術別

7.2. エクスビボ培養*

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率(%)

7.3. インビボ遺伝子改変

7.4. 3Dバイオプリンティング

7.5. ナノテクノロジー

7.6. CRISPRおよびゲノム編集

7.7. 足場ベースの処置

8. 用途別

8.1. はじめに

8.1.1. 用途別市場規模分析および前年比成長率(%)

8.1.2. 用途別市場魅力度指数

8.2. 皮膚科 *

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率分析(%)

8.3. 筋骨格系

8.4. 免疫学および炎症

8.5. 腫瘍学

8.6. 循環器

8.7. 眼科

8.8. その他

9. エンドユーザー別

9.1. はじめに

9.1.1. エンドユーザー別市場規模分析および前年比成長率(%)

9.1.2. エンドユーザー別市場魅力度指数

9.2. 病院およびクリニック*

9.2.1. はじめに

9.2.2. 市場規模分析および前年比成長率(%)

9.3. 研究機関

9.4. 製薬およびバイオテクノロジー企業

9.5. 学術機関

9.6. 医薬品開発業務受託機関(CRO)

10. 地域別

10.1. はじめに

10.1.1. 地域別市場規模分析および前年比成長率分析(%)

10.1.2. 地域別市場魅力度指数

10.2. 北米

10.2.1. はじめに

10.2.2. 地域特有の主な動向

10.2.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.2.4. 市場規模分析および前年比成長率分析(%)、技術別

10.2.5. 用途別市場規模分析および前年比成長率(%)

10.2.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.2.7. 国別市場規模分析および前年比成長率(%)

10.2.7.1. 米国

10.2.7.2. カナダ

10.2.7.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 地域別の主な動向

10.3.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.3.4. 市場規模分析および前年比成長率分析(%)、技術別

10.3.5. 用途別市場規模分析および前年比成長率(%)

10.3.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.3.7. 国別市場規模分析および前年比成長率(%)

10.3.7.1. ドイツ

10.3.7.2. イギリス

10.3.7.3. フランス

10.3.7.4. スペイン

10.3.7.5. イタリア

10.3.7.6. ヨーロッパのその他地域

10.4. 南アメリカ

10.4.1. はじめに

10.4.2. 主要地域特有の動向

10.4.3. 製品種類別市場規模分析および前年比成長率(%)

10.4.4. 技術別市場規模分析および前年比成長率(%)

10.4.5. 用途別市場規模分析および前年比成長率(%)

10.4.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.4.7. 市場規模の分析と前年比成長率の分析(%)、国別

10.4.7.1. ブラジル

10.4.7.2. アルゼンチン

10.4.7.3. 南米のその他地域

10.5. アジア太平洋地域

10.5.1. はじめに

10.5.2. 主要地域特有の動向

10.5.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.5.4. 市場規模分析および前年比成長率分析(%)、技術別

10.5.5. 市場規模分析および前年比成長率分析(%)、用途別

10.5.6. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

10.5.7. 市場規模分析および前年比成長率分析(%)、国別

10.5.7.1. 中国

10.5.7.2. インド

10.5.7.3. 日本

10.5.7.4. 韓国

10.5.7.5. アジア太平洋地域その他

10.6. 中東およびアフリカ

10.6.1. はじめに

10.6.2. 地域別主要動向

10.6.3. 製品種類別市場規模分析および前年比成長率(%)

10.6.4. 技術別市場規模分析および前年比成長率(%)

10.6.5. 用途別市場規模分析および前年比成長率(%)

10.6.6. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

10.6.7. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

11. 競合状況

11.1. 競合シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. 合併・買収分析

12. 企業プロフィール

Astellas Pharma Inc

Thermo Fisher Scientific Inc.

Smith & Nephew plc

Integra LifeSciences Holdings Corporation

Organogenesis Holdings Inc

Stryker Corporation

Amgen Inc.

F. Hoffmann, Roche Ltd

Baxter International Inc

Vertex Pharmaceuticals Incorporated

(リストは網羅的ではありません)

12. 付録

12.1 当社およびサービスについて

12.2 お問い合わせ

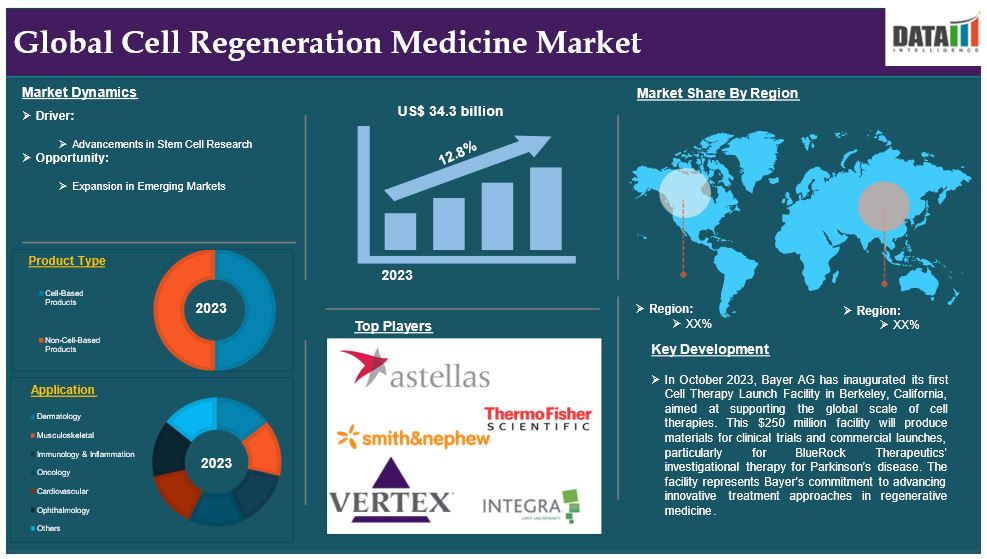

The global cell regeneration medicine market reached US$ 34.3 billion in 2023 and is expected to reach US$ 90.1 billion by 2031, growing at a CAGR of 12.8% during the forecast period 2024-2031.

Cell regeneration medicine is a medical science that uses biology, biotechnology, and tissue engineering to repair, replace, or regenerate damaged cells, tissues, and organs to restore normal function. It uses cell-based therapies like stem cells, gene therapies, and tissue-engineered products to address various diseases like neurodegenerative disorders, cardiovascular diseases, orthopedic injuries, and cancer. This approach has transformative potential for improving patient outcomes, extending healthy lifespans, and reducing chronic illness burden.

Market Dynamics: Drivers & Restraints

Advancements in Stem Cell Research

Improving technology in stem cell research and its rapid advancement into clinical translation is one of the primary factors driving the market for global cell regeneration medicine. Stem cells, especially induced pluripotent stem cells (iPSCs) and mesenchymal stem cells (MSCs), have shown great promise in treating medical conditions ranging from neurodegenerative diseases and cardiovascular events to musculoskeletal damage and chronic wounds.

Breakthroughs in the understanding of stem cell biology, better methods of culturing and differentiating stem cells, and improved novel delivery systems contribute to the fast acceptance of regenerative medicine therapies. Regulatory frameworks, including, among others, fast-track by the U.S. FDA and EMA, add to the stem-cell-based therapies pipeline, thus facilitating a faster approval process for entering the market.

Additionally, increased academic-biotech partnerships-which promote innovation and commercialization-also play a significant role in expanding the application spectrum at the end and driving upward trends in the market. Thus, these combinations of research, regulatory support, and commercial interest drive the global adoption of cell regeneration therapies.

High Production Cost

The Global Cell Regeneration Medicine Market is hindered by high production costs and complex manufacturing procedures, particularly for cell-based therapies like stem-cells. These therapies require stringent licensing and regulatory standards, and advanced technologies like 3D bioprinting and gene editing increase production costs. Logistical challenges, storage, transport, and administration costs also contribute to the overall expenses. Limited infrastructure and expertise in emerging markets also hinder widespread adoption. Affordable regenerative medicine remains a critical issue for health systems in low- and middle-income countries, limiting market penetration and accessibility.

Segment Analysis

The global cell regeneration medicine market is segmented based on product type, technology, application, end user and region.

Product type:

Cell-Based Products segment is expected to dominate the cell regeneration medicine market share

The cell-based products segment holds a major portion of the cell regeneration medicine market share and is expected to continue to hold a significant portion of the cell regeneration medicine market share during the forecast period.

Cell-based products are a key part of the regenerative medicine market, utilizing live cells like stem cells and progenitor cells to promote tissue repair and regeneration. These therapies address the root cause of cellular damage, offering a targeted approach to complex diseases like neurodegenerative disorders, cardiovascular conditions, and autoimmune diseases. Autologous products, derived from patients' own cells, minimize immune rejection risk, while allogeneic products, sourced from donors, offer scalable solutions for mass treatments. Advancements in cryopreservation, biomanufacturing, and gene editing have enhanced the efficacy and reliability of cell-based therapies. These products are revolutionizing chronic and degenerative conditions management, enabling personalized and curative treatment options.

For instance, in July 2024, Bioserve India is launched advanced stem cell products from REPROCELL, aiming to support scientific research, drug development, regenerative medicine, and therapeutic discovery in the Indian market. The rapidly growing stem cell market includes various industries involved in research, development, manufacturing, and distribution of stem cell therapy products, contributing to the advancements in the Indian market.

Application:

Oncology segment is the fastest-growing segment in cell regeneration medicine market share

The oncology segment is the fastest-growing segment in the cell regeneration medicine market share and is expected to hold the market share over the forecast period.

The oncology segment is revolutionizing the Global Cell Regeneration Medicine Market by utilizing cell-based therapies and regenerative technologies to address cancer treatment. Regenerative medicine focuses on repairing tissue damage caused by tumors or treatments, targeting cancer at the cellular level to prevent recurrence. Innovations like immune cell-based therapies, such as CAR-T cells and TILs, have redefined cancer care by enhancing the immune system's ability to recognize and destroy malignant cells. Stem cell-based approaches are also used for bone marrow transplants and reconstructive applications. With a focus on personalized medicine and immunotherapy, the oncology segment is driving significant advancements in cell regeneration, offering hope for improved survival rates and quality of life for cancer patients worldwide.

For instance, in April 2024, Stanford, UCLA and City of Hope have received a $10.2 Billion grant from the California Institute for Regenerative Medicine (CIRM) to fund their phase I clinical trial, "Stem-Derived IL13Ra2 Chimeric Antigen Receptor (CAR) T Cells for Patients with Melanoma and Advanced Solid Tumors." The grant, awarded to Dr. Anusha Kalbasi, Dr. Antoni Ribas, and Christine Brown, supports the team's research into a new immunotherapy treatment using CAR T-cells to treat patients with tumors expressing IL13Ra2, a protein target common in melanoma, thyroid cancers, and rare tumor types.

Geographical Analysis

North America is expected to hold a significant position in the cell regeneration medicine market share

North America holds a substantial position in the cell regeneration medicine market and is expected to hold most of the market share due to its robust healthcare infrastructure, high investment in research and development, and favorable regulatory environments. The US, a leader in regenerative medicine, has expedited the approval process for cell-based therapies through initiatives like the Orphan Drug Act and regenerative medicine advanced therapy designation.

Moreover, the presence of world-renowned research institutions and biotech companies accelerates innovation in stem cell research and gene therapies. The increasing prevalence of chronic diseases and demand for personalized medicine also drive the adoption of regenerative therapies. North America's high healthcare spending and focus on advanced treatments make it a critical market for cell regeneration medicine.

For instance, in July 2024, Longeveron Inc., a biotechnology company, has received Regenerative Medicine Advanced Therapy (RMAT) designation from the FDA for its proprietary, scalable, allogeneic cellular investigational therapy, Lomecel-B™, for the treatment of mild Alzheimer's Disease. The therapy is being evaluated across multiple indications, including Alzheimer's Disease, Aging-related Frailty, and hypoplastic left heart syndrome. Lomecel-B is the first cellular therapeutic candidate to receive RMAT designation for Alzheimer's Disease.

Europe is growing at the fastest pace in the cell regeneration Medicine market

Europe holds the fastest pace in the cell regeneration medicine market and is expected to hold most of the market share due to scientific advancements, regulatory support, and increasing demand for innovative therapies for age-related and degenerative diseases. The European Medicines Agency (EMA) has facilitated regenerative therapies approval, encouraging investment in clinical trials and commercialization. The region's aging population, particularly in Germany, Italy, and France, drives the demand for therapies. Government funding and favorable reimbursement policies in several European countries further support the market's expansion, highlighting the importance of collaboration between academic institutions, biotechnology companies, and healthcare providers.

Competitive Landscape

The major global players in the cell regeneration medicine market include Astellas Pharma Inc, Thermo Fisher Scientific Inc., Smith & Nephew plc, Integra LifeSciences Holdings Corporation, Organogenesis Holdings Inc, Stryker Corporation, Amgen Inc., F. Hoffmann, Roche Ltd, Baxter International Inc, Vertex Pharmaceuticals Incorporated and among others.

Emerging Players

The emerging players in the cell regeneration medicine market include BlueRock Therapeutics, Century Therapeutics, Fate Therapeutics, Inc., Caribou Biosciences, Inc and among others

Key Developments

• In October 2023, Bayer AG has inaugurated its first Cell Therapy Launch Facility in Berkeley, California, aimed at supporting the global scale of cell therapies. This $250 Billion facility will produce materials for clinical trials and commercial launches, particularly for BlueRock Therapeutics' investigational therapy for Parkinson’s disease. The facility represents Bayer's commitment to advancing innovative treatment approaches in regenerative medicine.

• In June 2024, Cryoport, a life sciences company, and Minaris Regenerative Medicine, a contract development and manufacturing organization for cell and gene therapies, have formed a strategic partnership to offer integrated logistics and manufacturing services to biotechnology and pharmaceutical companies for regenerative medicine products. The partnership combines Cryoport's logistics expertise and Minaris' expertise in contract manufacturing of regenerative medicine products, including stem cells, gene therapy, biomaterials, and engineered tissue.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global cell regeneration medicine market report delivers a detailed analysis with 60+ key tables, more than 50 visually impactful figures, and 176 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

Table of Contents

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product Type

3.2. Snippet by Technology

3.3. Snippet by Application

3.4. Snippet by End User

3.5. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Advancements in Stem Cell Research

4.1.1.2. XX

4.2. Restraints

4.2.1.1. High Production Cost

4.3. Opportunity

4.3.1. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

6. By Product type

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product type

6.1.2. Market Attractiveness Index, By Product type

6.2. Cell-Based Products*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Non-Cell-Based Products

7. By Technology

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

7.1.2. Market Attractiveness Index, By Technology

7.2. Ex Vivo Culture*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. In Vivo Gene Modification

7.4. 3D Bioprinting

7.5. Nanotechnology

7.6. CRISPR and Genome Editing

7.7. Scaffold-Based Techniques

8. By Application

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

8.1.2. Market Attractiveness Index, By Application

8.2. Dermatology *

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Musculoskeletal

8.4. Immunology & Inflammation

8.5. Oncology

8.6. Cardiovascular

8.7. Ophthalmology

8.8. Others

9. By End User

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

9.1.2. Market Attractiveness Index, By End User

9.2. Hospitals and Clinics*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Research Institutes

9.4. Pharmaceutical and Biotechnology Companies

9.5. Academic Institutes

9.6. Contract Research Organizations (CROs)

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.7.1. U.S.

10.2.7.2. Canada

10.2.7.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.7.1. Germany

10.3.7.2. U.K.

10.3.7.3. France

10.3.7.4. Spain

10.3.7.5. Italy

10.3.7.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.7.1. Brazil

10.4.7.2. Argentina

10.4.7.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.7.1. China

10.5.7.2. India

10.5.7.3. Japan

10.5.7.4. South Korea

10.5.7.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10.6.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Astellas Pharma Inc *

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. Thermo Fisher Scientific Inc.

12.3. Smith & Nephew plc

12.4. Integra LifeSciences Holdings Corporation

12.5. Organogenesis Holdings Inc.

12.6. Stryker Corporation

12.7. Amgen Inc.

12.8. F. Hoffmann-La Roche Ltd

12.9. Baxter International Inc

12.10. Vertex Pharmaceuticals Incorporated (LIST NOT EXHAUSTIVE)

12. Appendix

12.1 About Us and Services

12.2 Contact Us

*** 細胞再生医療の世界市場に関するよくある質問(FAQ) ***

・細胞再生医療の世界市場規模は?

→DataM Intelligence社は2023年の細胞再生医療の世界市場規模を343億米ドルと推定しています。

・細胞再生医療の世界市場予測は?

→DataM Intelligence社は2031年の細胞再生医療の世界市場規模を901億米ドルと予測しています。

・細胞再生医療市場の成長率は?

→DataM Intelligence社は細胞再生医療の世界市場が2024年~2031年に年平均12.8%成長すると展望しています。

・世界の細胞再生医療市場における主要プレイヤーは?

→「Astellas Pharma Inc、Thermo Fisher Scientific Inc.、Smith & Nephew plc、Integra LifeSciences Holdings Corporation、Organogenesis Holdings Inc、Stryker Corporation、Amgen Inc.、F. Hoffmann, Roche Ltd、Baxter International Inc、Vertex Pharmaceuticals Incorporatedなど ...」を細胞再生医療市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/