1. 市場の紹介と範囲

1.1. 本レポートの目的

1.2. 本レポートの対象範囲と定義

1.3. 本レポートの範囲

2. 経営陣の見解と主な結論

2.1. 市場のハイライトと戦略的結論

2.2. 主な傾向と将来予測

2.3. 製品の種類別抜粋

2.4. 接続形態別

2.5. 用途別

2.6. エンドユーザー別

2.7. 地域別

3. 動向

3.1. 影響要因

3.1.1. 推進要因

3.1.1.1. 在宅医療への需要の高まり

3.1.1.2. 技術的進歩の進展

3.1.2. 阻害要因

3.1.2.1. 運用およびユーザーの課題

3.1.3. 機会

3.1.4. 影響分析

4. 戦略的洞察および業界展望

4.1. 市場リーダーおよび先駆者

4.1.1. 新興の先駆者および有力企業

4.1.2. 最も売れているブランドを持つ確立されたリーダー企業

4.1.3. 確立された製品を持つ市場リーダー企業

4.2. 新興企業と主要イノベーター

4.3. CXOの見解

4.4. 最新の進展と画期的な出来事

4.5. ケーススタディ/進行中の研究

4.6. 規制と償還の概観

4.6.1. 北米

4.6.2. ヨーロッパ

4.6.3. アジア太平洋

4.6.4. ラテンアメリカ

4.6.5. 中東およびアフリカ

4.7. ポーターのファイブフォース分析

4.8. サプライチェーン分析

4.9. 特許分析

4.10. SWOT分析

4.11. 未充足ニーズとギャップ

4.12. 市場参入と拡大のための推奨戦略

4.13. シナリオ分析:最善のケース、基本ケース、最悪のケースの予測

4.14. 価格分析と価格力学

5. 製品種類別スマートポンプ市場

5.1. はじめに

5.1.1. 市場規模分析および前年比成長率(%)の種類別

5.1.2. 市場魅力度指数の種類別

5.2. 輸液スマートポンプ*

5.2.1. はじめに

5.2.2. 市場規模分析および前年比成長率(%)

5.3. スマート給餌ポンプ

5.4. 特殊ポンプ

6. スマートポンプ市場:接続性別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率(%)別、接続性別

6.1.2. 市場魅力度指数、接続性別

6.2. スタンドアロンポンプ*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率(%)別

6.3. 接続型ポンプ

6.3.1. 有線接続

6.3.2. 無線接続

7. 用途別スマートポンプ市場

7.1. はじめに

7.1.1. 用途別市場規模分析および前年比成長率(%)

7.1.2. 用途別市場魅力度指数

7.2. 薬物送達*

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率分析(%)

7.3. 化学療法

7.4. 疼痛管理

7.5. 糖尿病管理

7.6. 新生児および小児医療

7.7. その他

8. スマートポンプ市場、エンドユーザー別

8.1. はじめに

8.1.1. エンドユーザー別市場規模分析および前年比成長率(%)

8.1.2. エンドユーザー別市場魅力度指数

8.2. 病院*

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率(%)

8.3. 専門クリニック

8.4. 外来外科センター

8.5. 在宅医療

9. スマートポンプ市場、地域別市場分析と成長機会

9.1. はじめに

9.1.1. 市場規模分析と前年比成長率(%)、地域別

9.1.2. 市場魅力度指数、地域別

9.2. 北米

9.2.1. はじめに

9.2.2. 主要地域別ダイナミクス

9.2.3. 市場規模分析および前年比成長率(%)製品種類別

9.2.4. 市場規模分析および前年比成長率(%)接続性別

9.2.5. 市場規模分析および前年比成長率(%)用途別

9.2.6. エンドユーザー別市場規模分析および前年比成長率分析(%)

9.2.7. 国別市場規模分析および前年比成長率分析(%)

9.2.7.1. 米国

9.2.7.2. カナダ

9.2.7.3. メキシコ

9.3. ヨーロッパ

9.3.1. はじめに

9.3.2. 主要地域別の動向

9.3.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.3.4. 市場規模分析および前年比成長率分析(%)、接続別

9.3.5. 市場規模分析および前年比成長率分析(%)、用途別

9.3.6. エンドユーザー別市場規模分析および前年比成長率分析(%)

9.3.7. 国別市場規模分析および前年比成長率分析(%)

9.3.7.1. ドイツ

9.3.7.2. 英国

9.3.7.3. フランス

9.3.7.4. スペイン

9.3.7.5. イタリア

9.3.7.6. ヨーロッパのその他地域

9.4. 南アメリカ

9.4.1. はじめに

9.4.2. 主要地域別の動向

9.4.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.4.4. 接続形態別市場規模分析および前年比成長率(%)

9.4.5. 用途別市場規模分析および前年比成長率(%)

9.4.6. エンドユーザー別市場規模分析および前年比成長率(%)

9.4.7. 国別市場規模分析および前年比成長率(%)

9.4.7.1. ブラジル

9.4.7.2. アルゼンチン

9.4.7.3. 南米その他

9.5. アジア太平洋地域

9.5.1. はじめに

9.5.2. 主要地域特有の動向

9.5.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.5.4. 接続形態別市場規模分析および前年比成長率(%)

9.5.5. 用途別市場規模分析および前年比成長率(%)

9.5.6. エンドユーザー別市場規模分析および前年比成長率(%)

9.5.7. 国別市場規模分析および前年比成長率(%)

9.5.7.1. 中国

9.5.7.2. インド

9.5.7.3. 日本

9.5.7.4. 韓国

9.5.7.5. アジア太平洋地域その他

9.6. 中東およびアフリカ

9.6.1. はじめに

9.6.2. 主要地域特有の動向

9.6.3. 市場規模分析および前年比成長率分析(%)、製品種類別

9.6.4. 市場規模分析および前年比成長率分析(%)、接続別

9.6.5. 市場規模分析および前年比成長率分析(%)、用途別

9.6.6. 市場規模分析および前年比成長率分析(%)、エンドユーザー別

10. 競合状況と市場ポジショニング

10.1. 競合の概要と主要市場プレーヤー

10.2. 市場シェア分析とポジショニングマトリクス

10.3. 戦略的提携、合併および買収

10.4. 製品ポートフォリオとイノベーションにおける主要な展開

10.5. 企業ベンチマーキング

11. 企業プロフィール

B. Braun Medical Inc.

Medtronic plc

Fresenius Kabi USA, LLC

Terumo Corporation

Becton, Dickinson and Company

ICU Medical, Inc.

Baxter International Inc.

Insulet Corporation

BPL Medical Technologies

SINO MDT

(リストは網羅的ではない)

12. 仮定と調査方法

12.1. データ収集方法

12.2. データの三角測量

12.3. 予測の処置

12.4. データの検証と妥当性確認

13. 付録

13.1. 弊社とサービスについて

13.2. お問い合わせ

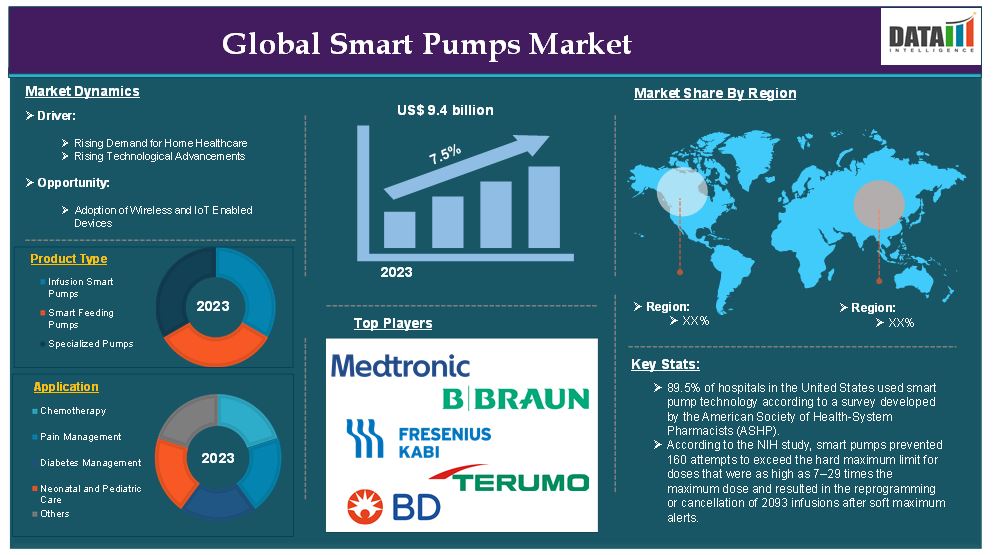

The global smart pumps market reached US$ 9.4 billion in 2023 and is expected to reach US$ 16.7 billion by 2031, growing at a CAGR of 7.5% during the forecast period 2024-2031.

Smart pumps are technologically advanced medical devices designed to accurately and safely deliver fluids, medications or nutrients to patients through intravenous (IV), enteral or other delivery routes. These pumps integrate intelligent software, sensors and connectivity features to enhance precision, reduce errors and optimize patient care. Smart pumps in healthcare represent a significant advancement in medical technology, enabling precise, safe and efficient delivery of critical therapies, with applications ranging from critical care units to home healthcare environments.

The smart pump market in healthcare is expanding rapidly. This growth is fueled by increased demand for patient safety features like dose error reduction software and smart integration capabilities. For instance, according to the National Institute of Health, 89.5% of hospitals in the United States used smart pump technology according to a survey developed by the American Society of Health-System Pharmacists (ASHP). The utilization of smart pump technology varied by hospital bed size with full implementation in hospitals with 600 beds and more.

Additionally, according to the study conducted by the National Institute of Health, using smart pump records, over 370,000 infusion starts for continuously infused medications used in neonates and infants hospitalized in a level IV NICU were evaluated. Smart pumps prevented 160 attempts to exceed the hard maximum limit for doses that were as high as 7–29 times the maximum dose and resulted in the reprogramming or cancellation of 2093 infusions after soft maximum alerts.

Market Dynamics: Drivers & Restraints

Rising demand for home healthcare

Rising demand for home healthcare is significantly driving the growth of the smart pumps market and is expected to drive the market over the forecast period by increasing the need for reliable, accurate and remotely manageable medical devices that can be used outside of hospital settings. As the global population ages, there is a higher prevalence of chronic conditions such as diabetes, heart disease and kidney failure. These conditions often require long-term treatments such as insulin delivery, parenteral nutrition and pain management through infusion pumps. Smart pumps, with their ability to provide accurate dosing and real-time monitoring, are ideal for home use.

According to the World Health Organization, about 830 million people worldwide have diabetes, the majority living in low-and middle-income countries. The number of people living with diabetes rose from 200 million in 1990 to 830 million in 2022. In 2021, diabetes and kidney disease due to diabetes caused over 2 million deaths. In addition, around 11% of cardiovascular deaths were caused by high blood glucose. This rising diabetes may increase the demand for insulin pumps, thus, there is an increasing demand for smart pumps to use at home.

For instance, according to the National Institute of Health, over 22 months, insulin pump use rates increased from 45 to 58%, a significant improvement. Use of diabetes technology, including insulin pumps, has been associated with improved glycemic control, particularly in youths with type 1 diabetes. This further increases the demand for smart pumps which helps to manage insulin levels at home.

The trend toward patient-centric care and hospital-at-home programs is fueling the adoption of smart pumps. Healthcare providers are increasingly allowing patients to manage their treatments at home, reducing hospital visits and costs. For instance, patients receiving chemotherapy, home parenteral nutrition or continuous insulin therapy can use smart pumps to safely administer their treatments while being monitored remotely by healthcare professionals.

For instance, almost $103 billion was spent on home health care in the United States and that number will reach nearly $173 billion by 2026, according to an analysis from the Centers for Medicare & Medicaid Services (CMS) Office of the Actuary. This growth is driven by the push for outpatient care, increasing healthcare costs and improvements in home-based medical devices.

Operational and user challenges

Operational and user challenges are expected to hamper the growth of the smart pumps market. Despite their advanced features and significant benefits, these challenges hinder widespread adoption, particularly in complex healthcare environments like hospitals, clinics, and home settings. Smart pumps come with sophisticated features like dose error reduction software, remote monitoring and integration with hospital systems. These features require a higher level of technical knowledge to operate effectively. For instance, pumps designed for drug delivery, such as those for chemotherapy or insulin, may have intricate settings that can overwhelm healthcare professionals without adequate training.

Additionally, in hospitals, some medical staff report a steep learning curve when it comes to handling smart pumps, especially when switching from traditional pumps. This increases the likelihood of human errors during the initial transition period, which can discourage facilities from fully adopting smart pump technologies.

In some instances, hospitals have faced integration challenges with their smart infusion pumps and medication administration systems. The lack of standardized protocols across devices and systems means that connecting these devices with existing infrastructure can be time-consuming and costly. For instance, according to the University Health System (UHS), smart pumps can run $1,200 to $1,300. One setup typically falls within a cost range of $3,000 to $4,000, including the software license cost. Of the 7,000 IV pumps in inventory, UHS had about 1,800 to 2,400 smart pumps.

Segment Analysis

The global smart pumps market is segmented based on product type, connectivity, application, end-user and region.

Product Type:

The infusion smart pumps segment is expected to dominate the smart pumps market share

The infusion smart pumps segment is expected to dominate the global smart pumps market. Infusion pumps are used extensively across various healthcare settings, including hospitals, clinics and home care environments. These devices are essential for drug delivery, parenteral nutrition, chemotherapy and insulin therapy, among other treatments.

Infusion smart pumps incorporate advanced dose error reduction systems, wireless connectivity, dose safety software and real-time monitoring, which enhances their safety and efficiency. These innovations help reduce medication errors, a significant concern in healthcare.

For instance, in April 2024, Baxter International Inc. cleared the U.S. Food and Drug Administration (FDA) 510(k) clearance of its Novum IQ large volume infusion pump (LVP) with Dose IQ Safety Software. Adding LVP modality to the Novum IQ Infusion Platform, which includes Baxter’s syringe infusion pump (SYR) with Dose IQ Safety Software, powered by the IQ Enterprise Connectivity Suite, enables clinicians to utilize a single, integrated system across a variety of patient care settings.

As more patients prefer managing their treatments at home, the need for portable infusion pumps has increased. Smart pumps allow for remote monitoring and data sharing, which are crucial for home healthcare settings, especially for chronic patients requiring ongoing infusion therapy.

Geographical Analysis

North America is expected to hold a significant position in the smart pumps market share

North America is expected to hold the largest market share in the global smart pumps market. North America, especially the United States is home to leading manufacturers of smart pumps, including Medtronic, Baxter International and other emerging players, which are continuously innovating to develop advanced, user-friendly smart pumps. These innovations, such as wireless connectivity, real-time monitoring and cloud-based data analytics, make these devices highly desirable in the healthcare industry.

For instance, in June 2023, B. Braun Medical Inc. launched its next generation of infusion management software, DoseTrac Enterprise Infusion Management Software. With this new software, organizations receive a mix of real-time views and retrospective reporting features to better understand their infusion pump fleet and associated data. The DoseTrac Enterprise Software platform can also connect up to 40,000 pumps at an unlimited number of facilities with just one application.

North America has a high prevalence of chronic diseases like diabetes, heart disease and cancer, which require continuous medication administration via infusion pumps. This has fueled the demand for smart pumps, especially for insulin infusion pumps and chemotherapy drug delivery systems. For instance, according to the American Diabetes Association, 38.4 million Americans, or 11.6% of the population, have diabetes, many of whom rely on infusion pumps for insulin delivery. The growing patient population is a significant driver for the smart infusion pump market.

Asia-Pacific is growing at the fastest pace in the smart pumps market

The Asia-Pacific region is experiencing the fastest growth in the smart pumps market. There has been a rapid increase in the adoption of smart healthcare devices in the Asia Pacific region. This is partly driven by the growing need for remote monitoring, dose error reduction and patient safety in hospitals and home care settings. Major market players in this region especially China, India and Japan focusing on smart infusion pumps with integrated technologies that allow for wireless communication, real-time data sharing and remote patient monitoring are seeing a surge in demand.

For instance, in February 2023 Mindray launched its BeneFusion i Series and u Series infusion systems featuring high precision, adaptive customization and extraordinary simplicity for guaranteed levels of medication safety in a variety of clinical settings. The new generation of smart pumps, for their advanced features to reduce medication errors, streamline workflow and improve cost-effectiveness, has seen greater potential in endoscopic, obstetrics, oncology, emergency departments and more.

Competitive Landscape

The major global players in the smart pumps market include B. Braun Medical Inc., Medtronic plc, Fresenius Kabi USA, LLC, Terumo Corporation, Becton, Dickinson and Company, ICU Medical, Inc., Baxter International Inc., Insulet Corporation, BPL Medical Technologies, SINO MDT and among others.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global smart pumps market report delivers a detailed analysis with 70 key tables, more than 65 visually impactful figures, and 179 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

Table of Contents

1. Market Introduction and Scope

1.1. Objectives of the Report

1.2. Report Coverage & Definitions

1.3. Report Scope

2. Executive Insights and Key Takeaways

2.1. Market Highlights and Strategic Takeaways

2.2. Key Trends and Future Projections

2.3. Snippet by Product Type

2.4. Snippet by Connectivity

2.5. Snippet by Application

2.6. Snippet by End-User

2.7. Snippet by Region

3. Dynamics

3.1. Impacting Factors

3.1.1. Drivers

3.1.1.1. Rising Demand for Home Healthcare

3.1.1.2. Rising Technological Advancements

3.1.2. Restraints

3.1.2.1. Operational and User Challenges

3.1.3. Opportunity

3.1.4. Impact Analysis

4. Strategic Insights and Industry Outlook

4.1. Market Leaders and Pioneers

4.1.1. Emerging pioneers and prominent players

4.1.2. Established leaders with largest-selling brands

4.1.3. Market leaders with established Product

4.2. Emerging Startups and Key Innovators

4.3. CXO Perspectives

4.4. Latest Developments and Breakthroughs

4.5. Case Studies/Ongoing Research

4.6. Regulatory and Reimbursement Landscape

4.6.1. North America

4.6.2. Europe

4.6.3. Asia Pacific

4.6.4. Latin America

4.6.5. Middle East & Africa

4.7. Porter’s Five Force Analysis

4.8. Supply Chain Analysis

4.9. Patent Analysis

4.10. SWOT Analysis

4.11. Unmet Needs and Gaps

4.12. Recommended Strategies for Market Entry and Expansion

4.13. Scenario Analysis: Best-Case, Base-Case, and Worst-Case Forecasts

4.14. Pricing Analysis and Price Dynamics

5. Smart Pumps Market, By Product Type

5.1. Introduction

5.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

5.1.2. Market Attractiveness Index, By Product Type

5.2. Infusion Smart Pumps*

5.2.1. Introduction

5.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

5.3. Smart Feeding Pumps

5.4. Specialized Pumps

6. Smart Pumps Market, By Connectivity

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

6.1.2. Market Attractiveness Index, By Connectivity

6.2. Standalone Pumps*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Connected Pumps

6.3.1. Wired Connectivity

6.3.2. Wireless Connectivity

7. Smart Pumps Market, By Application

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

7.1.2. Market Attractiveness Index, By Application

7.2. Drug Delivery*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Chemotherapy

7.4. Pain Management

7.5. Diabetes Management

7.6. Neonatal and Pediatric Care

7.7. Others

8. Smart Pumps Market, By End-User

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

8.1.2. Market Attractiveness Index, By End-User

8.2. Hospitals*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Specialty Clinics

8.4. Ambulatory Surgical Centers

8.5. Homecare Settings

9. Smart Pumps Market, By Regional Market Analysis and Growth Opportunities

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

9.1.2. Market Attractiveness Index, By Region

9.2. North America

9.2.1. Introduction

9.2.2. Key Region-Specific Dynamics

9.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

9.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.2.7.1. U.S.

9.2.7.2. Canada

9.2.7.3. Mexico

9.3. Europe

9.3.1. Introduction

9.3.2. Key Region-Specific Dynamics

9.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

9.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.3.7.1. Germany

9.3.7.2. U.K.

9.3.7.3. France

9.3.7.4. Spain

9.3.7.5. Italy

9.3.7.6. Rest of Europe

9.4. South America

9.4.1. Introduction

9.4.2. Key Region-Specific Dynamics

9.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

9.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.4.7.1. Brazil

9.4.7.2. Argentina

9.4.7.3. Rest of South America

9.5. Asia-Pacific

9.5.1. Introduction

9.5.2. Key Region-Specific Dynamics

9.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

9.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

9.5.7.1. China

9.5.7.2. India

9.5.7.3. Japan

9.5.7.4. South Korea

9.5.7.5. Rest of Asia-Pacific

9.6. Middle East and Africa

9.6.1. Introduction

9.6.2. Key Region-Specific Dynamics

9.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

9.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Connectivity

9.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

9.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10. Competitive Landscape and Market Positioning

10.1. Competitive Overview and Key Market Players

10.2. Market Share Analysis and Positioning Matrix

10.3. Strategic Partnerships, Mergers & Acquisitions

10.4. Key Developments in Product Portfolios and Innovations

10.5. Company Benchmarking

11. Company Profiles

11.1. B. Braun Medical Inc. *

11.1.1. Company Overview

11.1.2. Product Portfolio and Description

11.1.3. Financial Overview

11.1.4. Key Developments

11.1.5. SWOT Analysis

11.2. Medtronic plc

11.3. Fresenius Kabi USA, LLC

11.4. Terumo Corporation

11.5. Becton, Dickinson and Company

11.6. ICU Medical, Inc.

11.7. Baxter International Inc.

11.8. Insulet Corporation

11.9. BPL Medical Technologies

11.10. SINO MDT (LIST NOT EXHAUSTIVE)

12. Assumption and Research Methodology

12.1. Data Collection Methods

12.2. Data Triangulation

12.3. Forecasting Techniques

12.4. Data Verification and Validation

13. Appendix

13.1. About Us and Services

13.2. Contact Us

*** スマートポンプの世界市場に関するよくある質問(FAQ) ***

・スマートポンプの世界市場規模は?

→DataM Intelligence社は2023年のスマートポンプの世界市場規模を94億米ドルと推定しています。

・スマートポンプの世界市場予測は?

→DataM Intelligence社は2031年のスマートポンプの世界市場規模を167億米ドルと予測しています。

・スマートポンプ市場の成長率は?

→DataM Intelligence社はスマートポンプの世界市場が2024年~2031年に年平均7.5%成長すると展望しています。

・世界のスマートポンプ市場における主要プレイヤーは?

→「B. Braun Medical Inc.、Medtronic plc、Fresenius Kabi USA, LLC、Terumo Corporation、Becton, Dickinson and Company、ICU Medical, Inc.、Baxter International Inc.、Insulet Corporation、BPL Medical Technologies、SINO MDTなど ...」をスマートポンプ市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/