1. 調査方法および範囲

1.1. 調査方法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品タイプ別抜粋

3.2. インプラントの種類別抜粋

3.3. 用途別抜粋

3.4. エンドユーザー別抜粋

3.5. 地域別

4. 動向

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 歯科疾患の増加

4.1.1.2. XX

4.1.2. 抑制要因

4.1.2.1. 知覚過敏およびアレルギー反応

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 特許分析

5.5. 規制分析

5.6. SWOT分析

5.7. 未充足ニーズ

6. 製品種類別

6.1. はじめに

6.1.1. 製品種類別分析および前年比成長率(%)

6.1.2. 製品種類別市場魅力度指数

6.2. 商用純チタン(CPTi)*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率(%)

6.2.3. グレードI

6.2.4. グレードII

6.2.5. グレードIII

6.2.6. グレードIV

6.3. チタン合金

6.3.1. Ti-6Al-4V

6.3.2. Ti-6Al-4V超低間隙

6.3.3. Ti-5Al-2.5Fe

6.3.4. Ti-3Al-2.5V

7. インプラントの種類別

7.1. はじめに

7.1.1. 市場規模分析および前年比成長率分析(%)、インプラントの種類別

7.1.2. 市場魅力度指数、インプラントの種類別

7.2. 歯槽骨内インプラント*

7.2.1. イントロダクション

7.2.2. 市場規模分析および前年比成長率(%)

7.3. 骨膜下インプラント

7.4. 歯槽骨インプラント

8. 用途別

8.1. イントロダクション

8.1.1. 市場規模および前年比成長率分析(%)、用途別

8.1.2. 市場魅力度指数、用途別

8.2. 単一歯の置換*

8.2.1. 概要

8.2.2. 市場規模および前年比成長率分析(%)

8.3. 複数歯の置換

8.4. その他

9. エンドユーザー別

9.1. イントロダクション

9.1.1. エンドユーザー別市場規模分析および前年比成長率(%)

9.1.2. エンドユーザー別市場魅力度指数

9.2. 病院 *

9.2.1. イントロダクション

9.2.2. 市場規模分析および前年比成長率(%)

9.3. 歯科クリニック

9.4. その他

10. 地域別

10.1. はじめに

10.1.1. 地域別市場規模分析および前年比成長率(%)

10.1.2. 地域別市場魅力度指数

10.2. 北米

10.2.1. はじめに

10.2.2. 主要地域別の動向

10.2.3. 市場規模および前年比成長率(%)製品タイプ別

10.2.4. 市場規模および前年比成長率(%)インプラントの種類別

10.2.5. 市場規模および前年比成長率(%)用途別

10.2.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.2.7. 国別市場規模分析および前年比成長率(%)

10.2.7.1. 米国

10.2.7.2. カナダ

10.2.7.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 主要地域別の動向

10.3.3. 製品タイプ別市場規模分析および前年比成長率(%)

10.3.4. インプラントの種類別市場規模分析および前年比成長率(%)

10.3.5. 用途別市場規模分析および前年比成長率(%)

10.3.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.3.7. 国別市場規模分析および前年比成長率(%)

10.3.7.1. ドイツ

10.3.7.2. 英国

10.3.7.3. フランス

10.3.7.4. スペイン

10.3.7.5. イタリア

10.3.7.6. ヨーロッパのその他地域

10.4. 南アメリカ

10.4.1. はじめに

10.4.2. 主要地域特有の動向

10.4.3. 製品タイプ別市場規模分析および前年比成長率(%)

10.4.4. インプラントの種類別市場規模分析および前年比成長率(%)

10.4.5. 用途別市場規模分析および前年比成長率(%)

10.4.6. エンドユーザー別市場規模および前年比成長率分析(%)

10.4.7. 国別市場規模および前年比成長率分析(%)

10.4.7.1. ブラジル

10.4.7.2. アルゼンチン

10.4.7.3. 南米その他

10.5. アジア太平洋地域

10.5.1. はじめに

10.5.2. 主要地域特有の動向

10.5.3. 製品タイプ別市場規模分析および前年比成長率(%)

10.5.4. インプラントの種類別市場規模分析および前年比成長率(%)

10.5.5. 用途別市場規模分析および前年比成長率(%)

10.5.6. エンドユーザー別市場規模分析および前年比成長率(%)

10.5.7. 国別市場規模分析および前年比成長率(%)

10.5.7.1. 中国

10.5.7.2. インド

10.5.7.3. 日本

10.5.7.4. 韓国

10.5.7.5. アジア太平洋地域その他

10.6. 中東およびアフリカ

10.6.1. はじめに

10.6.2. 主要地域特有の動向

10.6.3. 製品タイプ別市場規模分析および前年比成長率(%)

10.6.4. インプラントの種類別市場規模分析および前年比成長率(%)

10.6.5. 用途別市場規模分析および前年比成長率(%)

10.6.6. エンドユーザー別市場規模分析および前年比成長率分析(%)

11. 競合状況

11.1. 競合シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. 合併・買収分析

12. 企業プロフィール

Institut Straumann AG

Nobel Biocare Services AG

Dentsply Sirona

Zimmer Biomet

OSSTEM IMPLANT CO., LTD.

KYOCERA Medical Technologies, Inc.

COWELLMEDI CO., LTD.

ZimVie Inc.

LeaderMedica SRL

BioHorizons

(リストは網羅的ではありません)

13. 付録

13.1. 当社およびサービスについて

13.2. お問い合わせ

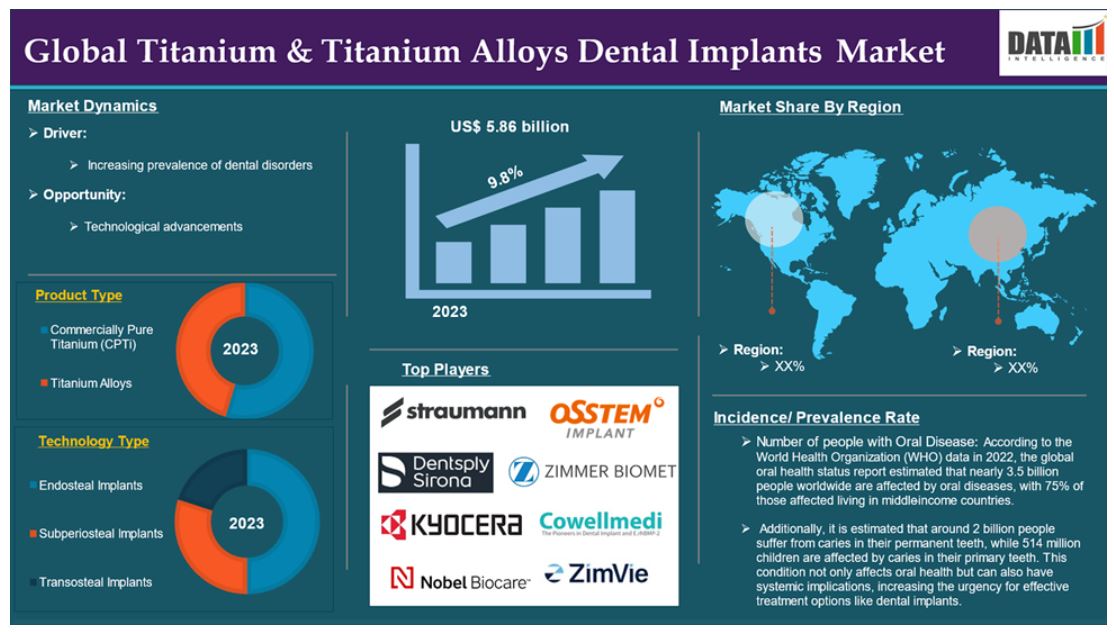

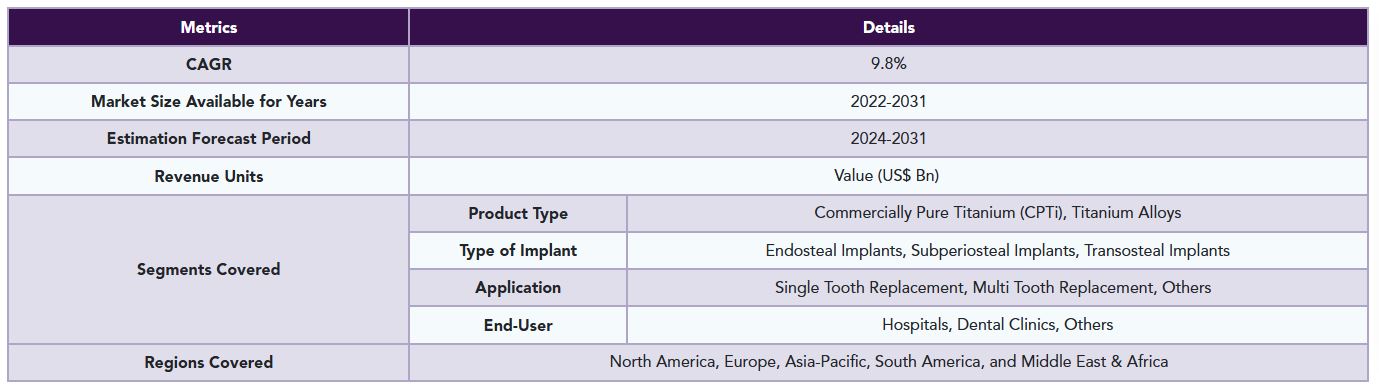

The global titanium & titanium alloys dental implants market reached US$ 5.86 billion in 2023 and is expected to reach US$ 12.33 billion by 2031, growing at a CAGR of 9.8% during the forecast period 2024-2031.

Titanium & titanium alloys dental implants are prosthetic devices designed from titanium or titanium alloys that are surgically inserted into the jawbone, acting as artificial roots for missing teeth. The implants bond with the bone through a process known as osseointegration, which provides a stable foundation for various dental restorations, including crowns, bridges, or dentures.

These materials are formed by combining titanium with other elements to enhance specific mechanical properties, such as strength and ductility. Common titanium alloys used in dental implants include Ti-6Al-4V, which contains 6% aluminum and 4% vanadium, and Ti-5Al-2.5Fe. These alloys are recognized for their superior mechanical performance compared to commercially pure titanium.

The global titanium & titanium alloys dental implants market is the widespread utilization of titanium and its alloys, which are favored for their advantageous properties that meet the requirements of contemporary dentistry. As technological advancements continue, particularly in manufacturing methods such as additive manufacturing, the versatility and application of titanium in dental implants are anticipated to grow further. Ongoing research aimed at improving implant designs and surface modifications is expected to enhance their performance and longevity, making them even more effective solutions for tooth replacement and restoration. These factors have driven the global titanium & titanium alloys dental implants market expansion.

Market Dynamics: Drivers & Restraints

Increasing Prevalence of Dental Disorders

The increasing prevalence of dental disorders is significantly driving the growth of the global titanium & titanium alloys dental implants market. It is expected to drive throughout the market forecast period.

The increasing incidence of dental diseases, particularly periodontal disease and dental caries, is a significant driver of demand in the global titanium & titanium alloys dental implants market. This demand is primarily fueled by the need for effective tooth replacement solutions as more individuals experience tooth loss due to these conditions.

According to the World Health Organization (WHO) data in 2022, the global oral health status report estimated that nearly 3.5 billion people worldwide are affected by oral diseases, with 75% of those affected living in middle-income countries. Additionally, it is estimated that around 2 billion people suffer from caries in their permanent teeth, while 514 million children are affected by caries in their primary teeth. This condition not only affects oral health but can also have systemic implications, increasing the urgency for effective treatment options like dental implants.

Titanium has become the standard material for dental implants for several compelling reasons. Its compatibility with human bone tissue is unmatched, making it an ideal choice for dental applications. Titanium and its alloys excel due to their biocompatibility, corrosion resistance, and dimensional stability. The dental community stands to gain significantly from ongoing research into developing new titanium alloys, which can enhance implant performance.

Furthermore, key players in the industry research studies that would drive this global titanium & titanium alloys dental implants market growth. According to the ScienceDirect research publication in January 2024, the advantages of additive manufacturing (AM) technology in creating dental implants are increasingly recognized. Researchers are actively studying the bio-functionality of titanium dental implants, employing various characterization techniques to identify ways to improve their effectiveness.

Titanium and its alloys remain an excellent choice for dental implants, with ongoing studies likely to confirm their suitability for dental implantology. All these factors demand the global titanium & titanium alloys dental implants market.

Moreover, the rising demand for technological advancements contributes to the expansion of the global titanium and titanium alloys dental implants market.

Hypersensitivity and Allergic Reactions

The hypersensitivity and allergic reactions will hinder the growth of the global titanium and titanium alloys dental implants market. While titanium is widely used in its biocompatibility and is generally deemed safe for dental applications, instances of hypersensitivity reactions must not be ignored. Titanium hypersensitivity is relatively uncommon, but it has been documented in clinical cases. Reactions may present as mild to severe peri-implant tissue hypersensitivity, potentially leading to complications such as inflammation, pain, and even implant failure.

According to ResearchGate, a case report published in April 2021, described a 64-year-old female patient who experienced acute allergic symptoms including pain, eczema, and swelling shortly after receiving a titanium implant. The patient's prior history of metal allergies contributed to the diagnosis of titanium hypersensitivity, which ultimately led to the removal of the implant and her subsequent recovery.

Similarly, Journal of Research in Medical and Dental Science publication in March 2022, although there is insufficient evidence-based research to definitively prove that titanium dental implants are biocompatible, reported cases of hypersensitivity reactions to titanium and its alloys cannot be ignored. There is a pressing need to develop tests that can accurately detect hypersensitivity to metals and alloys, including titanium, in the oral environment. Such advancements would facilitate further studies on implant hypersensitivity. Clinicians should also assess for hypersensitivity to titanium and its alloys in instances of implant failure. Thus, the above factors could be limiting the global titanium & titanium alloys dental implants market's potential growth.

For more details on this report – Request for Sample

Segment Analysis

The global titanium & titanium alloys dental implants market is segmented based on product type, type of implant, application, end-user, and region.

Product Type:

The commercially pure titanium (CPTi) segment is expected to dominate the global titanium & titanium alloys dental implants market share

The commercially pure titanium (CPTi) segment holds a major portion of the global titanium & titanium alloys dental implants market share and is expected to continue to hold a significant portion of the global titanium & titanium alloys dental implants market share during the forecast period.

The commercially pure titanium (CPTi) segment is integral to the global titanium & titanium alloys dental implants market due to its distinctive properties that make it suitable for dental applications. Commercially pure titanium (CP-Ti) consists of over 99% titanium, with varying amounts of nitrogen, carbon, oxygen, iron, and hydrogen depending on the specific grade. It is classified as a low-to-moderate strength metal and is not suitable for use in aircraft structures or engines. The yield strength of high-purity titanium ranges from 170 to 480 MPa, which is insufficient for heavily loaded aerospace applications.

CP-Ti is utilized in applications where high ductility, excellent corrosion resistance, moderate strength, and good weldability are essential. These characteristics make it suitable for use in medical implants, as well as in aerospace and chemical processing industries.

In the United States, commercially pure titanium is categorized according to the ASTM standard, although this classification system is not universally adopted in other countries. The classification uses a numbering system, such as Grade 1, Grade 2, and so forth, to differentiate between the various types of commercially pure titanium based on their properties and composition.

One of the primary advantages of commercially pure titanium is its excellent biocompatibility. This property enables the material to integrate seamlessly with human bone, minimizing the risk of rejection and promoting successful osseointegration. Consequently, CPTi is extensively used in dental implants, ensuring that patients experience minimal adverse reactions. These factors have solidified the segment's position in the global titanium & titanium alloys dental implants market.

Geographical Analysis

North America is expected to hold a significant position in the global titanium & titanium alloys dental implants market share

North America holds a substantial position in the global titanium & titanium alloys dental implants market and is expected to hold most of the market share.

The rising incidence of dental disorders, particularly periodontal disease and dental caries, significantly drives the demand for titanium dental implants. According to the Fédération Dentaire Internationale, (FDI) stated that between 15% to 20% of middle-aged adults suffer from severe periodontal disease, which can lead to tooth loss. Additionally, approximately 92% of adults aged 20 to 64 have experienced dental caries in their permanent teeth. This growing prevalence necessitates effective tooth replacement solutions like titanium implants.

North America has a substantial aging population that is more susceptible to dental issues requiring implants. The American Dental Association reports that 42% of adults aged 30 and older are affected by periodontitis, with around 7.8% experiencing severe cases. As the population ages, the demand for dental implants is expected to increase, further driving market growth.

Advances in dental technology, including computer-aided design (CAD) and computer-aided manufacturing (CAM), have improved the precision and effectiveness of dental implants. These innovations enhance overall patient experience and outcomes, making titanium implants more appealing to both practitioners and patients.

Furthermore, in this region, a major number of key players' presence, well-advanced healthcare infrastructure, government initiatives & regulatory support, technological advancements, and product launches & approvals would propel this global titanium & titanium alloys dental implants market.

For instance, in December 2021, Health Canada's approval of its first Canadian additively manufactured medical implant marks a significant advancement in the field of personalized medicine and surgical reconstruction. Developed at the 3D Anatomical Construction Laboratory (LARA 3D) in collaboration with Investissement Québec – CRIQ and the CHU de Québec-Université Laval, this bespoke 3D Specifit mandibular plate is specifically designed for patients undergoing reconstruction due to oral cancer.

Thus, the above factors are consolidating the region's position as a dominant force in the global titanium & titanium alloys dental implants market.

Asia Pacific is growing at the fastest pace in the global titanium & titanium alloys dental implants market

Asia Pacific holds the fastest pace in the global titanium & titanium alloys dental implants market and is expected to hold most of the market share.

The aging population in the Asia-Pacific region significantly drives the demand for dental implants. As individuals grow older, they are more likely to face dental issues such as tooth loss and periodontal diseases, necessitating effective replacement solutions like titanium implants. The rise in elderly individuals seeking dental care contributes significantly to market expansion.

There is a growing awareness among consumers regarding the importance of oral health and the availability of advanced dental treatments. This heightened awareness leads to greater acceptance rates of dental implants, as patients recognize the long-term benefits of titanium implants for tooth replacement. Innovations in dental technology, including 3D imaging, computer-aided design (CAD), and computer-aided manufacturing (CAM), have enhanced the precision and success rates of dental implant procedures. These advancements attract both patients and dental professionals, further driving the demand for titanium implants.

Increased government spending on healthcare and supportive policies are facilitating market growth. Various Asia-Pacific countries are investing in healthcare infrastructure to enhance dental care services. Additionally, multinational companies are investing in local implant manufacturers to improve production capabilities and meet rising demand.

There is a rising demand for aesthetic dental solutions as consumers seek natural-looking replacements for missing teeth. Titanium implants are preferred due to their biocompatibility and ability to integrate with bone, providing a stable foundation for artificial teeth that look and function like natural ones.

Furthermore, key players in the region investments in dental implants that would drive this titanium & titanium alloys dental implants market growth. For instance, in October 2023, Mubadala Investment Company's recent investment in Osstem Implant, Korea's largest dental implant material manufacturer, signifies a strategic move within the global titanium and titanium alloys dental implants market. This partnership, alongside MBK Partners and Unison Capital, positions Osstem to leverage its established market presence while enhancing its capabilities in a competitive landscape.

Thus, the above factors are consolidating the region's position as the fastest-growing force in the global titanium & titanium alloys dental implants market.

Competitive Landscape

The major global players in the titanium & titanium alloys dental implants market include Institut Straumann AG, Nobel Biocare Services AG., Dentsply Sirona., Zimmer Biomet, OSSTEM IMPLANT CO., LTD., KYOCERA Medical Technologies, Inc., COWELLMEDI CO., LTD., ZimVie Inc., LeaderMedica SRL, and BioHorizons among others.

Key Developments

• In May 2022, Osstem Europe, launched a next-generation implant system known as the Key Solution (KS) implant in Europe. This innovative system features a unique internal design that enhances the strength and durability of dental implants while providing a user-friendly platform for surgical procedures and prosthesis loading. According to Osstem, barium can attract blood to the titanium surface of implants, facilitating the rapid formation of woven bone. This process enhances the initial stability of the implants and improves their capacity for bone integration and remodeling.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, and product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global titanium & titanium alloys dental implants market report delivers a detailed analysis with 60+ key tables, more than 50 visually impactful figures, and 176 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

Table of Contents

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product Type

3.2. Snippet by Type of Implant

3.3. Snippet by Application

3.4. Snippet by End-User

3.5. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Increasing Prevalence of Dental Disorders

4.1.1.2. XX

4.1.2. Restraints

4.1.2.1. Hypersensitivity and Allergic Reactions

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Patent Analysis

5.5. Regulatory Analysis

5.6. SWOT Analysis

5.7. Unmet Needs

6. By Product Type

6.1. Introduction

6.1.1. Analysis and Y-o-Y Growth Analysis (%), By Product Type

6.1.2. Market Attractiveness Index, By Product Type

6.2. Commercially Pure Titanium (CPTi) *

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.2.3. Grade I

6.2.4. Grade II

6.2.5. Grade III

6.2.6. Grade IV

6.3. Titanium Alloys

6.3.1. Ti-6Al-4V

6.3.2. Ti-6Al-4V Extra Low Interstitial

6.3.3. Ti-5Al-2.5Fe

6.3.4. Ti-3Al-2.5V

7. By Type of Implant

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type of Implant

7.1.2. Market Attractiveness Index, By Type of Implant

7.2. Endosteal Implants*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Subperiosteal Implants

7.4. Transosteal Implants

8. By Application

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

8.1.2. Market Attractiveness Index, By Application

8.2. Single Tooth Replacement*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Multi Tooth Replacement

8.4. Others

9. By End-User

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.1.2. Market Attractiveness Index, By End-User

9.2. Hospitals *

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Dental Clinics

9.4. Others

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type of Implant

10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.7.1. U.S.

10.2.7.2. Canada

10.2.7.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type of Implant

10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.7.1. Germany

10.3.7.2. U.K.

10.3.7.3. France

10.3.7.4. Spain

10.3.7.5. Italy

10.3.7.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type of Implant

10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.7.1. Brazil

10.4.7.2. Argentina

10.4.7.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type of Implant

10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

10.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.7.1. China

10.5.7.2. India

10.5.7.3. Japan

10.5.7.4. South Korea

10.5.7.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Type of Implant

10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Institut Straumann AG *

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. Nobel Biocare Services AG.

12.3. Dentsply Sirona.

12.4. Zimmer Biomet

12.5. OSSTEM IMPLANT CO., LTD.

12.6. KYOCERA Medical Technologies, Inc.

12.7. COWELLMEDI CO., LTD.

12.8. ZimVie Inc.

12.9. LeaderMedica SRL

12.10. BioHorizons (LIST NOT EXHAUSTIVE)

13. Appendix

13.1. About Us and Services

13.2. Contact Us

*** チタン&チタン合金製歯科インプラントの世界市場に関するよくある質問(FAQ) ***

・チタン&チタン合金製歯科インプラントの世界市場規模は?

→DataM Intelligence社は2023年のチタン&チタン合金製歯科インプラントの世界市場規模を58億6000万米ドルと推定しています。

・チタン&チタン合金製歯科インプラントの世界市場予測は?

→DataM Intelligence社は2031年のチタン&チタン合金製歯科インプラントの世界市場規模を123億3000万米ドルと予測しています。

・チタン&チタン合金製歯科インプラント市場の成長率は?

→DataM Intelligence社はチタン&チタン合金製歯科インプラントの世界市場が2024年~2031年に年平均9.8%成長すると展望しています。

・世界のチタン&チタン合金製歯科インプラント市場における主要プレイヤーは?

→「Institut Straumann AG、Nobel Biocare Services AG、Dentsply Sirona、Zimmer Biomet、OSSTEM IMPLANT CO., LTD.、KYOCERA Medical Technologies, Inc.、COWELLMEDI CO., LTD.、ZimVie Inc.、LeaderMedica SRL、BioHorizonsなど ...」をチタン&チタン合金製歯科インプラント市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/