1. 調査手法および範囲

1.1. 調査手法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品種類別抜粋

3.2. 用途別抜粋

3.3. エンドユーザー別抜粋

3.4. 地域別抜粋

4. ダイナミクス

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 低侵襲処置への好みの高まり

4.1.1.2. 内視鏡システムの技術的進歩

4.1.2. 抑制要因

4.1.2.1. 軟性内視鏡の高コスト

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 特許分析

5.5. 規制分析

5.6. SWOT分析

5.7. 未充足ニーズ

6. 製品種類別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率分析(%)、種類別

6.1.2. 市場魅力度指数、種類別

6.2. 胃内視鏡*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率分析(%)

6.3. 大腸内視鏡

6.4. 腸内視鏡

6.5. 十二指腸内視鏡

6.6. 気管支鏡

6.7. 食道内視鏡

6.8. その他

7. 用途別

7.1. はじめに

7.1.1. 用途別市場規模および前年比成長率(%)

7.1.2. 用途別市場魅力度指数

7.2. 消化器科*

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率分析(%)

7.3. 呼吸器科

7.4. 婦人科

7.5. 泌尿器科

7.6. その他

8. エンドユーザー別

8.1. はじめに

8.1.1. エンドユーザー別市場規模分析および前年比成長率(%)

8.1.2. エンドユーザー別市場魅力度指数

8.2. 病院*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率(%)

8.3. 専門クリニック

8.4. 外来外科センター

8.5. 診断センター

8.6. その他

9. 地域別

9.1. はじめに

9.1.1. 地域別市場規模分析および前年比成長率分析(%)

9.1.2. 地域別市場魅力度指数

9.2. 北米

9.2.1. はじめに

9.2.2. 主要地域別ダイナミクス

9.2.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.2.4. 市場規模分析および前年比成長率分析(%)、用途別

9.2.5. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

9.2.6. 国別の市場規模分析および前年比成長率分析(%)

9.2.6.1. 米国

9.2.6.2. カナダ

9.2.6.3. メキシコ

9.3. ヨーロッパ

9.3.1. はじめに

9.3.2. 主要地域別の動向

9.3.3. 製品種類別市場規模分析および前年比成長率(%)

9.3.4. 用途別市場規模分析および前年比成長率(%)

9.3.5. エンドユーザー別市場規模分析および前年比成長率(%)

9.3.6. 国別市場規模分析および前年比成長率(%)

9.3.6.1. ドイツ

9.3.6.2. 英国

9.3.6.3. フランス

9.3.6.4. スペイン

9.3.6.5. イタリア

9.3.6.6. ヨーロッパのその他地域

9.4. 南アメリカ

9.4.1. はじめに

9.4.2. 主要地域別の動向

9.4.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.4.4. 市場規模分析および前年比成長率分析(%)、用途別

9.4.5. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

9.4.6. 国別の市場規模分析および前年比成長率分析(%)

9.4.6.1. ブラジル

9.4.6.2. アルゼンチン

9.4.6.3. 南米のその他地域

9.5. アジア太平洋

9.5.1. はじめに

9.5.2. 主要地域特有のダイナミクス

9.5.3. 製品種類別市場規模分析および前年比成長率(%)

9.5.4. 用途別市場規模分析および前年比成長率(%)

9.5.5. エンドユーザー別市場規模分析および前年比成長率(%)

9.5.6. 国別市場規模分析および前年比成長率(%)

9.5.6.1. 中国

9.5.6.2. インド

9.5.6.3. 日本

9.5.6.4. 韓国

9.5.6.5. アジア太平洋地域その他

9.6. 中東およびアフリカ

9.6.1. はじめに

9.6.2. 主要地域特有の動向

9.6.3. 製品種類別市場規模分析および前年比成長率(%)

9.6.4. 用途別市場規模分析および前年比成長率(%)

9.6.5. エンドユーザー別市場規模分析および前年比成長率(%)

10. 競合状況

10.1. 競合シナリオ

10.2. 市場ポジショニング/シェア分析

10.3. 合併・買収分析

11. 企業プロフィール

Becton

Dickinson and Company

KARL STORZ

Olympus Corporation

FUJIFILM Holdings Corporation

Boston Scientific Corporation

Richard Wolf GmbH

ATMOS MedizinTechnik GmbH & Co. KG

LABORIE MEDICAL TECHNOLOGIES CORP.

EndoMed Systems GmbH

Entermed

リストは網羅的なものではありません。

12. 付録

12.1. 当社およびサービスについて

12.2. お問い合わせ

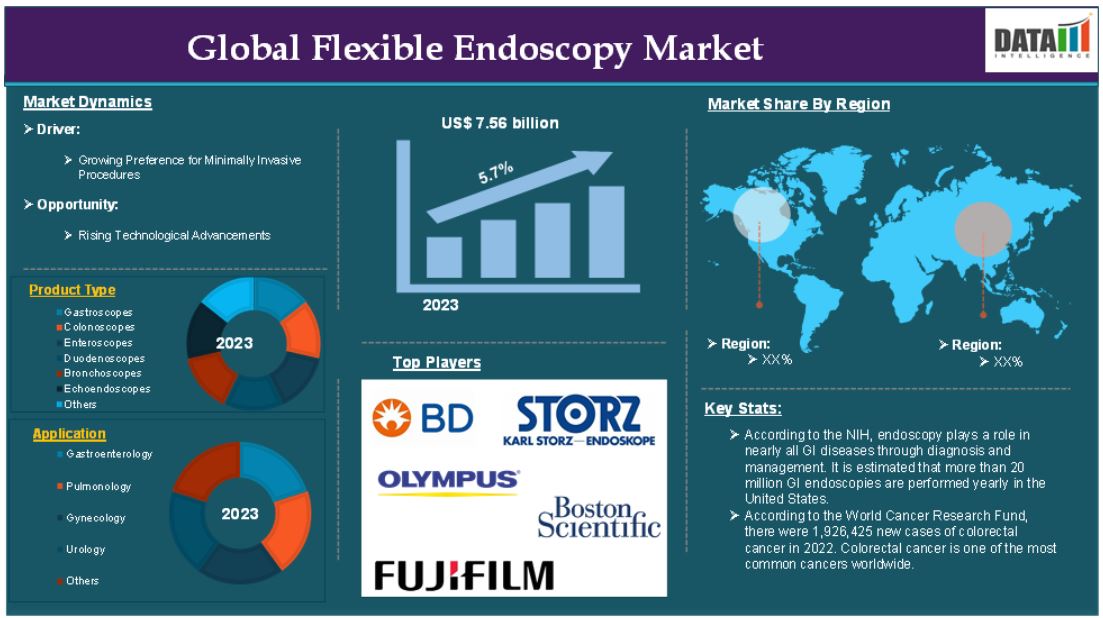

The global flexible endoscopy market reached US$ 7.56 billion in 2023 and is expected to reach US$ 11.73 billion by 2031, growing at a CAGR of 5.7% during the forecast period 2024-2031.

Flexible endoscopy is a medical procedure that involves the use of a flexible, long and thin tube known as an endoscope to visually examine the internal organs and cavities of the body. This technique allows healthcare professionals to diagnose, treat or monitor various conditions without the need for large incisions, making it a form of minimally invasive surgery. The endoscope is equipped with a light source, a camera and sometimes instrument channels to perform interventions. Unlike traditional surgery, flexible endoscopy involves smaller incisions or no incisions at all, reducing risks, pain and recovery time for patients.

The flexible endoscopy market is experiencing significant demand across a variety of medical specialties, driven by factors such as increasing incidence of chronic diseases, advancements in endoscopic technology, growing adoption of minimally invasive procedures and rising healthcare awareness globally. GI disorders, including colorectal cancer, inflammatory bowel disease (IBD) and gastroesophageal reflux disease (GERD), are major drivers for the demand for flexible endoscopy. For instance, according to the NIH, through diagnosis and management, endoscopy plays a role in nearly all GI diseases. It is estimated that more than 20 million GI endoscopies are performed yearly in the United States.

Market Dynamics: Drivers & Restraints

Growing preference for minimally invasive procedures

Growing preference for minimally invasive procedures is significantly driving the growth of the flexible endoscopy market and is expected to drive the market over the forecast period. Minimally invasive procedures performed using flexible endoscopes require smaller incisions or no incisions at all, resulting in less trauma to the body. This leads to faster recovery and reduced pain for patients compared to traditional surgeries.

For instance, in colonoscopy, the procedure involves a flexible endoscope inserted through the rectum. Patients typically recover much faster and with less discomfort than if they underwent an open surgery for colon cancer diagnosis.

The flexible endoscope is increasingly used in cancer screening, such as colonoscopy for colorectal cancer, which is a key application of minimally invasive procedures. Early detection and removal of precancerous growths reduce the need for more invasive treatments later on, making flexible endoscopy a preferred choice.

For instance, according to the World Cancer Research Fund, there were 1,926,425 new cases of colorectal cancer in 2022. Colorectal cancer is one of the most common cancers worldwide. Screening with colonoscopy allows for early detection and polyp removal, preventing the need for more invasive treatments.

High cost of flexible endoscopy

The high cost of flexible endoscopy is a significant factor hampering the growth of the flexible endoscopy market, as it presents challenges for both healthcare providers and patients. Several aspects of these costs including equipment purchase, maintenance and procedural expenses impact the accessibility and affordability of endoscopic procedures, limiting their widespread adoption.

Flexible endoscopes are sophisticated devices that require high-quality components, such as high-definition cameras, fiber-optic cables, light sources and advanced image processing systems. These features contribute to the high purchase cost of endoscopy equipment, depending on the specifications. For instance, according to Boston Scientific, the overall cost of reprocessing one flexible endoscope ranged from $114.07 to $280.71.

Segment Analysis

The global flexible endoscopy market is segmented based on product type, application, end-user and region.

Application:

The gastroenterology segment is expected to dominate the global flexible endoscopy market share

The gastroenterology segment holds a major portion of the flexible endoscopy market share and is expected to continue to hold a significant portion of the market share over the forecast period primarily driven by the high prevalence of gastrointestinal (GI) disorders, the increasing demand for early detection and screening of GI diseases and the use of minimally invasive procedures for both diagnostic and therapeutic purposes.

Gastrointestinal disorders, including colorectal cancer, irritable bowel syndrome (IBS), gastroesophageal reflux disease (GERD), and inflammatory bowel disease (IBD) are widespread globally. Flexible endoscopy plays a crucial role in diagnosing and managing these conditions, making gastroenterology the largest segment in the market.

For instance, according to the World Gastroenterology Organisation, While GI diseases remained very common (incidence 7.3 billion cases - largely due to enteric infections) and important (8 million deaths – cirrhosis a major factor) prevalence remained stable. Overall, 49% of females and 36.6% of males met the criteria for at least one functional gastrointestinal disorder - the most common disorders in all regions being functional constipation, functional dyspepsia, proctalgia fugax, functional diarrhea and IBS at prevalence rates of 11.7%, 7.2%, 5.9%, 4.7% and 4.1, respectively.

Additionally, Colorectal cancer (CRC) is one of the most common cancers worldwide, with about 1,926,425 new cases of colorectal cancer in 2022, and colonoscopy remains the gold standard for early detection. Flexible sigmoidoscopy and colonoscopy are key procedures used in the diagnosis and prevention of colorectal cancer.

North America is expected to hold a significant position in the global flexible endoscopy market

North America region is expected to hold the largest market share over the forecast period. North America, particularly the United States, is known for its state-of-the-art healthcare infrastructure, which includes hospitals, clinics and diagnostic centers equipped with the latest medical technologies, including advanced flexible endoscopes. The widespread adoption of high-definition flexible endoscopes, AI-assisted colonoscopy systems and robotic-assisted endoscopy technologies has significantly enhanced the accuracy and efficacy of endoscopic procedures in North America.

North America has some of the highest healthcare spending globally, particularly in the United States. For instance, according to the U.S. Centers for Medicare & Medicaid Services, U.S. healthcare spending grew 4.1 percent in 2022, reaching $4.5 trillion or $13,493 per person. As a share of the nation's Gross Domestic Product, health spending accounted for 17.3 percent. This high spending allows for the procurement of advanced medical devices, including flexible endoscopes.

North America has well-established cancer screening programs, particularly for colorectal cancer. The U.S. Preventive Services Task Force and other healthcare bodies recommend regular colonoscopy screenings for individuals over the age of 50. These screenings contribute significantly to the volume of flexible endoscopy procedures performed in the region.

For instance, according to the National Institute of Health, in the United States, the most commonly used colorectal cancer screening test was colonoscopy, with an estimated 61% of adults aged 50-75 years reporting colonoscopy use within the past 10 years, further fueling the demand for flexible endoscopy in the region.

Asia Pacific is growing at the fastest pace in the flexible endoscopy market

The Asia Pacific region is experiencing the fastest growth in the flexible endoscopy market. The prevalence of gastrointestinal diseases such as colorectal cancer (CRC), gastroesophageal reflux disease (GERD) and inflammatory bowel diseases (IBD) is rising in the Asia Pacific region, leading to an increased demand for flexible endoscopic procedures.

For instance, in China, colorectal cancer is also one of the most commonly diagnosed cancers. A recent study showed that colorectal cancer ranks second in incidence and fourth in mortality, with 408,000 cases and 196,000 deaths, and remains a major public health problem, this growing incidence of GI cancers drives demand for early detection through colonoscopy and other endoscopic procedures.

Competitive Landscape

The major global players in the flexible endoscopy market Becton, Dickinson and Company, KARL STORZ, Olympus Corporation, FUJIFILM Holdings Corporation, Boston Scientific Corporation, Richard Wolf GmbH, ATMOS MedizinTechnik GmbH & Co. KG, LABORIE MEDICAL TECHNOLOGIES CORP., EndoMed Systems GmbH, Entermed and among others.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global flexible endoscopy market report would provide approximately 62 tables, 53 figures and 197 pages.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product Type

3.2. Snippet by Application

3.3. Snippet by End-User

3.4. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Growing Preference for Minimally Invasive Procedures

4.1.1.2. Technological Advancements in Endoscopic Systems

4.1.2. Restraints

4.1.2.1. High Cost of Flexible Endoscopy

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Patent Analysis

5.5. Regulatory Analysis

5.6. SWOT Analysis

5.7. Unmet Needs

6. By Product Type

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

6.1.2. Market Attractiveness Index, By Product Type

6.2. Gastroscopes*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Colonoscopes

6.4. Enteroscopes

6.5. Duodenoscopes

6.6. Bronchoscopes

6.7. Echoendoscopes

6.8. Others

7. By Application

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

7.1.2. Market Attractiveness Index, By Application

7.2. Gastroenterology*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Pulmonology

7.4. Gynecology

7.5. Urology

7.6. Others

8. By End-User

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

8.1.2. Market Attractiveness Index, By End-User

8.2. Hospitals*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Specialty Clinics

8.4. Ambulatory Surgical Centers

8.5. Diagnostic Centers

8.6. Others

9. By Region

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

9.1.2. Market Attractiveness Index, By Region

9.2. North America

9.2.1. Introduction

9.2.2. Key Region-Specific Dynamics

9.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.2.6.1. U.S.

9.2.6.2. Canada

9.2.6.3. Mexico

9.3. Europe

9.3.1. Introduction

9.3.2. Key Region-Specific Dynamics

9.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.3.6.1. Germany

9.3.6.2. U.K.

9.3.6.3. France

9.3.6.4. Spain

9.3.6.5. Italy

9.3.6.6. Rest of Europe

9.4. South America

9.4.1. Introduction

9.4.2. Key Region-Specific Dynamics

9.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.4.6.1. Brazil

9.4.6.2. Argentina

9.4.6.3. Rest of South America

9.5. Asia-Pacific

9.5.1. Introduction

9.5.2. Key Region-Specific Dynamics

9.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.5.6.1. China

9.5.6.2. India

9.5.6.3. Japan

9.5.6.4. South Korea

9.5.6.5. Rest of Asia-Pacific

9.6. Middle East and Africa

9.6.1. Introduction

9.6.2. Key Region-Specific Dynamics

9.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10. Competitive Landscape

10.1. Competitive Scenario

10.2. Market Positioning/Share Analysis

10.3. Mergers and Acquisitions Analysis

11. Company Profiles

11.1. Becton, Dickinson and Company*

11.1.1. Company Overview

11.1.2. Product Portfolio and Description

11.1.3. Financial Overview

11.1.4. Key Developments

11.2. KARL STORZ

11.3. Olympus Corporation

11.4. FUJIFILM Holdings Corporation

11.5. Boston Scientific Corporation

11.6. Richard Wolf GmbH

11.7. ATMOS MedizinTechnik GmbH & Co. KG

11.8. LABORIE MEDICAL TECHNOLOGIES CORP.

11.9. EndoMed Systems GmbH

11.10. Entermed

LIST NOT EXHAUSTIVE

12. Appendix

12.1. About Us and Services

12.2. Contact Us

*** 軟性内視鏡の世界市場に関するよくある質問(FAQ) ***

・軟性内視鏡の世界市場規模は?

→DataM Intelligence社は2023年の軟性内視鏡の世界市場規模を75.6億米ドルと推定しています。

・軟性内視鏡の世界市場予測は?

→DataM Intelligence社は2031年の軟性内視鏡の世界市場規模を117.3億米ドルと予測しています。

・軟性内視鏡市場の成長率は?

→DataM Intelligence社は軟性内視鏡の世界市場が2024年~2031年に年平均5.7%成長すると展望しています。

・世界の軟性内視鏡市場における主要プレイヤーは?

→「Becton、Dickinson and Company、KARL STORZ、Olympus Corporation、FUJIFILM Holdings Corporation、Boston Scientific Corporation、Richard Wolf GmbH、ATMOS MedizinTechnik GmbH & Co. KG、LABORIE MEDICAL TECHNOLOGIES CORP.、EndoMed Systems GmbH、Entermedなど ...」を軟性内視鏡市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/