1. 調査方法および範囲

1.1. 調査方法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品種類別抜粋

3.2. 用途別抜粋

3.3. エンドユーザー別抜粋

3.4. 地域別抜粋

4. ダイナミクス

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 整形外科的疾患の増加

4.1.1.2. XX

4.2. 抑制要因

4.2.1.1. ロボットの高コスト

4.3. 機会

4.3.1. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

6. 製品種類別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率(%) 製品種類別

6.1.2. 市場魅力度指数、種類別

6.2. システム*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率分析(%)

6.3. 機器およびアクセサリー

7. 用途別

7.1. はじめに

7.1.1. 用途別市場規模分析および前年比成長率(%)、用途別

7.1.2. 用途別市場魅力度指数

7.2. 脊椎手術*

7.2.1. 概要

7.2.2. 市場規模分析および前年比成長率(%)、用途別

7.3. 膝関節手術

7.4. 股関節手術

7.5. 外傷および骨折手術

7.6. その他

8. エンドユーザー別

8.1. はじめに

8.1.1. エンドユーザー別市場規模分析および前年比成長率(%)

8.1.2. エンドユーザー別市場魅力度指数

8.2. 病院*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率分析(%)

8.3. 整形外科クリニック

8.4. 外来外科センター

9. 地域別

9.1. はじめに

9.1.1. 地域別市場規模分析および前年比成長率分析(%)

9.1.2. 市場魅力度指数、地域別

9.2. 北米

9.2.1. はじめに

9.2.2. 主な地域特有の動向

9.2.3. 市場規模分析および前年比成長率(%)、製品種類別

9.2.4. 市場規模分析および前年比成長率(%)、用途別

9.2.5. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

9.2.6. 市場規模分析および前年比成長率分析(%)、国別

9.2.6.1. 米国

9.2.6.2. カナダ

9.2.6.3. メキシコ

9.3. ヨーロッパ

9.3.1. はじめに

9.3.2. 主要地域別の動向

9.3.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.3.4. 市場規模分析および前年比成長率分析(%)、用途別

9.3.5. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

9.3.6. 市場規模分析および前年比成長率分析(%)、国別

9.3.6.1. ドイツ

9.3.6.2. 英国

9.3.6.3. フランス

9.3.6.4. スペイン

9.3.6.5. イタリア

9.3.6.6. ヨーロッパのその他地域

9.4. 南アメリカ

9.4.1. はじめに

9.4.2. 主要地域特有の動向

9.4.3. 製品種類別市場規模分析および前年比成長率(%)

9.4.4. 用途別市場規模分析および前年比成長率(%)

9.4.5. エンドユーザー別市場規模分析および前年比成長率(%)

9.4.6. 国別市場規模分析および前年比成長率(%)

9.4.6.1. ブラジル

9.4.6.2. アルゼンチン

9.4.6.3. 南米その他

9.5. アジア太平洋

9.5.1. はじめに

9.5.2. 主要地域別の動向

9.5.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.5.4. 市場規模分析および前年比成長率分析(%)、用途別

9.5.5. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

9.5.6. 国別の市場規模分析および前年比成長率分析(%)

9.5.6.1. 中国

9.5.6.2. インド

9.5.6.3. 日本

9.5.6.4. 韓国

9.5.6.5. アジア太平洋地域その他

9.6. 中東およびアフリカ

9.6.1. はじめに

9.6.2. 主要地域別の動向

9.6.3. 製品種類別市場規模分析および前年比成長率(%)

9.6.4. 用途別市場規模分析および前年比成長率(%)

9.6.5. エンドユーザー別市場規模分析および前年比成長率(%)

10. 競合状況

10.1. 競合シナリオ

10.2. 市場ポジショニング/シェア分析

10.3. 合併・買収分析

11. 企業プロフィール

Ekso Bionics

Intuitive Surgical

Medtronic

Stryker Corporation

Smith & Nephew

Wright Medical Group N. V

Zimmer Biomet

General Electric

Think Surgical Inc

Omni

リストは網羅的ではありません

12. 付録

12.1 弊社およびサービスについて

12.2 お問い合わせ

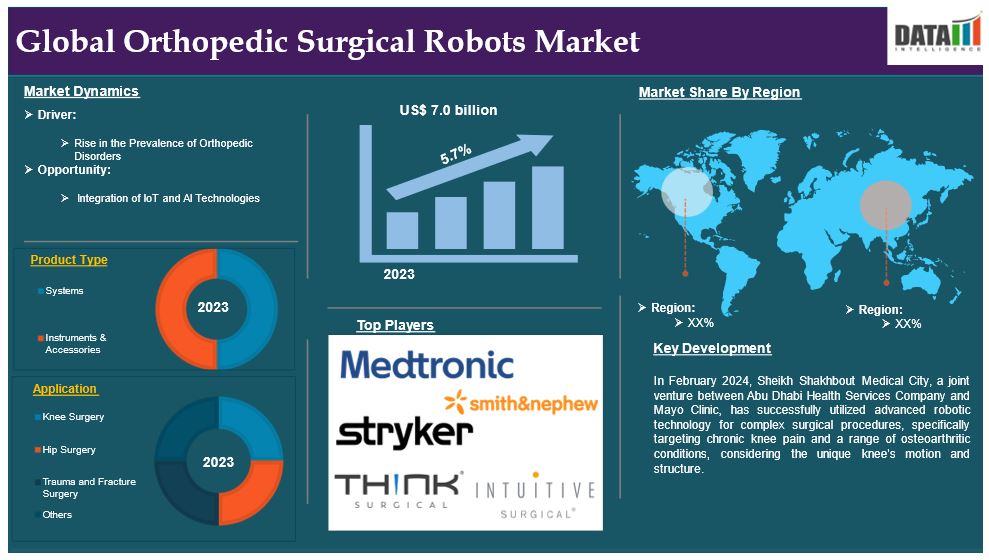

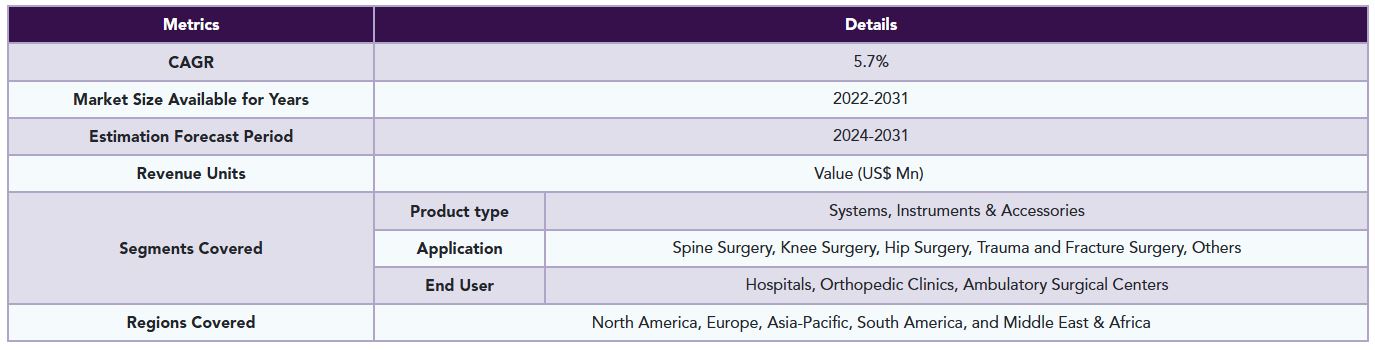

The global orthopedic surgical robots market reached US$ 7.0 billion in 2023 and is expected to reach US$ 10.7 billion by 2031, growing at a CAGR of 5.7% during the forecast period 2024-2031.

Orthopedic surgical robots are indeed revolutionary advances in the field of orthopedic surgery for the benefit of patients. Orthopedic surgical robots mark a considerable improvement in orthopedic surgery by providing surgery with high precision, effectiveness and invasiveness and has incredible advantages to improve patient outcomes. These robots help surgeons with unparalleled accuracy commit to intricate procedures without bringing the margin down due to human error.

They also provide real-time guidance for bone cutting and precise implant placement and alignment, thanks to advanced imaging technologies, robotic arms, and high-end software. Examples of commonly used procedures include total joint replacement, spine surgery, and fracture repairs. All orthopaedic surgical robots through minimal soft tissue damage and optimized workflow can now move a patient for faster recuperation, fewer complications, and greater surgical success.

Market Dynamics: Drivers & Restraints

Rise in the Prevalence of Orthopedic Disorders

The upsurge in the incidence of orthopedic conditions, such as osteoarthritis, rheumatoid arthritis, and osteoporosis, actually drives the global orthopedic surgical robots market. Little do these conditions depend on the age structure or sedentary lifestyle of the population; they directly create demand for joint replacements and other orthopedic interventions.

The practice of using orthopedic robots is focusing on giving precision and outcomes in knee surgeries, where most of the demands are required. Robotic alternatives have been favorable to both the patient and provider because they offer better or improved alignment, lower times of recovery, and fewer complications. There is growing dependence on robotic assistance in alleviating the rising burden of orthopedic disorders, thus attaining a wider footprint in the global market.

For instance, according to Australian Institute of Health and Welfare 2024, In 2023, the musculoskeletal conditions disease group accounted for 12.8% of total disease burden, 23.1% of non-fatal burden, and 0.8% of fatal burden. It was the second leading disease group contributing to non-fatal burden after mental health conditions and substance use disorders. Back problems were the leading cause of non-fatal burden, accounting for 7.9% of YLD. Within the musculoskeletal conditions disease group, back problems accounted for 34% of burden, followed by other musculoskeletal conditions at 30%, osteoarthritis at 20%, and rheumatoid arthritis at 16%.

High Cost of Robots

The global orthopedic surgical robots market is shaped by the high cost of these advanced systems, which can cost between $5,500 and over $10,000. These systems, which offer precision, reduced recovery times, and improved surgical outcomes, are expensive to implement, especially in smaller hospitals and developing regions. However, this financial barrier presents opportunities for innovation, such as developing cost-effective robotic systems or flexible financing models, which could broaden access and drive market growth.

Segment Analysis

The global orthopedic surgical robots market is segmented based on product type, application, end user and region.

Product type:

Systems segment is expected to dominate the orthopedic surgical robots market share

The systems segment holds a major portion of the orthopedic surgical robots market share and is expected to continue to hold a significant portion of the orthopedic surgical robots market share during the forecast period.

Orthopedic surgical systems are revolutionizing the global market by providing precise alignment, accurate bone resection, and improved implant placement in procedures like joint replacements and spine surgeries. These systems, equipped with advanced imaging, navigation, and robotic-assisted technologies, minimize human error, enhance surgical consistency, and contribute to better patient outcomes, reduced complications, and faster recovery times. As technological advancements continue, orthopedic surgical systems are expected to remain at the forefront of innovation, driving market growth by offering enhanced capabilities tailored to complex orthopedic procedures.

For instance, in October 2024, Aradhana Orthopedic Hospital in Shivamogga has introduced the region's first fully automatic robotic system for knee replacement surgeries, led by Dr. Girish Kumar K., MBBS, MS. This technology offers precision, efficiency, and quicker recovery times for patients undergoing knee replacement surgeries.

Application:

Spine Surgery segment is the fastest-growing segment in orthopedic surgical robots market share

The spine surgery segment is the fastest-growing segment in the orthopedic surgical robots market share and is expected to hold the market share over the forecast period.

Spine surgery is driving the global orthopedic surgical robots market growth, as robotic systems improve precision and safety in complex procedures like spinal fusions and decompressions. Advanced imaging and navigation technologies create accurate surgical plans, reducing complications and improving patient outcomes. The demand for robotic assistance in spine surgeries is driven by the increasing prevalence of spinal disorders, an aging population, and awareness of minimally invasive techniques. Robotic systems are reshaping the spine surgery landscape, making them a key segment in the orthopedic surgical robots market.

For instance, in August 2024, Johnson & Johnson MedTech has announced the launch of the VELYS Active Robotic-Assisted System (VELYS SPINE), a dual-use robotics and standalone navigation platform developed in collaboration with eCential Robotics. The system, which has received FDA clearance, is intended for spinal fusion procedures in the cervical, thoracolumbar, and sacroiliac spine. The dual-use system offers surgeons flexibility in their approach and plans, with active robotics allowing for surgical guidance tailored to their preferences. The unique features of active robotics technology are expected to set a new standard in spine surgical care.

Geographical Analysis

North America is expected to hold a significant position in the orthopedic surgical robots market share

North America holds a substantial position in the orthopaedic surgical robots’ market and is expected to hold most of the market share.

North America is a major player in the global orthopaedic surgical robots’ market due to technological advancements, robust healthcare infrastructure, and substantial financial investments. The region's network of hospitals and surgical centers prioritizes cutting-edge technologies, leading to widespread acceptance of robotic-assisted surgeries for joint replacements and spine surgeries. The high prevalence of musculoskeletal disorders, such as osteoarthritis and degenerative spine conditions, further fuels the demand for robotic-assisted surgeries.

Moreover, North America's leading manufacturers and innovators in robotic surgery systems drive the market forward, while favourable reimbursement policies and ongoing training of surgeons contribute to its dominance. The trend towards minimally invasive surgeries ensures the continued growth of orthopaedic surgical robots in the region.

For instance, in November 2024, THINK Surgical has received FDA clearance for its TMINI Miniature Robotic System, which is used with LinkSymphoKnee from Waldemar Link GmbH & Co. KG, Germany, under a collaboration agreement. The LinkSymphoKnee is part of THINK Surgical's ID-HUB, a proprietary data bank for the open platform version of its TMINI System in the US.

Europe is growing at the fastest pace in the orthopedic surgical robots market

Europe holds the fastest pace in the orthopaedic surgical robots market and is expected to hold most of the market share.

Europe is a key player in the global orthopaedic surgical robots’ market, driven by advanced healthcare systems, innovative technologies, and a focus on surgical precision. The region's supportive regulatory framework and reimbursement structures encourage the integration of robotics in surgical procedures. The aging population, more susceptible to orthopaedic conditions like osteoporosis and joint degeneration, drives the demand for surgical interventions. European healthcare providers are investing in robotic systems to enhance accuracy, reduce complications, and meet minimally invasive procedures. Countries like Germany, the UK, and France are leading the charge, with high adoption rates of robotic-assisted surgeries.

For instance, in September 2024, ZEISS Medical Technology has introduced the KINEVO 900 S, a new Robotic Visualization System, which enhances the clarity of complex surgical procedures in neurosurgery and other surgical disciplines, incorporating advanced digital visualization, collaborative assistant functions, and connected intelligence.

Moreover, in October 2024, Hospital Clinic Barcelona has performed 530 robotic knee replacement surgeries in three and a half years, using the ROSA robot developed by Zimmer and the Smith Nephew CORI Surgical System in 2022. This technological advancement enhances precision, safety, and patient recovery, making it the most performed hospital in Spain. The hospital's use of robotic surgery has minimized risks.

Competitive Landscape

The major global players in the orthopedic surgical robots market include Ekso Bionics, Intuitive Surgical, Medtronic, Stryker Corporation, Smith & Nephew, Wright Medical Group N. V, Zimmer Biomet, General Electric, Think Surgical Inc, Omni among others.

Emerging Players

The emerging players in the orthopedic surgical robots market include Adamis Robotics, OMNIlife Science, Inc, Medicaroid Corporation, Monogram Orthopedics and among others

Key Developments

• In February 2024, Sheikh Shakhbout Medical City, a joint venture between Abu Dhabi Health Services Company and Mayo Clinic, has successfully utilized advanced robotic technology for complex surgical procedures, specifically targeting chronic knee pain and a range of osteoarthritic conditions, considering the unique knee's motion and structure.

• In August 2023, Stryker has launched a direct patient marketing campaign to improve patient engagement and education about their innovative medical solutions, particularly joint replacement procedures. The campaign aims to empower individuals to make informed decisions about their healthcare, ultimately improving their overall experience and outcomes.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global orthopedic surgical robots market report delivers a detailed analysis with 60+ key tables, more than 50 visually impactful figures, and 176 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Component & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies

• Academic & Research: Academic Institutions.

Table of Contents

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product Type

3.2. Snippet by Application

3.3. Snippet by End User

3.4. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Rise in the Prevalence of Orthopedic Disorders

4.1.1.2. XX

4.2. Restraints

4.2.1.1. High Cost of Robots

4.3. Opportunity

4.3.1. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

6. By Product type

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product type

6.1.2. Market Attractiveness Index, By Product type

6.2. Systems*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Instruments & Accessories

7. By Application

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

7.1.2. Market Attractiveness Index, By Application

7.2. Spine Surgery*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Knee Surgery

7.4. Hip Surgery

7.5. Trauma and Fracture Surgery

7.6. Others

8. By End User

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

8.1.2. Market Attractiveness Index, By End User

8.2. Hospitals*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Orthopedic Clinics

8.4. Ambulatory Surgical Centers

9. By Region

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

9.1.2. Market Attractiveness Index, By Region

9.2. North America

9.2.1. Introduction

9.2.2. Key Region-Specific Dynamics

9.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

9.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.2.6.1. U.S.

9.2.6.2. Canada

9.2.6.3. Mexico

9.3. Europe

9.3.1. Introduction

9.3.2. Key Region-Specific Dynamics

9.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

9.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.3.6.1. Germany

9.3.6.2. U.K.

9.3.6.3. France

9.3.6.4. Spain

9.3.6.5. Italy

9.3.6.6. Rest of Europe

9.4. South America

9.4.1. Introduction

9.4.2. Key Region-Specific Dynamics

9.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

9.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.4.6.1. Brazil

9.4.6.2. Argentina

9.4.6.3. Rest of South America

9.5. Asia-Pacific

9.5.1. Introduction

9.5.2. Key Region-Specific Dynamics

9.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

9.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.5.6.1. China

9.5.6.2. India

9.5.6.3. Japan

9.5.6.4. South Korea

9.5.6.5. Rest of Asia-Pacific

9.6. Middle East and Africa

9.6.1. Introduction

9.6.2. Key Region-Specific Dynamics

9.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By End User

10. Competitive Landscape

10.1. Competitive Scenario

10.2. Market Positioning/Share Analysis

10.3. Mergers and Acquisitions Analysis

11. Company Profiles

11.1. Ekso Bionics*

11.1.1. Company Overview

11.1.2. Product Portfolio and Description

11.1.3. Financial Overview

11.1.4. Key Developments

11.2. Intuitive Surgical

11.3. Medtronic

11.4. Stryker Corporation

11.5. Smith & Nephew

11.6. Wright Medical Group N. V

11.7. Zimmer Biomet

11.8. General Electric

11.9. Think Surgical Inc

11.10. Omni

LIST NOT EXHAUSTIVE

12. Appendix

12.1 About Us and Services

12.2 Contact Us

*** 整形外科手術用ロボットの世界市場に関するよくある質問(FAQ) ***

・整形外科手術用ロボットの世界市場規模は?

→DataM Intelligence社は2023年の整形外科手術用ロボットの世界市場規模を70億米ドルと推定しています。

・整形外科手術用ロボットの世界市場予測は?

→DataM Intelligence社は2031年の整形外科手術用ロボットの世界市場規模を107億米ドルと予測しています。

・整形外科手術用ロボット市場の成長率は?

→DataM Intelligence社は整形外科手術用ロボットの世界市場が2024年~2031年に年平均5.7%成長すると展望しています。

・世界の整形外科手術用ロボット市場における主要プレイヤーは?

→「Ekso Bionics、Intuitive Surgical、Medtronic、Stryker Corporation、Smith & Nephew、Wright Medical Group N. V、Zimmer Biomet、General Electric、Think Surgical Inc、Omniなど ...」を整形外科手術用ロボット市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/