1. 調査手法および範囲

1.1. 調査手法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品種類別抜粋

3.2. 技術別抜粋

3.3. 用途別抜粋

3.4. エンドユーザー別抜粋

3.5. 地域別抜粋

4. ダイナミクス

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 慢性疾患および感染症の増加

4.1.1.2. XX

4.2. 阻害要因

4.2.1.1. 臨床検査機器の高コスト

4.3. 機会

4.3.1. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

6. 製品タイプ別

6.1. はじめに

6.1.1. 市場規模分析および前年比成長率(%)分析、製品タイプ別

6.1.2. 製品種類別市場魅力度指数

6.2. 分析装置*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率分析(%)

6.3. 消耗品

6.4. ソフトウェアおよびサービス

7. 技術別

7.1. はじめに

7.1.1. 市場規模分析および前年比成長率分析(%)、技術別

7.1.2. 市場魅力度指数、技術別

7.2. 臨床化学*

7.2.1. 概要

7.2.2. 市場規模分析および前年比成長率分析(%)

7.3. 分子診断

7.4. 免疫測定

7.5. ポイント・オブ・ケア・テスティング(POCT)

7.6. その他

8. 用途別

8.1. はじめに

8.1.1. 用途別市場規模分析および前年比成長率(%)

8.1.2. 用途別市場魅力度指数

8.2. 感染症検査*

8.2.1. イントロダクション

8.2.2. 市場規模分析および前年比成長率分析(%)

8.3. 癌診断

8.4. 循環器検査

8.5. 内分泌学検査

8.6. 腎臓学検査

8.7. その他

9. エンドユーザー別

9.1. はじめに

9.1.1. エンドユーザー別市場規模分析および前年比成長率(%)

9.1.2. エンドユーザー別市場魅力度指数

9.2. 病院および診療所*

9.2.1. はじめに

9.2.2. エンドユーザー別市場規模分析および前年比成長率(%)

9.3. 診断ラボ

9.4. 学術・研究機関

9.5. 在宅医療施設

9.6. その他

10. 地域別

10.1. はじめに

10.1.1. 地域別市場規模分析および前年比成長率分析(%)

10.1.2. 地域別市場魅力度指数

10.2. 北米

10.2.1. はじめに

10.2.2. 主要地域別の動向

10.2.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.2.4. 市場規模分析および前年比成長率分析(%)、技術別

10.2.5. 市場規模分析および前年比成長率分析(%)、用途別

10.2.6. エンドユーザー別市場規模分析および前年比成長率分析(%)

10.2.7. 国別市場規模分析および前年比成長率分析(%)

10.2.7.1. 米国

10.2.7.2. カナダ

10.2.7.3. メキシコ

10.3. ヨーロッパ

10.3.1. はじめに

10.3.2. 主要地域別の動向

10.3.3. 市場規模分析および前年比成長率(%)製品種類別

10.3.4. 市場規模分析および前年比成長率(%)技術別

10.3.5. 市場規模分析および前年比成長率(%)用途別

10.3.6. エンドユーザー別市場規模分析および前年比成長率分析(%)

10.3.7. 国別市場規模分析および前年比成長率分析(%)

10.3.7.1. ドイツ

10.3.7.2. 英国

10.3.7.3. フランス

10.3.7.4. スペイン

10.3.7.5. イタリア

10.3.7.6. ヨーロッパのその他地域

10.4. 南アメリカ

10.4.1. はじめに

10.4.2. 主要地域別の動向

10.4.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.4.4. 市場規模分析および前年比成長率(%)、技術別

10.4.5. 市場規模分析および前年比成長率(%)、用途別

10.4.6. 市場規模分析および前年比成長率(%)、エンドユーザー別

10.4.7. 市場規模分析および前年比成長率(%)、国別

10.4.7.1. ブラジル

10.4.7.2. アルゼンチン

10.4.7.3. 南米その他

10.5. アジア太平洋地域

10.5.1. はじめに

10.5.2. 主要地域特有の動向

10.5.3. 市場規模分析および前年比成長率分析(%)、製品種類別

10.5.4. 市場規模分析および前年比成長率(%)、技術別

10.5.5. 市場規模分析および前年比成長率(%)、用途別

10.5.6. 市場規模分析および前年比成長率(%)、エンドユーザー別

10.5.7. 市場規模分析および前年比成長率(%)、国別

10.5.7.1. 中国

10.5.7.2. インド

10.5.7.3. 日本

10.5.7.4. 韓国

10.5.7.5. アジア太平洋地域その他

10.6. 中東およびアフリカ

10.6.1. はじめに

10.6.2. 主要地域特有の動向

10.6.3. 製品種類別市場規模分析および前年比成長率(%)

10.6.4. 技術別市場規模分析および前年比成長率(%)

10.6.5. 用途別市場規模分析および前年比成長率(%)

10.6.6. エンドユーザー別市場規模分析および前年比成長率(%)

11. 競合状況

11.1. 競合シナリオ

11.2. 市場ポジショニング/シェア分析

11.3. 合併・買収分析

12. 企業プロフィール

Abbott Laboratories

Roche Diagnostics

Thermo Fisher Scientific

Siemens Healthineers

Danaher Corporation (Beckman Coulter, Cepheid)

Mindray Bio-Medical Electronics Co., Ltd

Trivitron Healthcare

GenScript

リストは網羅的ではありません

13. 付録

13.1 当社およびサービスについて

13.2 お問い合わせ

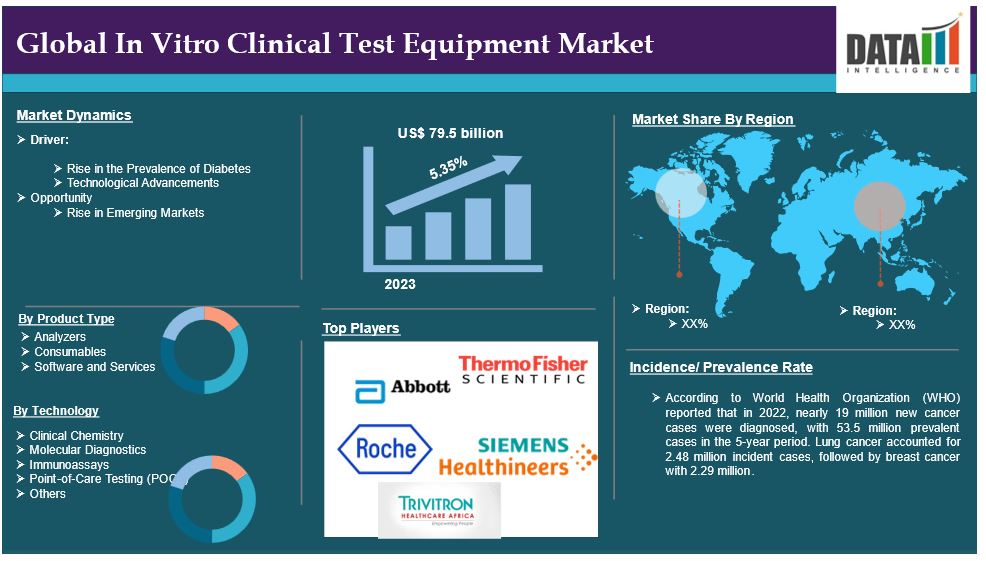

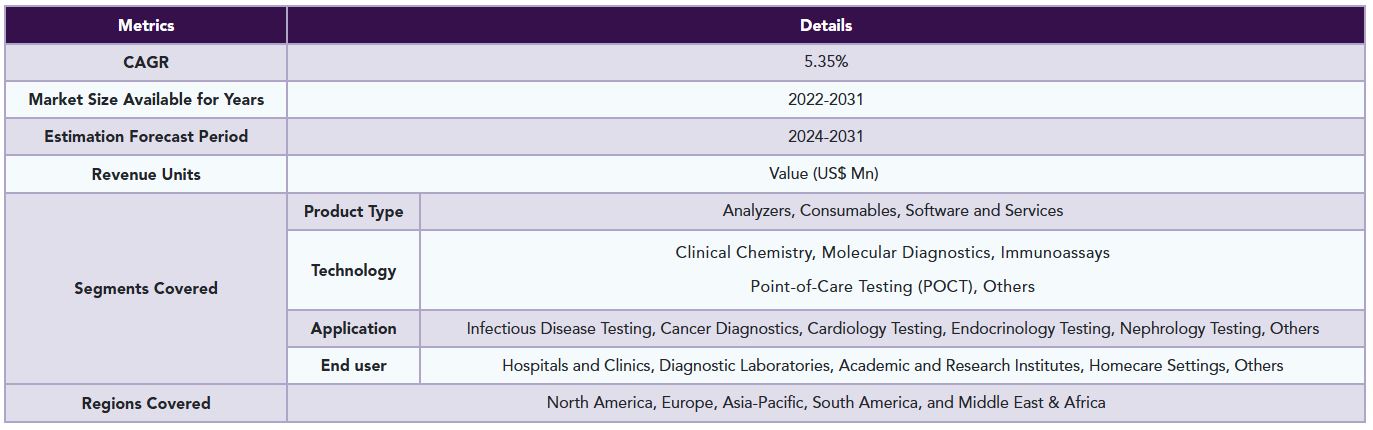

The global In Vitro Clinical Test Equipment market reached US$ 79.5 billion in 2023 and is expected to reach US$ 120.62 billion by 2031, growing at a CAGR of 5.35% during the forecast period 2024-2031.

In vitro clinical test equipment denotes a different but specific category of medical equipment which is utilized in performing , tests that do not involve human subjects and are also mainly performed in a laboratory. Moreover these devices are of a great importance in the processing of various specimens including blood, urine, saliva, or tissue for the purposes of diagnosing, prognosis, treatment response assessment, or even follow-up of diseases.

The traditional in vitro clinical test equipment underwent little to no changes; however, the modern one embraces technology such as automation, artificial intelligence, and connectivity which makes it a more effective, precise, adaptable to healthcare and research demands, and mass testing technique.

Market Dynamics: Drivers & Restraints

Growing Prevalence of Chronic and Infectious Diseases

The rising burden of chronic as well as infectious diseases across the world is amongst the leading factors that encourage the uptake of in vitro clinical test equipment. Chronic ailments like diabetes, heart diseases, and cancer necessitate periodical observation as well as accurate diagnostic tests so as to formulate the best treatment procedures.

For instance, according to World Health Organization (WHO) reported that in 2022, nearly 19 billion new cancer cases were diagnosed, with 53.5 billion prevalent cases in the 5-year period. Lung cancer accounted for 2.48 billion incident cases, followed by breast cancer with 2.29 billion. The International Agency for Research on Cancer projected that cancer incidence cases will reach 21.3 billion in 2025 and 24.1 billion in 2030. Breast cancer is becoming the most burdening cancer globally, with advances in early detection and diagnosis, including advanced tumor profiling technologies, paving the way for a projected 2.7 billion incidence cases in 2030.

At the same time, communicable diseases such as COVID-19, influenza, and any other newly coined pathogens have increased the demand for quick and effective diagnosis machinery in order to control the outbreaks and curb their spread. Portable diagnostic testing devices including molecular diagnostics and immunoassays are also available to support public health and disease management by offering more reliable, rapid, and non-invasive diagnostic testing solutions.

High Cost of the Clinical Test Equipments

The high cost involved with the equipment serves as one of the primary drawbacks in the enhancement of the in vitro clinical test equipment sector. This equipment often comprises advanced diagnostic machines such as molecular or hematology analyzers, automated systems, and immunoassay equipment, all of which demand a high capital due to their complex nature, technological precisions, and the certifications needed from regulating bodies.

These high costs are quite detrimental to some health care providers, laboratories or countries with recent developments, as some of them do not have the necessary capital for the initial investment. Apart from that, the spare parts, continuous calibration, and day-to-day expenses associated with these instruments increase the cost problemati. Due to this cost hurdle, use of advanced diagnostic methods often becomes out of reach, more so is in under developed or developing regions causing slow growth in the market for in vivo test solutions and resulting in low uptake of in vitro testing alternatives.

Segment Analysis

The global In vitro clinical test equipment market is segmented based on product type, technology, application, end user, and region.

Product Type:

Analyzers segment is expected to dominate the In vitro clinical test equipment market share

The analyzers segment holds a major portion of the In vitro clinical test equipment market share and is expected to continue to hold a significant portion of the In vitro clinical test equipment market share during the forecast period.

Analyzers are crucial tools in the global in vitro clinical test equipment market, aiding in the diagnosis and monitoring of various diseases and health conditions. They process biological samples like blood, urine, and tissues to detect biomarkers, pathogens, or abnormalities. Modern analyzers offer high throughput, reduce human error, and improve laboratory workflow efficiency. They are essential in managing chronic diseases, detecting infections, and monitoring treatment effectiveness, driving their adoption in hospitals, diagnostic labs, and research settings. Their versatility and ability to provide rapid results make analyzers a cornerstone of the in vitro diagnostic landscape.

For instance, in January 2024, HORIBA Medical has introduced the HELO 2.0 high throughput automated hematology platform, CE-IVDR approved and pending US FDA approval. This new generation high-end hematology range, designed in consultation with customers, offers a flexible, efficient, and scalable modular solution for mid to large-scale laboratories, offering a flexible and efficient solution for high throughput automated hematology.

Molecular Diagnostics segment is the fastest-growing segment in the In vitro clinical test equipment market share

The molecular diagnostics segment is the fastest-growing segment in the In vitro clinical test equipment market share and is expected to hold the market share over the forecast period.

The molecular diagnostics segment is a significant player in the global in vitro clinical test equipment market due to its ability to provide accurate, rapid, and sensitive disease detection at genetic and molecular levels. This includes advanced technologies like PCR, NGS, and molecular assays, which are crucial for detecting infectious diseases, genetic disorders, and cancer biomarkers. The demand for personalized medicine and precision diagnostics is driving the expansion of molecular diagnostics, enabling targeted therapies based on individual genetic profiles. The increasing prevalence of infectious diseases, like COVID-19, has further accelerated the need for molecular diagnostic tools. The segment continues to grow with continuous technological advancements enhancing the accuracy, efficiency, and affordability of in vitro clinical tests.

For instance, in April 2023, ELITech Group has announced the launch of a new high-throughput sample-to-result instrument for molecular diagnostics. The company, which introduced the ELITe InGenius in 2016, has since expanded its menu to over 50 CE-IVD parameters and validated over 20 sample matrices. BeGenius, launched in 2021, is designed for laboratories requiring higher throughput. Over 1100 instruments have been installed globally, and ELITech MDx is committed to transitioning its entire portfolio of CE-IVD parameters to IVDR.

Geographical Analysis

North America is expected to hold a significant position in the In vitro Clinical Test Equipment market share

North America holds a substantial position in the In vitro Clinical Test Equipment market and is expected to hold most of the market share due to the advanced healthcare infrastructure, high healthcare spending, and a strong emphasis on research and development. The US, with its leading medical device manufacturers, research institutions, and hospitals, drives demand for advanced diagnostic technologies. The region's regulatory environment and strict quality standards by agencies like the FDA ensure high-quality in vitro diagnostic equipment.

Moreover, the rising prevalence of chronic diseases, personalized medicine, early detection, and prevention also contribute to the expanding use of in vitro diagnostic tools in North America. The ongoing efforts to combat infectious diseases like COVID-19 further emphasize the importance of molecular diagnostics and in vitro testing solutions, making the North American market a vital hub for innovation and growth.

For instance, in November 2024, Veracyte has signed a multi-year agreement with Illumina to develop and offer high-performing molecular tests as decentralized in vitro diagnostic (IVD) tests on Illumina's NextSeq 550Dx next-generation sequencing instrument. This is part of Veracyte's expanded, multi-platform IVD approach, which includes qPCR, and aims to make its tests available to more patients globally.

Europe is growing at the fastest pace in the In vitro Clinical Test Equipment market

Europe holds the fastest pace in the In vitro Clinical Test Equipment market and is expected to hold most of the market share due to the increasing prevalence of chronic diseases, well-established healthcare infrastructure, significant investments in research and development, and a strong regulatory framework. This has led to increased demand for advanced diagnostic tools, boosting market confidence and adoption. The aging population in many European countries also intensifies the need for efficient and early diagnostic methods. The presence of leading medical device industry players and high awareness and healthcare expenditure continue to fuel market growth in this region.

Competitive Landscape

The major global players in the In vitro clinical test equipment market include Abbott Laboratories, Roche Diagnostics, Thermo Fisher Scientific, Siemens Healthineers, Danaher Corporation (Beckman Coulter, Cepheid), Mindray Bio-Medical Electronics Co., Ltd, Trivitron Healthcare, GenScript and among others.

Emerging Players

The emerging players in the In vitro clinical test equipment market include PerkinElmer Inc, Agilent Technologies, Inc, Sysmex Corporation and among others.

Key Developments

• In September 2023, NeoDx Biotech Labs has introduced a Real-time PCR-Technology-based in vitro diagnostic kit for Ankylosing Spondylitis, enhancing healthcare services' testing capabilities. The kit, HLA-B27 RT-PCR detection kit for Exon 2/Exon 3, detects Human Leukocyte Antigen B27 in whole blood, a key factor in inflammatory disorders like Ankylosing Spondylitis, Psoriasis, Inflammatory Bowel Disease, and Reactive Arthritis, aiding early diagnosis and treatment.

Why Purchase the Report?

• To visualize the global In vitro clinical test equipment market segmentation based on product type, technology, application, end user and region and understand key commercial assets and players.

• Identify commercial opportunities by analyzing trends and co-development.

• Excel data sheet with numerous data points of the In vitro clinical test equipment market with all segments.

• PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

• Product mapping is available in excel consisting of key products of all the major players.

The global In vitro clinical test equipment market report would provide approximately 70 tables, 65 figures, and 184 pages.

Target Audience 2023

• Manufacturers/ Buyers

• Industry Investors/Investment Bankers

• Research Professionals

• Emerging Companies

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product Type

3.2. Snippet by Technology

3.3. Snippet by Application

3.4. Snippet by End user

3.5. Snippet by Region

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Growing Prevalence of Chronic and Infectious Diseases

4.1.1.2. XX

4.2. Restraints

4.2.1.1. High Cost of the Clinical Test Equipment’s

4.3. Opportunity

4.3.1. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

6. By Product Type

6.1. Introduction

6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

6.1.2. Market Attractiveness Index, By Product Type

6.2. Analyzers*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.3. Consumables

6.4. Software and Services

7. By Technology

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

7.1.2. Market Attractiveness Index, By Technology

7.2. Clinical Chemistry*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Molecular Diagnostics

7.4. Immunoassays

7.5. Point-of-Care Testing (POCT)

7.6. Others

8. By Application

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

8.1.2. Market Attractiveness Index, By Application

8.2. Infectious Disease Testing*

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Cancer Diagnostics

8.4. Cardiology Testing

8.5. Endocrinology Testing

8.6. Nephrology Testing

8.7. Others

9. By End user

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End user

9.1.2. Market Attractiveness Index, By End user

9.2. Hospitals and Clinics*

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Diagnostic Laboratories

9.4. Academic and Research Institutes

9.5. Homecare Settings

9.6. Others

10. By Region

10.1. Introduction

10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

10.1.2. Market Attractiveness Index, By Region

10.2. North America

10.2.1. Introduction

10.2.2. Key Region-Specific Dynamics

10.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End user

10.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.2.7.1. U.S.

10.2.7.2. Canada

10.2.7.3. Mexico

10.3. Europe

10.3.1. Introduction

10.3.2. Key Region-Specific Dynamics

10.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End user

10.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.3.7.1. Germany

10.3.7.2. U.K.

10.3.7.3. France

10.3.7.4. Spain

10.3.7.5. Italy

10.3.7.6. Rest of Europe

10.4. South America

10.4.1. Introduction

10.4.2. Key Region-Specific Dynamics

10.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End user

10.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.4.7.1. Brazil

10.4.7.2. Argentina

10.4.7.3. Rest of South America

10.5. Asia-Pacific

10.5.1. Introduction

10.5.2. Key Region-Specific Dynamics

10.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End user

10.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

10.5.7.1. China

10.5.7.2. India

10.5.7.3. Japan

10.5.7.4. South Korea

10.5.7.5. Rest of Asia-Pacific

10.6. Middle East and Africa

10.6.1. Introduction

10.6.2. Key Region-Specific Dynamics

10.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Product Type

10.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

10.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

10.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By End user

11. Competitive Landscape

11.1. Competitive Scenario

11.2. Market Positioning/Share Analysis

11.3. Mergers and Acquisitions Analysis

12. Company Profiles

12.1. Abbott Laboratories*

12.1.1. Company Overview

12.1.2. Product Portfolio and Description

12.1.3. Financial Overview

12.1.4. Key Developments

12.2. Roche Diagnostics

12.3. Thermo Fisher Scientific

12.4. Siemens Healthineers

12.5. Danaher Corporation (Beckman Coulter, Cepheid)

12.6. Mindray Bio-Medical Electronics Co., Ltd

12.7. Trivitron Healthcare

12.8. GenScript

LIST NOT EXHAUSTIVE

13. Appendix

13.1 About Us and Services

13.2 Contact Us

*** 体外臨床検査用機器の世界市場に関するよくある質問(FAQ) ***

・体外臨床検査用機器の世界市場規模は?

→DataM Intelligence社は2023年の体外臨床検査用機器の世界市場規模を795億米ドルと推定しています。

・体外臨床検査用機器の世界市場予測は?

→DataM Intelligence社は2031年の体外臨床検査用機器の世界市場規模を1206.2億米ドルと予測しています。

・体外臨床検査用機器市場の成長率は?

→DataM Intelligence社は体外臨床検査用機器の世界市場が2024年~2031年に年平均5.4%成長すると展望しています。

・世界の体外臨床検査用機器市場における主要プレイヤーは?

→「Abbott Laboratories、Roche Diagnostics、Thermo Fisher Scientific、Siemens Healthineers、Danaher Corporation (Beckman Coulter, Cepheid)、Mindray Bio-Medical Electronics Co., Ltd、Trivitron Healthcare、GenScriptなど ...」を体外臨床検査用機器市場のグローバル主要プレイヤーとして判断しています。

※上記FAQの市場規模、市場予測、成長率、主要企業に関する情報は本レポートの概要を作成した時点での情報であり、最終レポートの情報と少し異なる場合があります。

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/