1. 調査手法および対象範囲

1.1. 調査手法

1.2. 調査目的およびレポートの対象範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 膝関節置換術による抜粋

3.2. 股関節置換術による抜粋

3.3. 固定方法による抜粋

3.4. エンドユーザーによる抜粋

3.5. 地域別

4. 力学

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 高齢者人口の増加

4.1.2. 抑制要因

4.1.2.1. インプラントおよび処置の高コスト

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

5.5. 償還分析

5.6. 特許分析

5.7. SWOT分析

5.8. DMI意見

6. 膝関節置換術別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率分析(%)、膝関節置換術別

6.1.2. 市場魅力度指数、膝関節置換術別

6.2. 人工膝関節システム*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率分析(%)

6.3. 部分膝関節システム

6.4. 再置換膝関節システム

7. 人工股関節置換術別

7.1. はじめに

7.1.1. 人工股関節置換術別:市場規模分析および前年比成長率(%)

7.1.2. 人工股関節置換術別:市場魅力度指数

7.2. 人工股関節全置換術システム *

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率分析(%)

7.3. 部分股関節システム

7.4. 修正股関節システム

8. 固定方法別

8.1. はじめに

8.1.1. 固定方法別市場規模分析および前年比成長率分析(%)

8.1.2. 固定方法別 市場魅力度指数

8.2. セメント固定*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率(%)

8.3. セメントレス固定

8.4. ハイブリッド固定

9. エンドユーザー別

9.1. はじめに

9.1.1. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

9.1.2. 市場魅力度指数、エンドユーザー別

9.2. 病院およびクリニック*

9.2.1. 概要

9.2.2. 市場規模分析および前年比成長率分析(%)

9.3. 外来外科センター

9.4. 整形外科クリニック

9.5. その他

10. 地域別

10.1. はじめに

10.1.1. 市場規模分析および前年比成長率分析(%)、地域別

10.1.2. 市場魅力度指数、地域別

10.2. 北米

10.2.1. はじめに

10.2.2. 主要地域別ダイナミクス

10.2.3. 製品・サービス別市場規模分析および前年比成長率分析(%)

10.2.4. 膝関節置換術別市場規模分析および前年比成長率分析(%)

10.2.5. 股関節置換術別市場規模分析および前年比成長率分析(%)

10.2.6. 固定方法別市場規模分析および前年比成長率分析(%)

10.2.7. エンドユーザー別市場規模分析および前年比成長率分析(%)

10.2.8. 国別市場規模分析および前年比成長率分析(%)

10.2.8.1. 米国

10.2.8.2. カナダ

10.2.8.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 主要地域別の動向

10.3.3. 製品・サービス別市場規模分析および前年比成長率分析(%)

10.3.4. 膝関節置換術別市場規模分析および前年比成長率(%)

10.3.5. 股関節置換術別市場規模分析および前年比成長率(%)

10.3.6. 固定方法別市場規模分析および前年比成長率(%)

10.3.7. エンドユーザー別市場規模推移および前年比成長率(%)

10.3.8. 国別市場規模推移および前年比成長率(%)

10.3.8.1. ドイツ

10.3.8.2. 英国

10.3.8.3. フランス

10.3.8.4. イタリア

10.3.8.5. スペイン

10.3.8.6. ヨーロッパのその他

10.4. 南アメリカ

10.4.1. はじめに

10.4.2. 主要地域別の動向

10.4.3. 製品・サービス別市場規模分析および前年比成長率分析(%)

10.4.4. 膝関節置換術別市場規模分析および前年比成長率(%)

10.4.5. 股関節置換術別市場規模分析および前年比成長率(%)

10.4.6. 固定方法別市場規模分析および前年比成長率(%)

10.4.7. エンドユーザー別市場規模分析および前年比成長率分析(%)

10.4.8. 国別市場規模分析および前年比成長率分析(%)

10.4.8.1. ブラジル

10.4.8.2. アルゼンチン

10.4.8.3. 南米その他

10.5. アジア太平洋

10.5.1. はじめに

10.5.2. 主要地域別の動向

10.5.3. 製品・サービス別市場規模分析および前年比成長率分析(%)

10.5.4. 膝関節置換別市場規模分析および前年比成長率分析(%)

10.5.5. 股関節置換別市場規模分析および前年比成長率分析(%)

10.5.6. 固定方法別市場規模分析および前年比成長率分析(%)

10.5.7. エンドユーザー別市場規模分析および前年比成長率分析(%)

10.5.8. 国別市場規模分析および前年比成長率分析(%)

10.5.8.1. 中国

10.5.8.2. インド

10.5.8.3. 日本

10.5.8.4. 韓国

10.5.8.5. アジア太平洋地域その他

10.6. 中東およびアフリカ

10.6.1. はじめに

10.6.2. 主要地域別の動向

10.6.3. 製品・サービス別市場規模分析および前年比成長率分析(%)

10.6.4. 人工膝関節置換術別市場規模分析および前年比成長率分析(%)

10.6.5. 人工股関節置換術別市場規模分析および前年比成長率分析(%)

10.6.6. 固定方法別市場規模分析および前年比成長率分析(%)

10.6.7. エンドユーザー別市場規模分析および前年比成長率分析(%)

11. 競合状況

11.1. 競合シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. 合併・買収分析

12. 企業プロフィール

F. Hoffmann-La Roche Ltd

Abbott

Hologic, Inc.

Danaher Corporation

Bio-Rad Laboratories, Inc.

Revvity

Siemens Healthcare Private Limited

Thermo Fisher Scientific Inc.

Illumina, Inc.

Sysmex Corporation

リストは網羅的なものではありません

13. 付録

13.1. 当社およびサービスについて

13.2. お問い合わせ

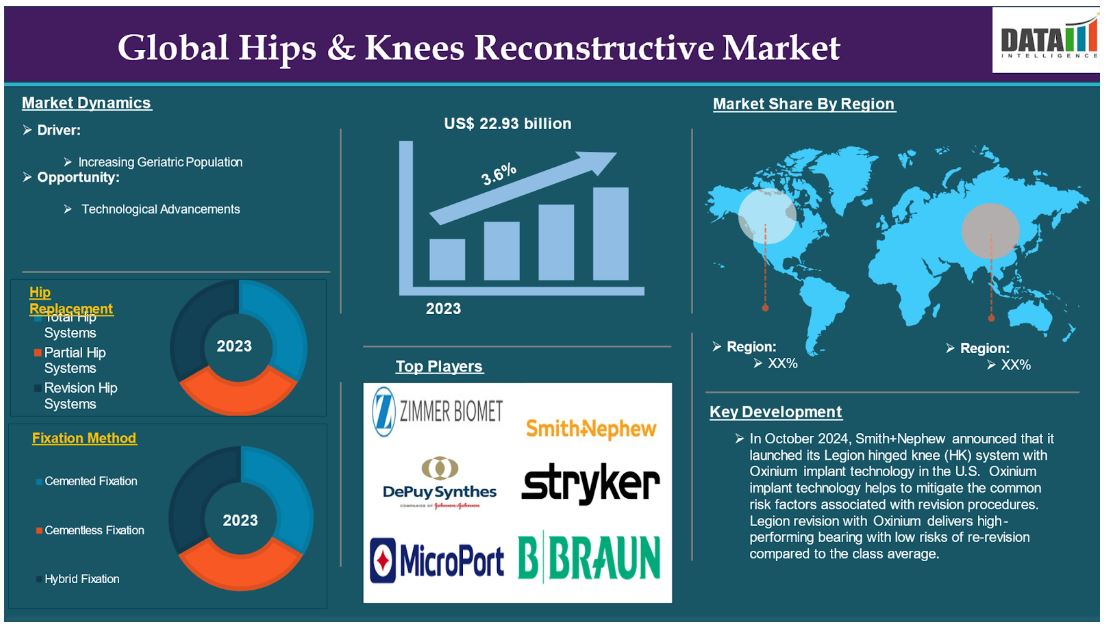

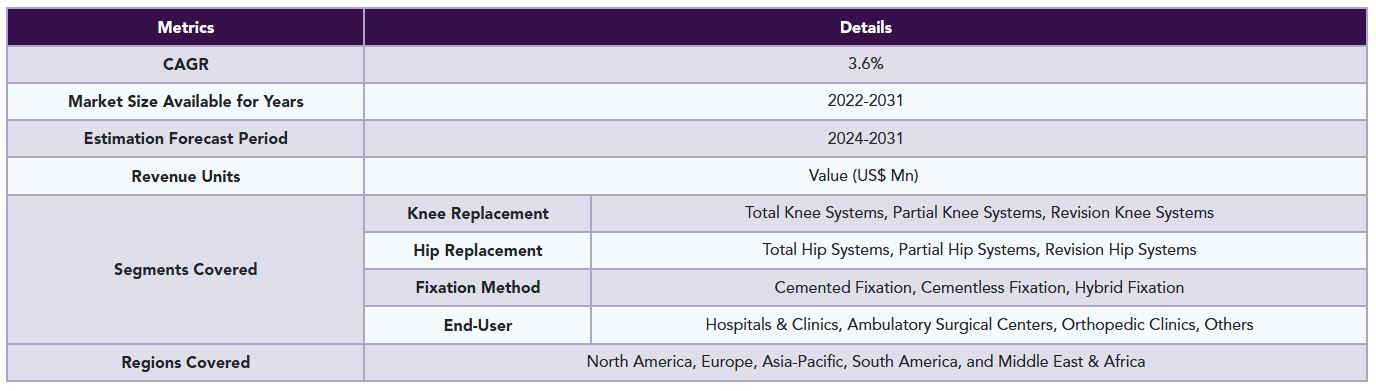

The global hips & knees reconstructive market reached US$ 17.30 billion in 2023 and is expected to reach US$ 22.93 billion by 2031, growing at a CAGR of 3.6% during the forecast period 2024-2031.

Hip and knee reconstructive procedures are surgical interventions designed to restore the function and integrity of hip and knee joints that have been affected by disorders such as osteoarthritis, rheumatoid arthritis, accident, or other degenerative diseases. These treatments usually entail replacing damaged joint components with artificial implants that mimic the natural mobility and function of healthy joints. The two main types of hip and knee reconstructive procedures are total joint replacement and partial joint replacement. Total joint replacement involves removing all damaged joint surfaces and replacing them with artificial components known as prostheses. These prostheses are precisely constructed to mimic the shape and movement of healthy joints.

The increasing prevalence of geriatric population is the driving factor that drives the market over the forecast period. For instance, according to the Pan American Health Organization, globally, there were an expected 20 million new cancer diagnoses and 10 million cancer deaths. Over the next two decades, the cancer burden will rise by almost 60%, putting a further burden on healthcare systems, individuals, and communities. For instance, according to the United Nations, The number of people aged 65 years or older worldwide is projected to more than double, rising from 761 million in 2021 to 1.6 billion in 2050. The number of people aged 80 years or older is growing even faster. Population ageing is an irreversible global trend.

Market Dynamics: Drivers & Restraints

Increasing geriatric population

The increasing geriatric population is expected to be a significant factor in the growth of the global hips & knees reconstructive market. As the population ages, the prevalence of age-related joint diseases such osteoarthritis and rheumatoid arthritis increases. These diseases frequently cause considerable pain, restricted mobility, and a lower quality of life, driving many senior people to seek surgical treatments such as hip and knee replacements. According to research, despite being at a higher risk of problems, older patients are becoming more inclined to undergo hip and knee replacements due to the significant benefits these treatments provide in terms of pain reduction and enhanced functionality. Furthermore, improvements in surgical techniques and implant technology have made these surgeries safer and more successful for older people.

For instance, according to WHO, in 2050, 80% of older people will be living in low- and middle-income countries. The pace of population aging is much faster than in the past. In 2020, the number of people aged 60 years and older outnumbered children younger than 5 years. Between 2015 and 2050, the proportion of the world's population over 60 years will nearly double from 12% to 22%. By 2030, 1 in 6 people in the world will be aged 60 years or over. At this time the share of the population aged 60 years and over will increase from 1 billion in 2020 to 1.4 billion. By 2050, the world’s population of people aged 60 years and older will double (2.1 billion). The number of persons aged 80 years or older is expected to triple between 2020 and 2050 to reach 426 million.

High Costs of Implants and Procedures

Factors such as high costs of implants and procedures are expected to hamper the global hips & knees reconstructive market. The high cost of implants and surgical procedures is a major hindrance to industry growth. These financial constraints can impede access to important therapies, especially for low-income patients or those without complete health insurance coverage. Total hip arthroplasty (THA) and total knee arthroplasty (TKA) operations can be expensive, frequently costing several thousand dollars when pre-operative examinations, surgery, and post-operative rehabilitation are all added together.

Segment Analysis

The global hips & knees reconstructive market is segmented based on knee replacement, hip replacement, fixation method, end-user, and region.

Knee replacement segment is expected to dominate the global hips & knees reconstructive market share

The knee replacement segment is expected to dominate the global hips and knees reconstructive market, owing to the rising prevalence of knee-related disorders and the increasing desire for effective surgical solutions. As osteoarthritis and other degenerative joint illnesses become more frequent, particularly among the elderly, the demand for knee replacements is increasing rapidly. This tendency is bolstered by the acceptance of knee replacement procedures as realistic solutions for regaining mobility and improving quality of life.

Advances in medical technology have also contributed significantly to the expansion of the knee replacement market. Innovations such as minimally invasive surgical techniques and improved implant designs have made operations safer and more effective, resulting in improved patient outcomes. These innovations not only extend the life of implants, but also appeal to a broader spectrum of patients, including younger people who are increasingly seeking knee replacements due to their active lives.

For instance, in June 2024, Meril, a Gujarat-based medical devices company, has launched an indigenously developed surgical robotic technology, MISSO, which will provide assistance to doctors during knee replacement surgeries in real-time. It is expected to make these surgeries up to 66 per cent budget friendly.

Geographical Analysis

North America is expected to hold a significant position in the global hips & knees reconstructive market share

North America is expected to hold a significant portion of the global hips & knees reconstructive market. North America is likely to maintain its dominant position in the worldwide hips and knees reconstructive market, owing to a mix of demographic trends, technological improvements, and a strong healthcare infrastructure. The region's aging population is one of the key drivers of the rising need for joint reconstruction surgeries. As people age, they become more prone to musculoskeletal problems like arthritis, which frequently demand surgical interventions such as hip and knee replacements. This demographic transition not only increases the need for these procedures, but also emphasizes the importance of appropriate healthcare solutions suited to elderly people.

For instance, according to urban.org, the number of Americans aged 65 and older will more than double over the next 40 years, reaching 80 million in 2040. The number of adults ages 85 and older, the group most often needing help with basic personal care, will nearly quadruple between 2000 and 2040. For an instance, according to America Health Ranking.org, 17.3% of the entire US population is geriatric population.

Asia Pacific is growing at the fastest pace in the global hips & knees reconstructive market

Asia Pacific is experiencing the fastest growth in global hips & knees reconstructive owing to the increasing incidence of chronic diseases and technological advancements in the region. The Asia Pacific region is experiencing the fastest growth in the global hips and knees reconstructive market, owing to a combination of demographic shifts, increased healthcare investments, and growing awareness of joint health. The aging population in many of the region's countries is one of the most significant contributors to its rapid growth. As life expectancy rises and birth rates fall, a bigger proportion of the population enters the elderly age bracket, which coincides with a higher prevalence of joint-related diseases like osteoarthritis.

The increasing geriatric population is one of the driving factors in this region making it the fastest growing region. For instance, according to the UNFPA India, he current elderly population of 153 million (aged 60 and above) is expected to reach a staggering 347 million by 2050.

Competitive Landscape

The major global players in the global hips & knees reconstructive market include F. Hoffmann-La Roche Ltd, Abbott, Hologic, Inc., Danaher Corporation, Bio-Rad Laboratories, Inc., Revvity, Siemens Healthcare Private Limited, Thermo Fisher Scientific Inc., Illumina, Inc., and Sysmex Corporation among others.

Emerging Players

Genomtec, QuantiLight, and GeneSys Bio among others

Key Developments

• In April 2024, Kharadi’s Manipal Hospital launched robotic knee replacement surgery, promising better accuracy and quicker recovery. Manipal Hospital, Kharadi has unveiled advanced robotic knee replacement surgery, promising improved precision, faster recovery times, and reduced pain compared to traditional procedures.

• In October 2024, Smith+Nephew announced that it launched its Legion hinged knee (HK) system with Oxinium implant technology in the U.S. Oxinium implant technology helps to mitigate the common risk factors associated with revision procedures. Legion revision with Oxinium delivers high-performing bearing with low risks of re-revision compared to the class average.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global hips & knees reconstructive market report would provide approximately 53 tables, 47 figures, and 176 pages.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Knee Replacement

3.2. Snippet by Hip Replacement

3.3. Snippet by Fixation Method

3.4. Snippet by End-User

3.5. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Increasing Geriatric Population

4.1.2. Restraints

4.1.2.1. High Costs of Implants and Procedures

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter's Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

5.5. Reimbursement Analysis

5.6. Patent Analysis

5.7. SWOT Analysis

5.8. DMI Opinion

6. By Knee Replacement

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Knee Replacement

6.1.2. Market Attractiveness Index, By Knee Replacement

6.2. Total Knee Systems*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Partial Knee System

6.4. Revision Knee Systems

7. By Hip Replacement

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Hip Replacement

7.1.2. Market Attractiveness Index, By Hip Replacement

7.2. Total Hip Systems *

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Partial Hip Systems

7.4. Revision Hip Systems

8. By Fixation Method

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Method

8.1.2. Market Attractiveness Index, By Fixation Method

8.2. Cemented Fixation*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Cementless Fixation

8.4. Hybrid Fixation

9. By End-User

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.1.2. Market Attractiveness Index, By End-User

9.2. Hospitals & Clinics*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Ambulatory Surgical Centers

9.4. Orthopedic Clinics

9.5. Others

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product and Service

10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Knee Replacement

10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Hip Replacement

10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Method

10.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.2.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.8.1. The U.S.

10.2.8.2. Canada

10.2.8.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product and Service

10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Knee Replacement

10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Hip Replacement

10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Method

10.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.3.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.8.1. Germany

10.3.8.2. UK

10.3.8.3. France

10.3.8.4. Italy

10.3.8.5. Spain

10.3.8.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product and Service

10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Knee Replacement

10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Hip Replacement

10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Method

10.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.4.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.8.1. Brazil

10.4.8.2. Argentina

10.4.8.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product and Service

10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Knee Replacement

10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Hip Replacement

10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Method

10.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.5.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.8.1. China

10.5.8.2. India

10.5.8.3. Japan

10.5.8.4. South Korea

10.5.8.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product and Service

10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Knee Replacement

10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Hip Replacement

10.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Fixation Method

10.6.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Zimmer Biomet*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. DePuy Synthes

12.3. Smith & Nephew plc.

12.4. Stryker

12.5. MicroPort Scientific Corporation

12.6. B. Braun Melsungen AG

12.7. Exactech Inc.

12.8. Limacorporate S.p.a.

12.9. CeramTec

12.10. ConforMIS

LIST NOT EXHAUSTIVE

13. Appendix

13.1. About Us and Services

13.2. Contact Us

*** 股関節&膝関節再建の世界市場に関するよくある質問(FAQ) ***

・股関節&膝関節再建の世界市場規模は?

→DataM Intelligence社は2023年の股関節&膝関節再建の世界市場規模を173億米ドルと推定しています。

・股関節&膝関節再建の世界市場予測は?

→DataM Intelligence社は2031年の股関節&膝関節再建の世界市場規模を229億3000万米ドルと予測しています。

・股関節&膝関節再建市場の成長率は?

→DataM Intelligence社は股関節&膝関節再建の世界市場が2024年~2031年に年平均3.6%成長すると展望しています。

・世界の股関節&膝関節再建市場における主要プレイヤーは?

→「F. Hoffmann-La Roche Ltd、Abbott、Hologic, Inc.、Danaher Corporation、Bio-Rad Laboratories, Inc.、Revvity、Siemens Healthcare Private Limited、Thermo Fisher Scientific Inc.、Illumina, Inc.、Sysmex Corporationなど ...」を股関節&膝関節再建市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/