1. 調査手法および範囲

1.1. 調査手法

1.2. 調査目的およびレポートの範囲

2. 定義および概要

3. エグゼクティブサマリー

3.1. 製品種類別抜粋

3.2. 技術別抜粋

3.3. 処置の種類別抜粋

3.4. エンドユーザー別抜粋

4. 力学

4.1. 影響因子

4.1.1. 推進要因

4.1.1.1. 口腔疾患の負担増大と

4.1.1.2. XX

4.1.2. 阻害要因

4.1.2.1. 機器および治療費の高額さ

4.1.3. 機会

4.1.4. 影響分析

5. 産業分析

5.1. ポーターのファイブフォース分析

5.2. サプライチェーン分析

5.3. 価格分析

5.4. 規制分析

6. 製品種類別

6.1. はじめに

6.1.1. 製品種類別分析および前年比成長率(%)

6.1.2. 製品種類別市場魅力度指数

6.2. 一般および診断用機器*

6.2.1. はじめに

6.2.2. 市場規模分析および前年比成長率(%)

6.2.3. 歯科用レーザー

6.2.4. 放射線機器

6.2.5. 歯科用チェアおよび機器

6.2.6. その他

6.3. 歯科用消耗品

6.3.1. 歯科用生体材料

6.3.2. 歯科用インプラント

6.3.3. クラウンおよびブリッジ

6.3.4. その他

6.4. その他

7. 技術別

7.1. はじめに

7.1.1. 技術別市場規模分析および前年比成長率(%)

7.1.2. 技術別市場魅力度指数

7.2. デジタルソリューション*

7.2.1. はじめに

7.2.2. 市場規模分析および前年比成長率(%)

7.3. 先進イメージング技術

7.4. 遠隔歯科ソリューション

7.5. その他

8. 治療の種類別

8.1. はじめに

8.1.1. 市場規模分析および前年比成長率(%)、治療の種類別

8.1.2. 市場魅力度指数、治療の種類別

8.2. 矯正器具 *

8.2.1. はじめに

8.2.2. 市場規模分析および前年比成長率分析(%)

8.3. 歯内治療用器具

8.4. 歯周治療用器具

8.5. 補綴治療用器具

9. エンドユーザー別

9.1. はじめに

9.1.1. エンドユーザー別市場規模分析および前年比成長率分析(%)

9.1.2. 市場魅力度指数、エンドユーザー別

9.2. 病院 *

9.2.1. 概要

9.2.2. 市場規模分析および前年比成長率分析(%)

9.3. 歯科クリニック

9.4. その他

10. 競合状況

10.1. 競合シナリオ

10.2. 市場ポジショニング/シェア分析

10.3. 合併・買収分析

11. 企業プロフィール

Dentsply Sirona

3M

Takara Belmont

KaVo Dental

J. MORITA CORP.

MANI, INC.

GC Corporation

Nakanishi Inc. (NSK)

Ivoclar Vivadent

Ultradent Products Inc.

リストは完全なものではありません。

12. 付録

12.1. 当社およびサービスについて

12.2. お問い合わせ

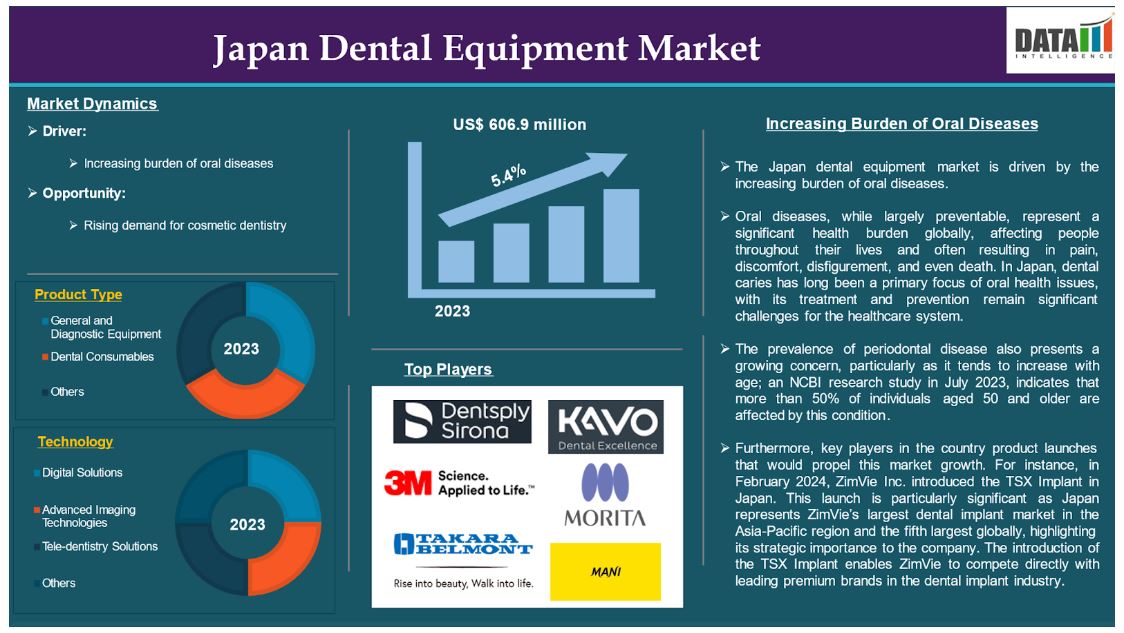

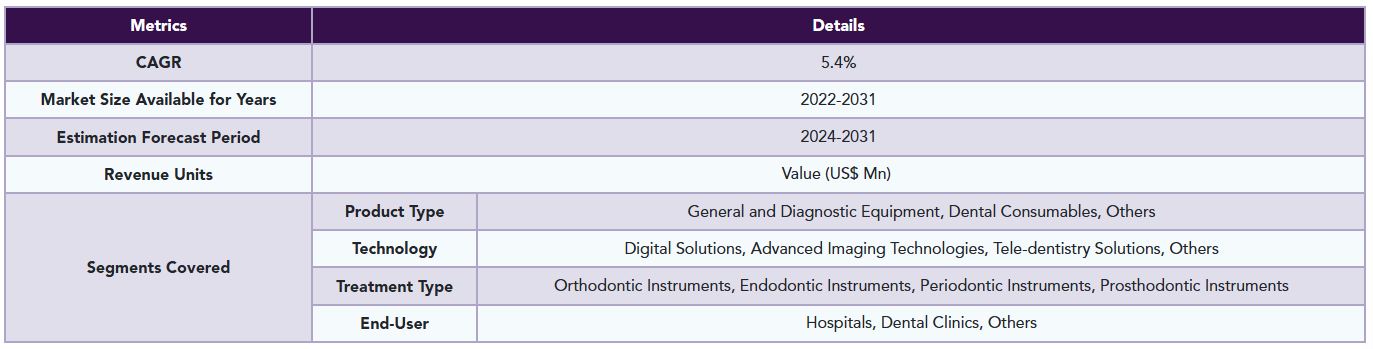

The Japan dental equipment market reached US$ 606.9 million in 2023 and is expected to reach US$ 924.2 million by 2031, growing at a CAGR of 5.4 % during the forecast period 2024-2031.

Dental equipment comprises a specialized collection of instruments utilized by oral surgeons and dental specialists to conduct a variety of procedures involving the mouth, jaw, and face. These procedures encompass tooth extractions, implant placements, bone grafting, and corrective jaw surgeries. The range of dental instruments includes scalpels and blades designed for precise incisions in gum tissue and bone, available in various shapes and sizes to meet specific treatment needs.

Dental equipment includes permanent fixtures commonly found in dental offices, such as chairs, lights, x-ray and imaging machines, lasers, compressors, vacuums, handpieces, and cabinets. These tools are vital for ensuring the effective delivery of dental care and maintaining healthy teeth and gums.

Furthermore, dental equipment encompasses utility systems that support the operation of a dental practice, including infection control protocols and setups for portable dental operatories. This equipment can be categorized into multiple types to cover the diverse needs of dental practices in treating patients effectively. These factors have driven the Japan dental equipment market expansion.

Market Dynamics: Drivers & Restraints

Increasing Burden of Oral Diseases

The increasing burden of oral diseases is significantly driving the growth of the Japan dental equipment market and is expected to drive throughout the market forecast period.

Oral diseases, while largely preventable, represent a significant health burden, affecting people throughout their lives and often resulting in pain, discomfort, disfigurement, and even death. In Japan, dental caries has long been a primary focus of oral health issues, with its treatment and prevention remain significant challenges for the healthcare system.

Despite improvements in dental care and public health initiatives, caries continue to affect a substantial portion of the population. The prevalence of periodontal disease also presents a growing concern, particularly as it tends to increase with age; an NCBI research study in July 2023, indicates that more than 50% of individuals aged 50 and older are affected by this condition.

Periodontal disease is characterized by chronic inflammation that can lead to tooth loss if left untreated. Unlike caries, which often causes noticeable pain as it progresses, periodontal disease may not present severe symptoms until significant damage has occurred, making it a "silent" disease. This lack of immediate discomfort can result in delayed diagnosis and treatment, further exacerbating the condition. Consequently, there is an urgent need for public health initiatives that not only continue to address caries but also shift focus towards preventing and managing periodontal disease, especially as Japan faces the challenges of an aging population.

Furthermore, key players' strategies such as partnerships and collaborations would propel this Japan dental equipment market. For instance, in November 2021, Singapore-based Zenyum, announced its expansion into Japan, marking its entry into the ninth market across Asia. This move is part of Zenyum's strategy to broaden its reach and capitalize on the growing demand for dental solutions in the region. The company has gained recognition as one of Asia's fastest-growing brands in the consumer dental sector and was named a LinkedIn Top Startup in 2021.

Also, in August 2021, Kyocera Corporation, led by President Hideo Tanimoto, announced a strategic partnership with Osteon Digital Japan Co., Ltd., headed by CEO Michael Tuckman. This collaboration focuses on continuous sales transactions and will commence the sale of customized dental prostheses for implants utilizing Osteon’s advanced digital technology.

This agreement is significant for Kyocera as it aims to enhance its presence in the dental implant market, particularly in Japan, which is a key region for dental innovations. By partnering with Osteon, Kyocera seeks to leverage Osteon’s expertise in digital solutions and CAD/CAM technology to improve its offerings in dental prosthetics. All these factors demand the Japan dental equipment market.

Moreover, the rising demand for cosmetic dentistry contributes to the Japan dental equipment market expansion.

High Equipment and Treatment Costs

The high costs associated with advanced dental equipment present a significant barrier for many dental practices in Japan, particularly for smaller clinics. Advanced technologies, such as digital imaging systems and lasers, require substantial financial investment, which can lead practitioners to postpone upgrades or choose less effective options, ultimately affecting the quality of care.

Additionally, dental insurance coverage in Japan is often limited; many advanced procedures are not fully reimbursed, forcing patients to pay a considerable portion of these expenses out-of-pocket. This financial burden can deter individuals from seeking necessary treatments, particularly elective or cosmetic procedures.

Expensive procedures and equipment can mean increased out-of-pocket expenses for patients. This may discourage patients from pursuing required dental surgery, reducing overall demand for the equipment utilized in those procedures. Smaller dental practices, particularly in low-income areas, may be hesitant to invest in expensive equipment due to concerns about return on investment. The high equipment and treatment costs will hinder the growth of Japan dental equipment market.

The prices of some dental X-ray instruments can be as low as 500 USD or less, while the newest, high-tier systems may cost as much as 100,000 USD. Thus, the above factors could be limiting the Japan dental equipment market's potential growth.

Segment Analysis

The Japan dental equipment market is segmented based on product type, technology, treatment type, and end-user.

Product Type:

The dental consumables segment is expected to dominate the Japan dental equipment market share

The dental consumables segment holds a major portion of the Japan dental equipment market share and is expected to continue to hold a significant portion of the Japan dental equipment market share during the forecast period.

Consumables in dentistry, such as drills, burs, scalpels, sutures, and barriers (drapes), are disposable items that require frequent repurchases by dental clinics. This creates a consistent and recurring revenue stream for manufacturers compared to capital equipment sales, which typically involve significant upfront costs for research, development, and production. In contrast, consumables generally have lower production costs and higher profit margins.

The consumable segment is continually evolving due to innovations in materials, design, and functionality. This ongoing cycle of innovation encourages dentists to adopt and utilize new consumables, contributing to market growth. As a result, these factors are expected to drive the growth of the consumable segment, which is anticipated to dominate the Japan dental equipment market share moving forward.

Furthermore, key players in the country product launches that would propel this segment's growth in the Japan dental equipment market. For instance, in February 2024, ZimVie Inc. introduced the TSX Implant in Japan. This launch is particularly significant as Japan represents ZimVie’s largest dental implant market in the Asia-Pacific region and the fifth largest globally, highlighting its strategic importance to the company. The introduction of the TSX Implant enables ZimVie to compete directly with leading premium brands in the dental implant industry. These factors have solidified the segment's position in the Japan dental equipment market.

Competitive Landscape

The major players in the Japan dental equipment market include Dentsply Sirona., 3M, Takara Belmont, KaVo Dental, J. MORITA CORP., MANI, INC., GC Corporation, Nakanishi Inc. (NSK), Ivoclar Vivadent, and Ultradent Products Inc. among others.

Emerging Players

The emerging players in the Japan dental equipment market include Imagoworks Inc., and Zenyum, among others.

Key Developments

• In January 2023, Imagoworks, a South Korean company specializing in digital dental solutions powered by artificial intelligence (AI), has recently announced a distribution agreement with Ci Medical, a dental supplier, to introduce its Dentbird Solutions software into the Japanese dental market. This partnership marks a significant step for Imagoworks as it expands its presence in Asia.

• In November 2022, NSK Ltd. introduced QuickStopBearing, an innovation designed for air turbine dental handpieces, which are commonly used instruments in dental practices worldwide. This development aims to enhance both the efficiency and safety of dental procedures, addressing critical needs in the dental industry.

Why Purchase the Report?

• Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

• Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

• Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

• Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

• Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

• Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

• Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

• Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

• Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

• Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

• Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

• Post-market Surveillance: Uses post-market data to enhance product safety and access.

• Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The Japan dental equipment market report would provide approximately 42 tables, 33 figures, and 183 pages.

Target Audience 2023

• Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

• Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

• Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

• Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

• Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

• Supply Chain: Distribution and Supply Chain Managers.

• Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

• Academic & Research: Academic Institutions.

1. Methodology and Scope

1.1. Research Methodology

1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

3.1. Snippet by Product Type

3.2. Snippet by Technology

3.3. Snippet by Treatment Type

3.4. Snippet by End-User

4. Dynamics

4.1. Impacting Factors

4.1.1. Drivers

4.1.1.1. Increasing Burden of Oral Diseases and

4.1.1.2. XX

4.1.2. Restraints

4.1.2.1. High Equipment and Treatment Costs

4.1.3. Opportunity

4.1.4. Impact Analysis

5. Industry Analysis

5.1. Porter’s Five Force Analysis

5.2. Supply Chain Analysis

5.3. Pricing Analysis

5.4. Regulatory Analysis

6. By Product Type

6.1. Introduction

6.1.1. Analysis and Y-o-Y Growth Analysis (%), By Product Type

6.1.2. Market Attractiveness Index, By Product Type

6.2. General and Diagnostic Equipment*

6.2.1. Introduction

6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

6.2.3. Dental Lasers

6.2.4. Radiology Equipment

6.2.5. Dental Chairs and Equipment

6.2.6. Others

6.3. Dental Consumables

6.3.1. Dental Biomaterials

6.3.2. Dental Implants

6.3.3. Crowns and Bridges

6.3.4. Others

6.4. Others

7. By Technology

7.1. Introduction

7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Technology

7.1.2. Market Attractiveness Index, By Technology

7.2. Digital Solutions*

7.2.1. Introduction

7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

7.3. Advanced Imaging Technologies

7.4. Tele-dentistry Solutions

7.5. Others

8. By Treatment Type

8.1. Introduction

8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Treatment Type

8.1.2. Market Attractiveness Index, By Treatment Type

8.2. Orthodontic Instruments *

8.2.1. Introduction

8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

8.3. Endodontic Instruments

8.4. Periodontic Instruments

8.5. Prosthodontic Instruments

9. By End-User

9.1. Introduction

9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By End-User

9.1.2. Market Attractiveness Index, By End-User

9.2. Hospitals *

9.2.1. Introduction

9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

9.3. Dental Clinics

9.4. Others

10. Competitive Landscape

10.1. Competitive Scenario

10.2. Market Positioning/Share Analysis

10.3. Mergers and Acquisitions Analysis

11. Company Profiles

11.1. Dentsply Sirona. *

11.1.1. Company Overview

11.1.2. Product Portfolio and Description

11.1.3. Financial Overview

11.1.4. Key Developments

11.2. 3M

11.3. Takara Belmont

11.4. KaVo Dental

11.5. J. MORITA CORP.

11.6. MANI, INC.

11.7. GC Corporation

11.8. Nakanishi Inc. (NSK)

11.9. Ivoclar Vivadent

11.10. Ultradent Products Inc.

LIST NOT EXHAUSTIVE

12. Appendix

12.1. About Us and Services

12.2. Contact Us

*** 免責事項 ***

https://www.globalresearch.co.jp/disclaimer/